Conclusion: We remain bullish on corn for the intermediate-term TREND duration as the confluence of perpetuating inflation, spiraling demand, and supply shortage indicate that corn prices will continue to rise.

Position: Long corn via the etf CORN

We added our on and off again long position in corn yesterday via the etf CORN in the Hedgeye Virtual Portfolio. As a reminder, we have been bullish on corn on an intermediate-term TREND basis since August of last year, when we initiated our first long position at $26.27. With the US dollar making lower lows, it is necessary to point out that corn has a -0.52 correlation to the US Dollar over the last three weeks. As a food crop with inverse correlation to a sinking US Dollar, investors would be remiss not to notice that inflation is present and will persist. Corn futures are up +10.8% YTD and up +67.9% over the last twelve months.

According to the United Nations Food & Agriculture Organization, record food prices will be sustained this year due to high oil prices and smaller crops. Corn is facing a serious supply shortage in the year 2010-2011 as corn output is estimated at 814.3 million tons while corn demand will flirt with 836 million tons. Looking thoroughly at supply and demand fundamentals, we have good reason to be bullish on corn. Here’s why:

On the supply side, corn is facing a shortage as climate change and natural disasters have decreased production. Moreover, cold weather continues to delay planting in the world’s largest supplying country. The US harvest represents nearly 55% of world exports and 39% of the global corn output in the 2010-2011 year. Unfortunately, the US has a lot of uncertainty surrounding its corn output due mainly to a legitimate concern that La Nina is forecast to cause heavy rainfall in the northern US plains as well as Canadian prairies. Though La Nina is expected to strike in the US, you can bet your buck on it that this will threaten the global harvest of corn and result in tightening global supplies. It is certainly a stark reality that the US could see a third yearly deficit for corn.

Despite the potential decrease in the global supply of corn, the demand for the crop continues to trend higher. When the US Department of Agriculture reports tomorrow, we expect to see a reduction in their estimates for the world stockpile, as demand increases in part due to the recent political turmoil in North Africa and the Middle East. Rising demand is corroding US corn stocks and a recent surge in ethanol demand—due to runaway crude oil prices—isn’t quite helping. Dating back to January, the Environmental Protection Agency agreed to let refiners increase their corn-based fuel additive in gasoline from 10% up to 15% for automobiles made in 2001 or later. Ethanol continues to eat away at the US supply of corn. According to a Feb. 9th USDA estimate, approximately 43% (4.95B out of the 11.6B bushels) of corn demand in the US is for ethanol use. With rising demand and an insufficient corn supply, there is plenty reason to be bullish on corn.

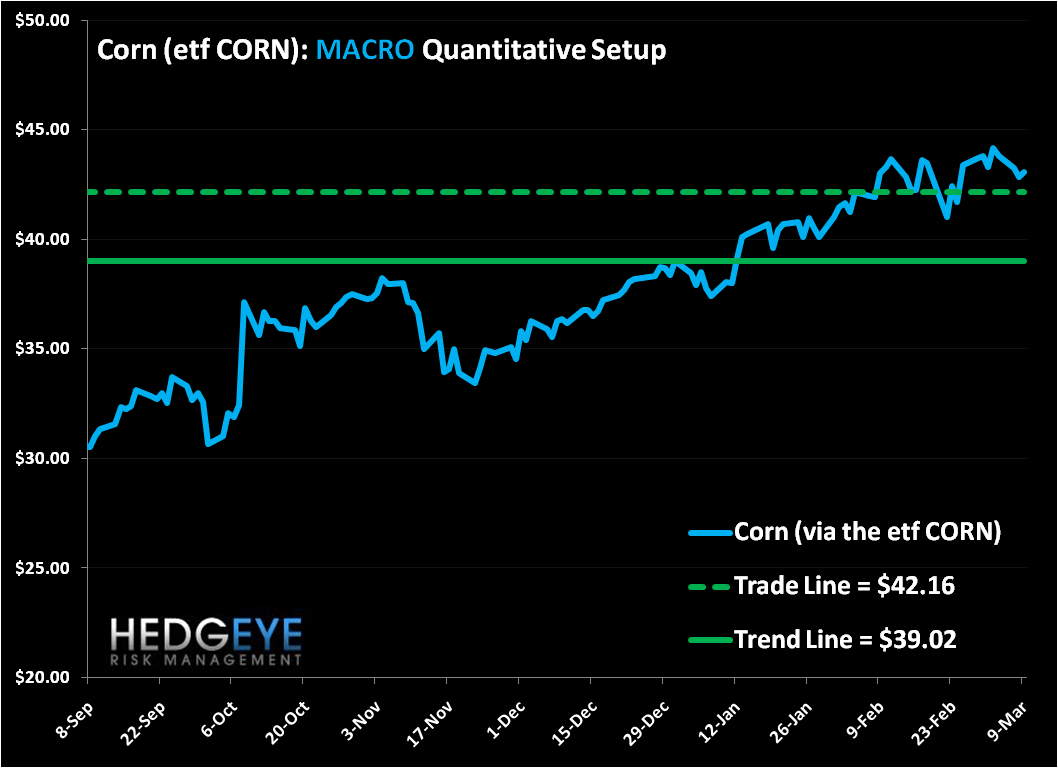

CORN was added into the portfolio at $42.74. From a quantitative setup, CORN is bullish on both a TRADE and TREND duration with no upside resistance, TRADE line support at $42.16, and TREND line support at $39.02.

Daryl G. Jones

Managing Director