TODAY’S S&P 500 SET-UP - March 11, 2011

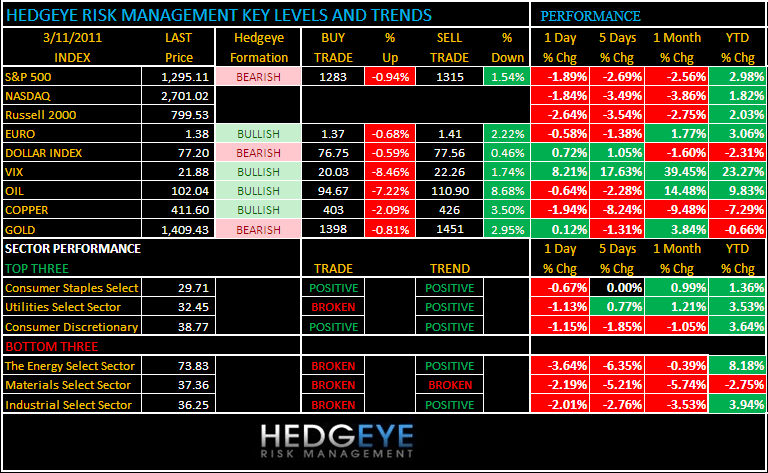

Overnight China down on another sequentially accelerating monthly inflation reading (February (+4.9% CPI, +7.2% PPI). We continue to hammer home the theme – Global Growth Slowing as Global Inflation Accelerates. As we look at today’s set up for the S&P 500, the range is 32 points or -0.94% downside to 1283 and 1.54% upside to 1315.

MACRO DATA POINTS:

- 8:30a.m.: U.S. retail sales - Bloomberg estimate is 1%

- 8:30 a.m.: Fed’s Dudley speaks in New York

- 9:55 a.m.: U Michigan Confidence, est. 76.3, prior 77.5

- 10 a.m.: Business inventories, est. 0.8%, prior 0.8%

WHAT TO WATCH:

- APPL may sell 600,000 units of the second version of theiPad2 when it debuts this weekend

- Saudi Arabia anti-government demonstrators have called for a “Day of Rage”

- China’s inflation and industrial production exceeded forecasts in February

- Libyan forces are mounting a full-scale attack on rebels, as NATO defense ministers said they lack the authority to impose a no-fly zone

- President Obama will hold a news conference today to discuss rising energy prices

PERFORMANCE:

As of the close yesterday we have 3 of 9 sectors positive on TRADE and 8 of 9 sectors positive on TREND. The XLB was the 1st S&P Sector to break its intermediate-term TREND line since May, 2010. The 3 Sectors that remain bullish on both TRADE and TREND durations are all low beta defensive sectors:

- Healthcare (XLV)

- Utilities (XLU)

- Consumer Staples (XLP)

- One day: Dow (1.87%), S&P (1.89%), Nasdaq (1.84%), Russell 2000 (2.64%)

- Month-to-date: Dow (1.98%), S&P (2.42%), Nasdaq (2.92%), Russell (2.90%)

- Quarter/Year-to-date: Dow +3.52%, S&P +2.98%, Nasdaq +1.82%, Russell +2.03%

- Sector Performance: - Energy (3.6%), Materials (2.2%), Financials (2.1%), Tech (2%), Industrials (2%), Healthcare (1.6%), Utilities (1.2%), Consumer Disc (1%), Consumer Spls (0.7%),

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2188 (-1966)

- VOLUME: NYSE 1120.06 (+28.56%)

- VIX: 21.88 +8.21% YTD PERFORMANCE: +23.27%

- SPX PUT/CALL RATIO: 1.35 from 2.27 (-40.41%)

CREDIT/ECONOMIC MARKET LOOK:

Yesterday, Treasuries were stronger for a second straight session with the heightened deterioration in the risk backdrop.

- TED SPREAD: 24.66 +0.406 (1.672%)

- 3-MONTH T-BILL YIELD: 0.08% -0.02%

- 10-Year: 3.46 from 3.48

- YIELD CURVE: 2.81 from 2.78

COMMODITY/GROWTH EXPECTATION:

- CRB: 354.45 -1.61% YTD: +6.50%

- Oil: 102.70 -1.61%; YTD: +9.82% (trading -1.43% in the AM)

- COPPER: 419.75 -0.36%; YTD: -7.28% (trading -2.53% in the AM)

- GOLD: 1,407.80 -1.52%; YTD: -0.67% (trading +0.07% in the AM)

COMMODITY HEADLINES:

- Oil pared losses after the police in Saudi Arabia, the Middle East’s biggest producer of crude, reportedly opened fire at a rally in the east of the country.

- Gold fell the most in a week as a stronger dollar prompted some investors to sell the metal after unrest in the Middle East and northern Africa pushed prices to a record.

- Copper fell to the lowest in almost three months as imports slowed in China, the world’s biggest user, and amid rising concern that global growth may ease.

- Inventories of the grain will total 181.9 million metric tons as of May 31, up 2.3 percent from a February forecast, the U.S. Department of Agriculture said in a report today.

- Cash cattle prices this week hit a record high at mostly $1.18 a pound on a live basis and from $1.86 to $1.93 dressed in Nebraska in active trading Wednesday.

CURRENCIES:

- EURO: 1.33820 -0.58% (trading -0.25% in the AM)

- DOLLAR: 77.276 +0.72% (trading -0.11% in the AM)

EUROPEAN MARKETS:

- FTSE 100: (0.63%); DAX: (1.05%); CAC 40: (1.04%)

- European markets opened lower on continuing unrest in NAME and after an 8.9 magnitude earthquake hit Japan.

- Markets across the region saw a broad retreat with all sectors trading lower.

- An EU leaders meeting today will discuss the Libyan crisis as well as EuroZone bailout fund, though it is unlikely that any final decisions will be made on the rescue package ahead of the leaders' Summit on 24-Mar.

- Germany Feb final CPI +2.1% y/y vs prior +2.0%; Feb wholesales prices +10.8% y/y vs consensus +10.5%

- UK Feb core PPI 3.1% y/y vs consensus 3.4% and prior 3.2%.

ASIAN MARKTES:

- Nikkei (1.7%); Hang Seng (1.6%); Shanghai Composite (0.8%)

- A major earthquake lasted 14 minutes before the close in Japan

- Banks led China down after inflation data prompted fears of further tightening measures. An early afternoon rally was wiped out by the Japanese earthquake.

- Australia was lower across the board.

- South Korea fell as foreigners sold out of the market.

- China February CPI +4.9% y/y vs consensus +4.8%. February PPI +7.2% y/y vs consensus +7.0%.

Howard Penney

Managing Director