This note was originally published at 8am on March 07, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“For every promise, there is a price to pay.”

-Jim Rohn

Paying The Price is what hard working Americans do every morning. They take responsibility for their families. They are accountable for their actions. They’ll also be paying for their government’s promises at the pump this morning.

If you didn’t know that The Inflation is what you get when your government promises the entire world to devalue its currency, now you know. In order to calculate the price of The Petro-Dollars look no further than the price of The Petro and the price of The Dollar.

Here’s what those two prices did last week:

- The Petro = UP another 6.7% week-over-week taking its 2-week move to +17.6%

- The US Dollar = DOWN another -1.1% week-over-week hitting new YTD lows (DOWN 8 of the last 10 weeks)

Now someone who is in the business of obfuscating the facts will tell you that the price of The Petro-Dollars raging to the upside has to do with something other than the debauchery of the dollar. Of course it does – everything that adversely affects the marketing message of Washington, DC must have to do with someone else – that’s the un-American way.

Pointing the finger at some nut-job wearing shades in Libya just makes the marketing message easier. Since speaking at the American public on economic matters has turned into a world class game of politics, we should expect nothing less. On NBC’s Meet The Press yesterday, President Obama’s newly minted Chief of Storytelling, Bill Daley, reminded the world how Washington’s finest think about risk management plainly:

“Most people don’t know what they are talking about… The President knows…”

OK. Thanks Chief.

We will un-humbly submit that, on Global Macro economic matters, US Presidents and their crony economic advisors haven’t known what they don’t know for at least a decade. That’s a long time. That’s a problem.

Back to those stubborn little critters called real-time market prices that we use to illustrate the problem, here’s what else happened in the US as a result of the US Dollar being devalued last week:

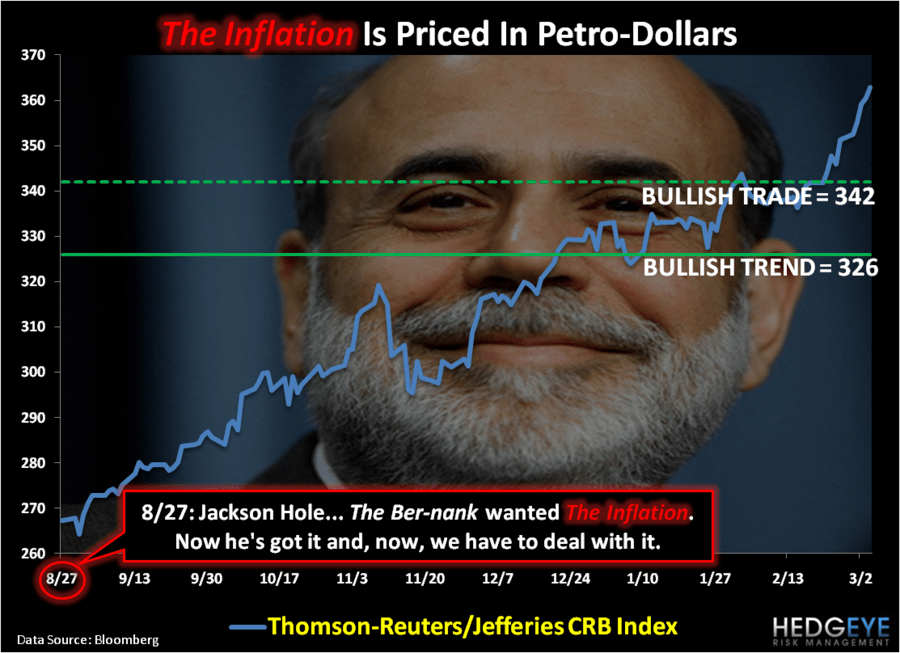

- CRB Commodities Index (19 components) = +3.1% week-over-week to close at a fresh weekly closing high for 2011 of 362

- Price Volatility (VIX Index) = flat week-over-week, holding its +22% gain above its February 18th YTD low of 15.59

- US Stocks (SP500) = +0.15% week-over-week to close at 1321, -1.7% lower than its YTD closing high of 1343 (also established on FEB18)

Altogether what this means is that since the US stock market stopped making higher intermediate-term highs on February 18th, the market has started to price in Slowing US Growth assumptions as US Inflation Accelerates.

For readers of our work, this shouldn’t be a new theme. Our 3 core Macro Themes at Hedgeye have been calling for Global Growth Slowing as Global Inflation Accelerates since October of 2010.

Our call on Accelerating Global Inflation’s impact on both Emerging Markets and Bonds is best captured by the #1 Economics headline on Bloomberg this morning: “Global Bond Rout Resembling 1994 As Inflation Exceeds Rates” – so, globally, people get it. The question is what will it take for US stock-centric consensus to finally get it?

Don’t fool yourself by letting some of the Fed’s Fiats fool the media most of the time, whether you look at the stock market performance divergences in US Equities or abroad, Mr. Macro Market is pricing in Global Inflation Accelerating, big time.

US S&P Sector Performance divergences for 2011 YTD:

- Best Sector = Energy (XLE) +14.78%

- Worst Sector = Consumer Staples (XLP) +0.92%

Global Equity Market Performance divergences for 2011 YTD:

- Best Countries = Ukraine +14.3%, Russia +13.8%, and Greece +12.2%

- Worst Countries = Tunisia -22.7%, Saudi Arabia -19.6%, and Dubai -17.1%

Obviously when presented with these prices on a real-time basis, the fundamental takeaways are crystal clear:

- Countries, Sectors, and Companies that get paid in The Petro-Dollars are getting paid by The Inflation

- Countries, Sectors, and Companies that don’t have pricing power are taking it in the margin

- Citizens are getting plugged

If this continues, the global economic risk management scenario starts to look a lot more like the 1970s than it does anything that most investors have had to wrestle with for the last 30 years. Stocks aren’t in the area code of “cheap” if inflation finds its way into margin and multiple compression.

The best way to fight this is by breaking the gigantic promise that America has made to the world – cheap moneys forever. If we start promising the world more hawkish monetary policy, the US Dollar will stop being debauched. That, in turn, will deflate The Inflation. And I’ll be the first in line to start investing more of my 49% position in Cash (versus 58% on Monday of last week). Paying the lower price works for me.

My immediate-term support and resistance levels for the SP500 are now 1315 and 1333, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer