Below is a complimentary Demography Unplugged research note written by Hedgeye Demography analyst Neil Howe. Click here to learn more and subscribe.

|

Once the hottest trend in investing, ESG is now under fire. The ESG label is being targeted by politicians and regulators—some of whom want it to be more clearly defined, and others who want to ban it altogether. (Reuters) |

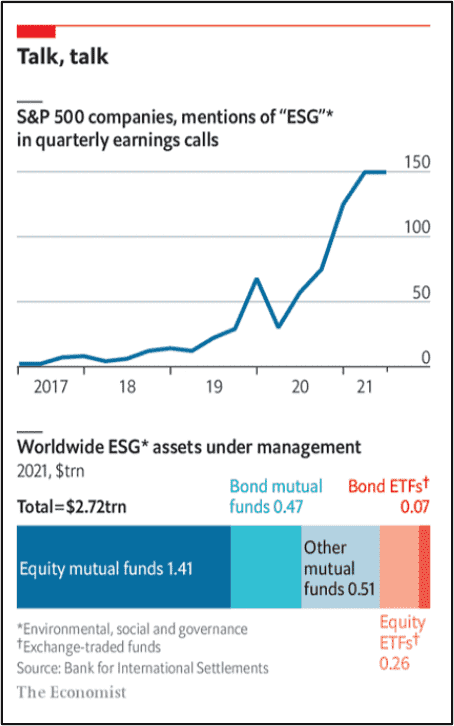

NH: It wasn’t long ago that ESG was championed as the future of investing. Since 2017, the number of sustainable funds and ETFs in the United States has nearly tripled, with the assets in them soaring from $70B to $296B.

Worldwide, ESG funds in 2021 held $2.7T. BlackRock, the world’s largest asset manager, has led the way.

But now the backlash has arrived. Politicians and investors attacking ESG insist that it hurts local industries, delivers subpar returns, lacks any transparent method, and subverts the democratic process. ESG funds are also under scrutiny from the SEC, which wants to crack down on “greenwashing."

Republicans are leading the backlash. They charge that firm CEOs are being strongarmed, against their own judgment, to adopt various "social responsibility" policies in order keep the ESG label.

That label, they say, got its initial clout largely from blue-zone states (like CA and NY) that dutifully invested most of their pension funds according to ESG guidelines. So maybe, Republicans feel, it's time for red-zone states to strike back.

So far this year, 17 GOP-led states have introduced at least 44 bills to punish firms adopting ESG-friendly policies--and, most of all, the financial companies offering ESG funds.

Florida Gov. Ron DeSantis recently banned state pension fund managers from considering ESG criteria when choosing investments.

Texas Comptroller Glenn Hegar blacklisted 10 major financial firms, including BlackRock and Credit Suisse, for “boycotting energy companies.” West Virginia cut ties with some of the same firms, claiming that their ESG efforts are harming the coal industry.

The pushback has even given rise to “anti-woke” ETFs. The biggest is Strive Asset Management’s U.S. Energy ETF (DRLL), which has raised more than $315M in less than a month, mostly from retail investors.

Entrepreneur Vivek Ramaswamy, the executive chair of Strive, is a vocal critic of ESG and claims that, unbound from ESG constraints, U.S. energy stocks would soar 2X or 3X in value over the next two years.

With Europe facing energy rationing this winter, many agree that this is a poor time to be depressing energy valuations, thereby suppressing energy investment.

ESG funds are also under fire from the left. Progressives contend that many of these ESG funds don’t do much to promote socially responsible goals, but rather seek to profit off investor demand for the feel-good label. Evidence? The largest ESG funds, like iShares's US ESG Aware ETF (ESGU), include about 90% of the stocks in the S&P 500, with similar weights. Their performance, likewise, is nearly identical to SPY's.

That's a pretty low bar. But it doesn't prevent these ETFs from charging sizeable fees for the privilege of being an "ESG investor."

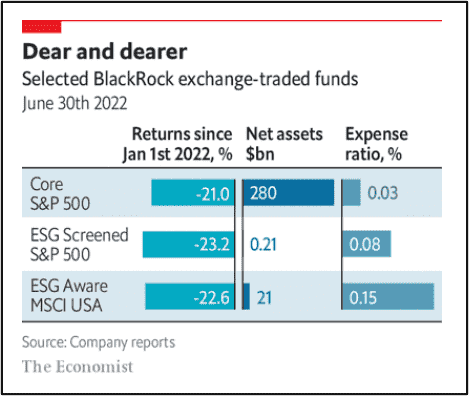

On average, ESG ETFs have 43% higher fees than conventional ETFs. BlackRock's ESG Aware fund, for example, charges fees that are 5X higher than those of its Core S&P 500 fund.

