This note was originally published at 8am on March 04, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“He is able who thinks he is able.”

-Buddha

When I started this firm, I had a simple goal – to democratize the risk management process of a hedge fund. What does that mean? That means showing the world exactly what it is we do, real-time, in a transparent and accountable way.

What does a hedge fund do? You’ll get a lot of different answers to that question – and as industry supply of hedge funds continues to expand, you’ll get more hedge funds who really don’t do what I do – hedge. Some strategies are simply levered-long versions of mutual funds that charge higher fees. Those hedge funds tend to blow up when markets stop going up.

Enabling Success in a hedge fund model is best achieved by having short positions that don’t hurt you when the market goes up. It’s a trivial exercise to buy something when everything is going up – that’s called beta. Managing losses is the key to this game – not chasing relative returns.

I don’t run money anymore, and a lot of people still ask me why. Three years ago, I thought I might eventually go back to doing it again – not anymore. I’m having too much fun building a real company with real cash flows. I absolutely love reading and researching so that I can put myself out there every morning. The challenge for me isn’t how much money I make, it’s how big of an arena I can play this game in.

I’m certainly not walking through these thoughts for any other reason than this is what I am thinking right now. I only have 45 minutes to write you these missives every morning – so I have to roll with what’s in my head. That requires a risk management process in and of itself – editors!

Enabling clients to look inside our risk management process seems to be the most empowering part of what we do. In order to Enable Success in this business, I think you need to let independent minds explain their research perspectives so that you can weigh them against your own. Whether our research is top-down, bottom-up, or quantitative – it seems to elicit plenty of feedback. Constant feedback enables success too.

How have we enabled this research platform to deliver an 81.6% batting average on the short ideas since inception in 2008? It certainly hasn’t been by sitting on my positions. Short-And-Hold isn’t a repeatable strategy across market cycles inasmuch as Buy-And-Hold isn’t. If you want to compound positive absolute returns on the short side over time, you have to keep moving.

Enabling Success on the short side of your portfolio is also driven by finding asymmetric opportunities. Since I attach the Hedgeye Portfolio at the bottom of this note every morning, you can monitor this real-time. But the upshot of it all is that you can witness a raging bull-run in US stocks and, at the same time, find ways to make money on the short side. If you broaden your scope, there’s always a short selling opportunity somewhere.

When I was younger, I was pigeon-holed into following US Retail and Restaurant stocks – so automatically, I was handcuffed to fishing in the creek that was in my area code. I was in the right place at the right time however, because 2000-2002 were bearish US stock market tapes, so there were plenty of names that were going down. Timing, like gravity, matters.

As I get older, I’ve simply broadened my horizons to fishing in oceans around the world across asset classes. At the same time, I’ve expanded my research team to 40 people (the largest team I managed at a hedge fund was 6).

Enough about that. I just felt like writing about it this morning. I think it’s important to be transparent about what it is we do.

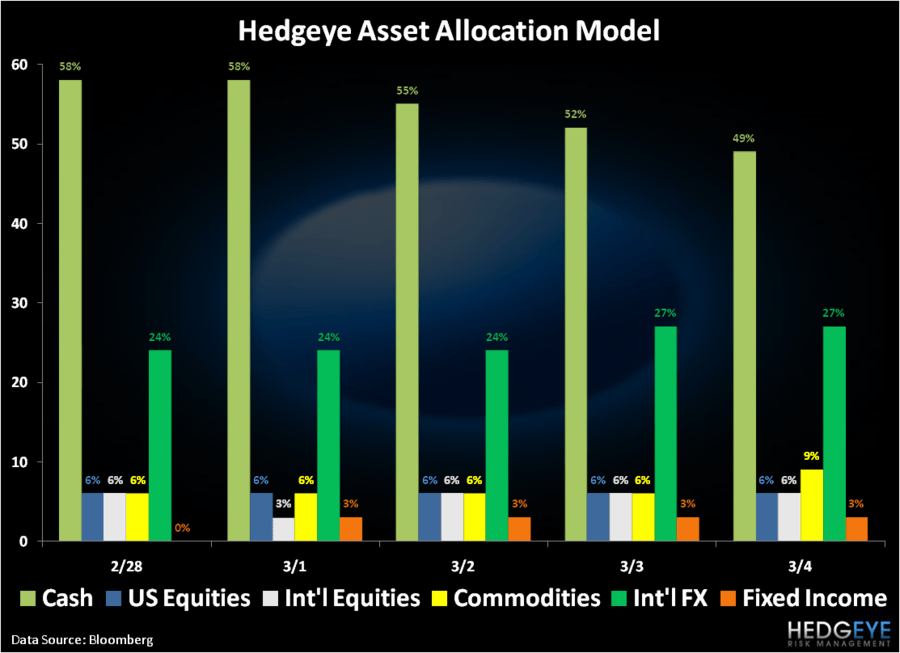

Since I only have 15 minutes left, here’s what I’ve been doing this week in the Hedgeye Asset Allocation Model:

- Reduced my cash position from 58% to 49%, taking advantage of some lower prices earlier in the week

- Expanded my invested position in International Currencies (Chinese Yuan and Canadian Dollars) as the Buck Burns

- Expanded my invested position in German Equities (EWG) where we remain bullish

- Bought back Gold on yesterday’s correction (GLD)

- Stayed long Oil and Grains (OIL and JJG)

- Stayed long US Healthcare (XLV) – my favorite US Sector alongside Energy

On the long/short side of the Hedgeye Portfolio, the main investment theme remains being long of The Inflation:

- Long Stocks with top line leverage to The Inflation (bought Petrobras (PBR) this week)

- Short stocks without pricing power whose margins get jammed with The Inflation (McDonalds (MCD), Target (TGT), etc.)

- Short Bonds and Emerging Markets – The Inflation is bad for them

Yes, there are some names in the Hedgeye Portfolio that aren’t working – there always are. There are also names that don’t always fit the top down and quantitative themes we’re focused on like a glove. These are names that my analysts like on either a turnaround or operating basis (SBUX, WEN, IGT, etc.).

Altogether, Enabling Success in terms of asset allocation, security selection, or net exposure is really best achieved managing your mistakes so that they don’t suppress your ability to generate repeatable absolute returns across market cycles.

My sincerest thank you to all of you who have enabled this platform to thrive. We don’t have to wake up every morning looking for some central planner in government to help us employ people. In an industry that is in dire need of evolution, you’ve enabled us to be the change we want to see in the world.

My immediate term support and resistance levels for the SP500 are now 1318 and 1342, respectively.

Happy birthday to my baby girl, Callie.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer