R3: REQUIRED RETAIL READING

March 10, 2011

RESEARCH ANECDOTES

- JCP began testing price increases almost a year ago on women’s private label apparel and to a lesser degree on men’s. Management found that customer response to raising pricing on opening or sharp price point goods was met negatively. On more aspirational product there a was a bit more forgiveness in the consumer’s acceptance. While just a small test, the results are certainly telling for those that sell deep-value opening price point goods.

- Macy’s noted that March trends have started off well, following a similar trend to February. Recall that the Easter shift has yet to occur which will ultimately lead to negative sales trends in March and disproportionately better trends in April. Management also noted that early and sporadic efforts to increase prices in certain areas have been met with little resistance and in some cases are actually helping to raise overall AUR’s.

- With strength in the sporting goods channel across just about every category (including golf), the industry is becoming increasingly focused on the latest ‘untapped’ opportunity – the youth consumer. At recent presentations, DKS management addressed this reality highlighting a strategy that includes efforts from both UA and NKE. The reality here is that while the youth consumer has not evolved overnight, but the industry is seeing increasing demand from the 8-12 year-old customer.

OUR TAKE ON OVERNIGHT NEWS

Kate Spade's Web Site Amps Up Edit - Kate Spade unveiled a redesigned Web site Wednesday, adding greater editorial content to its previously e-commerce-focused site. The new katespade.com will fuse a 50-50 ratio of shopping and editorial, according to digital marketing manager Cecilia Liu. Previously editorial content occupied just 15 percent. Now, when users arrive at the homepage, they are welcomed with a split screen that gives them the option to “shop” or “play.” The latter takes them to an image-driven, behind-the-scenes world of the brand. Consumers will also be able to engage in content such as company projects, partnerships, events and ad campaigns. <WWD>

Hedgeye Retail’s Take: Brand created content remains a key and growing aspect of a differentiated customer experience. And, if done well the consumer will not even realize they are being seduced/induced to make a purchase!

Asics Launches 33 Lightweight Running Shoe - Asics introduced a lightweight, minimalist running shoe collection that encourages natural foot movement in its new 33 by Asics collection. Inspired by the fact that 33 joints in the foot allow it to move efficiently, 33 by ASICS styles features the GEL-Blur33 to debut in April 2011 and the Rush33 available in June 2011, both in select stores. "We're excited to introduce this new collection for the consumer looking for a lightweight, minimalist style," says Brice Newton, Running Footwear Manager. "We have been encouraging natural foot movement with our Impact Guidance System (I.G.S.) for years, and this is an opportunity to showcase out latest adaptation with 33 by ASICS." <SportsOneSource>

Hedgeye Retail’s Take: For those who thought lightweight running was coming to an end, think again. Asics, New Balance, and Nike have all released new and innovative product in the last week.

City Sports to Launch New Private Label - City Sports is launching a premium collection of private label running and training apparel, called CS Designed by City Sports, according to The Boston Herald. Prices range from $15 to $45 with offerings extending from shirts, shorts and sweatshirts to bras. City Sports, which has 18 stores on the East Coast, originally launched its CS private-label line five years ago, but began an overhaul of the line last year. "We felt like we weren't serving (customers) well enough," Chrissy Durden, head of design, told the Herald. The slogan for the collection is, 'Love It For Life.' <SportsOneSource>

Hedgeye Retail’s Take: With just 18 stores there’s no reason to believe that any retailer can’t be in the private label business.

U.S Retailers Look to Europe - There’s a renaissance under way among U.S. web retailers targeting Europe for e-commerce growth, according to data and analysis contained in Internet Retailer’s newly published Top 300 Europe research guide. Some U.S. web merchants such as eBags.com have tried selling online in Europe in recent years, but pulled back because of problems with unexpectedly high operating costs, language barriers, international payments processing and other issues. But today U.S. web retailing companies that are selling successfully in Europe—or have ambitious plans to create a viable European e-commerce business over time—aren’t doing it just from the U.S. And they aren’t doing it on a shoestring budget. <InternetRetailer>

Hedgeye Retail’s Take: Clearly the easiest and fastest way to go global, e-commerce has also become a way for domestic brands to test the waters on a brand’s acceptance in international markets. This goes beyond sales and actually helps to define broader market opportunities.

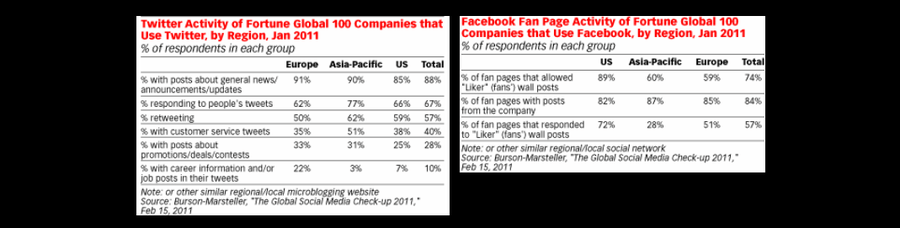

Marketers Move Toward Engagement on Social Media - Companies and marketers are more comfortable on social networks and have started to engage more authentically and build communities with other users on the sites. PR firm Burson-Marsteller analyzed the social media presence of the Fortune Global 100 for its “Global Social Media Check-Up 2011” and found that 25% of companies worldwide are using all four major social media platforms: Facebook, Twitter, YouTube and blogs. Eighty-four percent are on at least one platform. Twitter, specifically, saw major growth compared to 2010, as 77% of companies around the world have Twitter accounts, up from 65% last year. As companies get beyond the idea that they “just have to be on” social media platforms, they are becoming more active on these sites. <eMarketer>

Hedgeye Retail’s Take: Still much to do here with social media, marketing, and ultimately conversion. Most exciting is the idea that “fans” or “Twitterers” actually opt-in to their brand affiliations, adding a layer of responsiveness not seen with traditional media.