The same criticism is directed at rating agencies, who are of course pocketing a large share of this gigantic fee stream. About 160 providers create and sell ESG ratings data. MSCI is, by far, the most popular.

According to Bloomberg Intelligence, 60% of all retail investment money flowing into ESG funds globally has gone into funds built using MSCI's ratings. According to UBS Group AG, 40% of all these fees go to MSCI alone. Quite simply, the recent investor stampede into ESG has been a bonanza for MSCI. Its price soared from 2019 through 2021--though lately it has been sinking.

Let's use MSCI to revisit our "low bar" point about ESG from a different direction. MSCI gives the iShares ESGU fund an AAA rating. No surprise there. But MSCI also gives SPY an AAA rating! What gives?

If you look at the distribution of component firms in these two indexes, you have to squint a bit to see where they differ. The share of these funds' holdings with below-BBB ratings differ by only 5 percentage points.

Sure, this difference is a big deal for the 5% of large-cap firms who find themselves dropped--and for a larger share of firms who find themselves underweighted. They're howling.

That's what's fueling the conservative fire. But it's also a disappointment for progressives, who may have hoped that these funds are overhauling capitalism. Meanwhile, rating agencies like MSCI profit handsomely from selling its ratings to the funds, the cost of which is borne by investors. And that annoys everybody.

In short, the criticism is coming from all sides.

So what is ESG, anyway? That’s the thing: No one really knows. The term was coined in 2004 in a U.N. Global Compact report called Who Cares Wins, which made the case for integrating "ESG factors" into the investment process.

Reading this report, you will encounter a basic definitional puzzle. At times, it suggests that ESG is about firm practices that will benefit the world--like cutting carbon emissions or eliminating worker accidents or helping local communities--presumably at substantial cost to the firms. At other times, it suggests ESG is about practices that are all in the firm’s own long-term self-interest.

So which is it? Here’s where the straddle starts. On the one hand, most individual investors (and blue-state politicians) who drive the ultimate retail demand for ESG care about saving the world.

They want policies with teeth, not just enlightened self-interest advice for CEOs. On the other hand, rating agencies know full well they can’t tell pension portfolio managers to ditch their fiduciary responsibility to investors.

This may seem to be a hopeless roadblock. But wait, there’s an out. What if we define firm self-interest over the very long term, say, the next 20 or 30 years? (BlackRock stresses the phrase “long term” when defending its most nebulous ESG ratings criteria.)

Firm CEOs may be excused for not understanding, as well as the experts employed by the rating agencies, what the world will be like in 2050. Moreover, consider this: The risks posed by that future world will include laws and regulations that are not yet on the books. The original U.N. document repeatedly invokes “increasing pressure by civil society to improve performance, transparency, and accountability, leading to reputational risks if not managed properly.”

The bottom line is this. By deeming laws and regulations expected tomorrow to be a reputational risk for firms today, the ESG raters claim to know in advance how our democracy will eventually rule on all these issues.

Firm CEOs routinely comply with ESG guidelines not because they agree with the ESG raters about their firm’s long-term interests, but simply because they want to avoid the immediate reputational risk posed by the ESG ratings themselves. In this sense, the ratings are perversely self-enforcing. They need no justification.

When firm CEOs defend their adoption of ESG standards as a means of serving the shareholders’ long-term interests, they are telling the truth. Bad press is bad for shareholders. But as Ramaswamy points out, by that logic ESG becomes little more than "a protection racket."

Now let’s move on the next definitional problem. Let’s say we’re on board with this overall project. We want to identify all risks, including those posed by public policy, that may affect a firm over the next several decades. How do we even begin such a massive task? How do we know which risks will be posed by the world in the year 2050? And how do we assess which risks are or are not already priced in by investors?

The answer is: You can't. These are arbitrary decisions. Philip Morris (PMI) made it onto the Dow Jones Sustainability Index (DJSI), because the raters decided the business of selling 700 billion cigarettes a year is not at any regulatory risk.

Coca-Cola has an AAA rating from MSCI--because the raters have decided that, while methane emissions are an emerging health hazard, obesity and type 2 diabetes are not.

And speaking of methane, what about McDonald's, a prodigious emitter of greenhouse gases? MSCI recently upgraded McDonald's rating to BBB because it dropped climate change from the list of issues the company needs to be worried about--though some utilities that emit much less are graded much more harshly. In May, S&P dropped Tesla (TSLA) from its broad ESG index (SPXESUP) due to poor workplace practices, despite the firm's leading global role in pulling drivers away from carbon-based fuel. But Exxon (XOM) remains on the index. Hmm? How do the raters weigh bad bosses against a warmer earth? Your guess is as good as mine.

