GS downgraded WMS and trashed the sector. Their slot estimates are factually wrong but are their concerns warranted?

Goldman Sachs sent shock waves through the gaming investment community yesterday with the release of its annual slot survey. Smaller than expected slot budgets, waning Wide-Area Progressive (WAP) demand, and more competition were cited as reasons to be cautious on the stocks. The firm was particularly negative on WMS and actually downgraded the stock to sell.

While we are not sure WMS is a sell given the favorable long-term outlook for this sector, we’ve articulated the view that the company is in danger of losing some share in calendar 2011. GS’s survey corroborates that to some extent. However, we must take the slot company responses with some caution. Firstly, the number of participants and the participating operators in the survey change each year, so the results each year aren't exactly apple to apple comparison of sentiment changes within the same group. In last year’s survey, WMS was cited as the clear winner in the survey, yet from Q4 2009 to Q4 2010, its market share was essentially unchanged. IGT was considered somewhat of a loser in last year’s survey, yet its market share only dropped 1%. In terms of stock performance, WMS has dropped 24% since last year’s GS survey was released up until the day before this year’s survey while BYI and IGT only fell 7% and 5%, respectively.

The reaction yesterday may have been extreme but we’re still a little wary of WMS over the near term. We do like IGT and BYI – IGT is a better near-term story because it’s safer (margin levers) but BYI is a better 12-18 month story. Both should be sequential market share gainers as we move through the year.

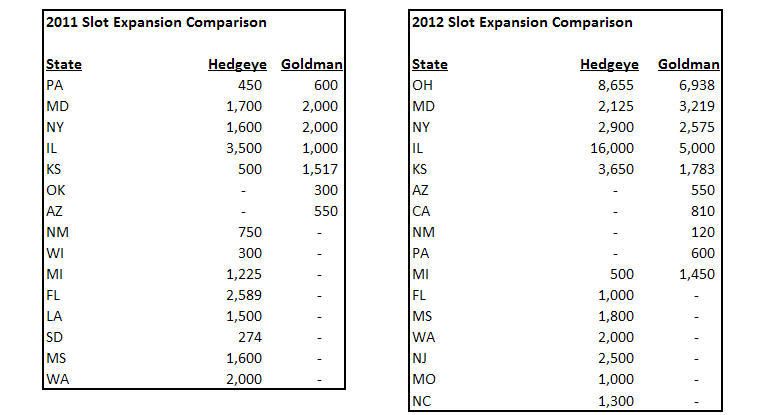

In terms of Goldman’s industry conclusions, we would caution investors on putting too much stock on operator responses regarding budgets. We stand by our 55k estimate for calendar 2011 replacement demand versus GS at 47k. More importantly, we are pretty sure GS’s slot estimates for new casinos and expansions are just flat out wrong. They appear to be off by 10k units in 2011 and 20k units in 2012. Here are the discrepancies:

The other important issue is wide area progressive where GS seems to be overly focused. Yes that business is waning but they ignore that a big reason for that is the growth in other pricing models such as fixed daily fees and straight revenue participation. These are actually higher margin pricing schemes because there is no jackpot expense.

We continue to believe that replacement demand is uncertain but priced in to the stocks. IGT seems to be the best positioned over the near term because they maintain the most margin levers should replacement growth fail to materialize. BYI seems to have the most upside over a 12-18 month time horizon given the likely technology-driven, sequential pickup in ship share off of a low base and low valuation. WMS is well-positioned long term but could continue to hit bumps in the road as market share normalizes at a lower level.