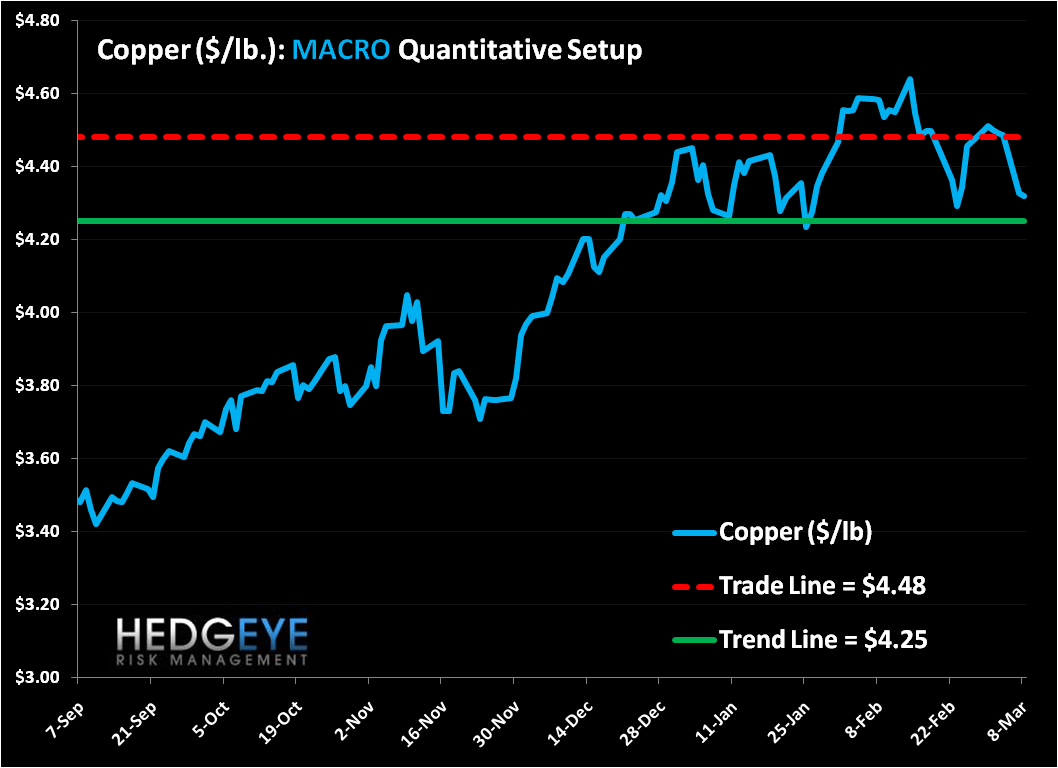

Conclusion: Price momentum is slowing in copper. The industrial metal is now bearish on TRADE duration and that has our attention. The fundamentals – supply and demand – confirm the price breakdown; thus, we do not see the pullback in copper as a buying opportunity

China consumes ~40% of the world’s refined copper – 4x as much as the U.S. Historically, copper prices and Chinese growth have been positively correlated. However, just as at a point higher oil prices are bad for economic growth, so are higher copper prices. The chart below illustrates this point. The Chinese stock market and the price of copper closely mirrored each other for the first half of 2010. But when copper crossed over $4.00/lb in October 2010, the two diverged meaningfully. At a point reflation becomes inflation, and inflation hampers growth.

The method through which higher prices stymie growth is lower demand. Consumption of copper in China peaked in early 2010, and has trended down since:

As consumption slows, inventories build. Here is what that looks like in China:

What about the developed world? After China, the largest consumers of refined copper are the US, Germany, and Japan. Here’s what consumption of copper looks like in those countries:

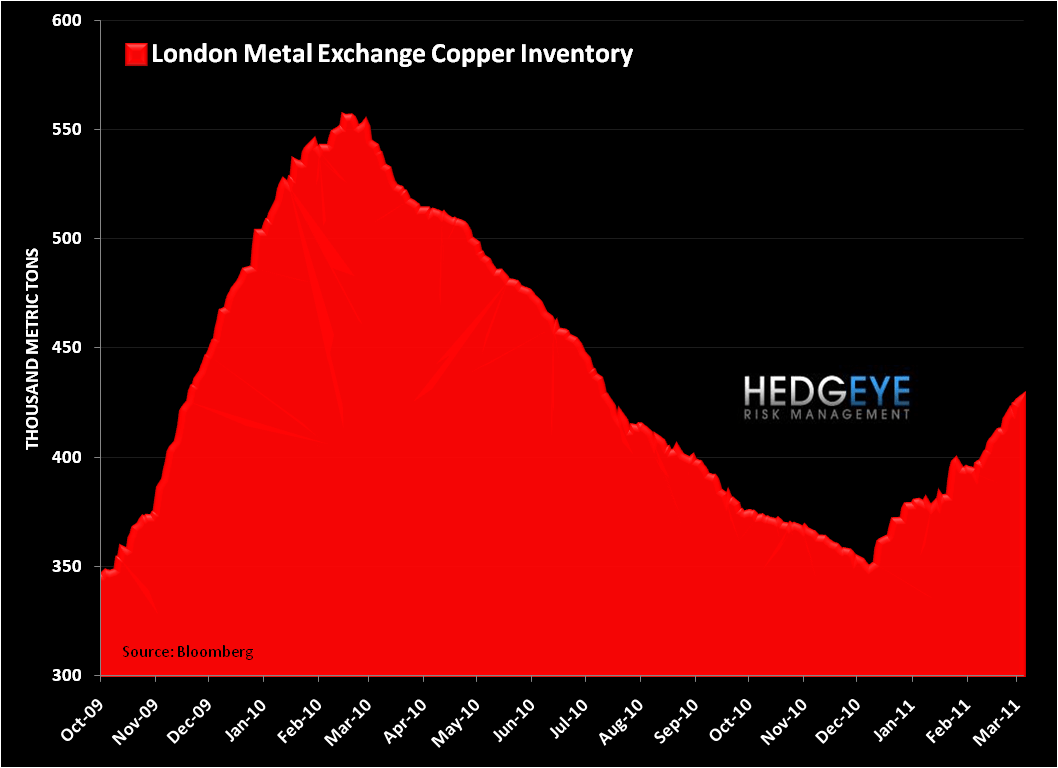

Obviously, developed economies cannot be relied upon to pick up the slack for a marginal slowdown in Chinese copper consumption. And recently copper inventories at the largest copper warehouse in the world – the London Metal Exchange – have built aggressively. When China slows, copper inventories build:

Lending to the inventory builds, copper production (mining) is strong, increasing 7% in 2010 year-over-year:

Inflationary pressures (copper included) have forced the Chinese to tighten monetary policy, leading to slower growth. Slower growth has led to a decline in copper consumption, though we have to not seen the impact of that feed through to the price of copper until very recently. We contend that copper traded away from the supply – demand fundamentals beginning in late 2010, and simply inflated. After all, the correlation between the USD and the price of copper is -0.80 over the last year.

If inflationary pressures subside and copper returns to the fundamentals, lower demand and higher supply will take the metal lower. We will be watching the TREND line of support ($4.25/lb.) closely. If that line breaks, look out below.

Kevin Kaiser

Analyst