That's another thing. If carbon emissions are the biggest problem, why do so many energy majors stay on so many ESG indexes? Apparently, the raters like to rate firms against their competition within their industry.

So if you're Exxon, you get to stay in if you're better than Chevron (CVX). This makes no logical sense. Risk is risk. If that means the whole industry going down, so be it. Why do raters have such little backbone? Simple. They want to keep most firms in all industries in the ESG index so that its return won't differ much from the entire market. They only go after the stragglers, presumably to put competitive "social pressure" on the industry.

If you suspect that the best efforts by teams of experts come to very different risk assessments, you are right. The rating agencies all start with the same range of concerns identified in the original U.N. report: environmental, social, and corporate governance issues.

But the methods they apply to measure risks across these issues show huge variation. One study of six rating agencies found that the agencies used 709 different metrics across 64 categories of risk. A mere 10 of these metrics were used by all six agencies.

Not surprisingly, the absence of any standard methodology results in ESG scores that vary wildly depending on the agency that creates them. Credit risk ratings have a 99% correlation across agencies, but ESG ratings align just over half the time. In January, Credit Suisse received a dismal 15% rating for corporate governance from S&P Global, far behind peers like JPMorgan and Goldman Sachs. MSCI gave it a single-A rating: an average score on par with the other two banks’. Refinitiv was the least critical, awarding Credit Suisse a governance score of 81%.

Firms like Credit Suisse that are awarded a wide range of scores by different agencies may be encouraged to cherry-pick the best ones in its communications with investors or the public.

Other firms may have fewer options. And firms wanting to get placed into the highest-rated ESG ETFs may have no choice but to figure out how to score well on the MSCI index, currently used in most of the “green” funds.

Finally, let’s assume away all the conceptual and practical problems with calculating these ESG ratings. Let’s say we really could devise a consistent, high-quality score. What social good would it accomplish? That's really hard to say. Most obviously, it provides a big incentive for large-caps to divest "problem" operations.

Energy majors are divesting dirty refiners in the Mideast, for example, so that these are now regulated by the Iraqi and Nigerian governments. This hardly makes the world a better place. And some firms, after being devalued due to ESG stigma, may just decide to stay there so long as they have no big new capex plans. Many investors will be happy to buy into them and reap the higher returns.

IMO, the best way out of this mess would be to get rid of ESG. All of it. Not just the "S" and the "G," but also the "E." Companies are in the business of generating long-term value for their investors. This mission ordinarily aligns with the public interest.

When it does not, we have a forum that acts in the public interest, and it’s called the government--federal, state, or local, depending on what the issue is. If, for example, you want firms to cut carbon emissions to benefit the public (to eliminate what economists call their "negative externalities"), then do everything you can to enact a carbon tax. That's direct, logical, transparent, and democratic. Everybody can debate the issue, and then vote.

ESG, on the other hand, is indirect, illogical, obscure, and fundamentally undemocratic. It's also corrupting our politics. Do we really want to see separate groups of blue and red states battling each other over whose pension funds are going into whose vision of future governance?

It's crazy. Individual investors are free to have their own opinions about where they think the world is heading. And if you think we ought to be governing differently, then you can try to change current policy. Failing that, don't coerce others to invest the way you would like.

| To view and search all NewsWires, reports, videos, and podcasts, visit Demography World. For help making full use of our archives, see this short tutorial. |

* * *

ABOUT NEIL HOWE

Neil Howe is a renowned authority on generations and social change in America. An acclaimed bestselling author and speaker, he is the nation's leading thinker on today's generations—who they are, what motivates them, and how they will shape America's future.

A historian, economist, and demographer, Howe is also a recognized authority on global aging, long-term fiscal policy, and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

Howe has written over a dozen books on generations, demographic change, and fiscal policy, many of them with William Strauss. Howe and Strauss' first book, Generations is a history of America told as a sequence of generational biographies. Vice President Al Gore called it "the most stimulating book on American history that I have ever read" and sent a copy to every member of Congress. Newt Gingrich called it "an intellectual tour de force." Of their book, The Fourth Turning, The Boston Globe wrote, "If Howe and Strauss are right, they will take their place among the great American prophets."

Howe and Strauss originally coined the term "Millennial Generation" in 1991, and wrote the pioneering book on this generation, Millennials Rising. His work has been featured frequently in the media, including USA Today, CNN, the New York Times, and CBS' 60 Minutes.

Previously, with Peter G. Peterson, Howe co-authored On Borrowed Time, a pioneering call for budgetary reform and The Graying of the Great Powers with Richard Jackson.

Howe received his B.A. at U.C. Berkeley and later earned graduate degrees in economics and history from Yale University.