The U.S. shortfall is overshadowing the stronger-than-expected results in Europe and APMEA.

For the second consecutive month, MCD’s same-store sales results fell short of street expectations in the U.S. while exceeding consensus estimates in Europe and APMEA. The company’s comps came in up 2.7% in the U.S. relative to the street’s 3.6% estimate, up 5.1% in Europe versus the street at +3.6% and up 4.0% in APMEA, much better than the street’s +1.8% estimate.

Trends in Europe have remained solid for the second consecutive month after decelerating sharply in December. Although two-year average trends decelerated nearly 70 bps in February on a calendar-adjusted basis, this was expected after the more than 400 bp sequential improvement in January.

MCD’s APMEA segment posted its third consecutive month of accelerating two-year average trends in February. The company’s +4.0% comp growth was particularly impressive given the fact it was lapping a+10.5% comp from February 2010.

Despite these strong results internationally, MCD overall results are being overshadowed today by the lower-than-expected U.S. numbers. Although MCD is a global company, MCD’s U.S. segment still accounts for about 45% of the company’s total operating income and investor sentiment still seems to be driven largely by the U.S. story.

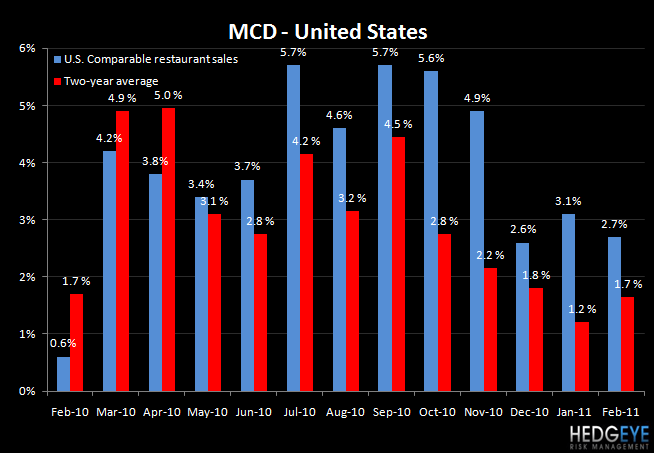

Two-year average trends in the U.S. moved slightly higher in February, up nearly 20 bps to about 1.7% (on a calendar-adjusted basis). Although some investors may be encouraged by this sequential improvement, I continue to think people are too bullish about MCD’s momentum in the U.S. as evidenced by the company’s posting another monthly comp result below expectations.

I continue to believe MCD’s comp trends will slow as we progress through the year and the reported March same-store sales result will likely turn negative as the company faces its first difficult monthly comparison of the year. In March 2010, MCD reported a +4.2% comp relative to -0.7% in January and +0.6% in February of 2010. Even if the company can maintain its two-year average trend from February, it would imply a -1.6% comp in March. For reference, MCD has not posted a decline in monthly same-store sales growth since January 2010.

The comparisons will remain difficult for the balance of the year, particularly in the summer months when the company laps its initial smoothie/frappe rollout. MCD has said that 2-3% comp growth is necessary in the U.S. to maintain margins in 2011 as a result of commodity inflation. If the company can maintain two-year average trends for the remainder of the year, it implies a 0.5% decline in FY11 same-store sales growth in the U.S. and I would not be surprised to see two-year average trends decelerate from current levels. Either way, I would expect MCD’s U.S. comp results to fall short of investor expectations in FY11.

Howard Penney

Managing Director