In general, commodities continue to gain in price with this past week bringing a more broad-based gain in week-over-week growth. Many restaurant stocks are hoping for an abatement or moderation in prices ahead of 2H11 (having given up on 1H in many cases). That notwithstanding, prices march higher.

Cheese prices merit a mention once again this week not due to any major week-over-week move but because of both DPZ and PZZA reporting recently. Below, I provide some commentary on cheese from both management teams provided during their most recent respective earnings calls:

DPZ:

Yeah, so the forward curve and kind of looking at about three different sources right now have cheese actually easing a little bit through the rest of the year. We're at almost $2 right now. And so, our expectation is that we're going to see a little bit of easing, to give you on cheese. We've talked about this in the past, we've got a contract in place that basically reduces the volatility on cheese moves by about a third. So about two thirds of increases or decreases in cheese are passed through to our system.

I think the kind of consensus forecast out there right now for cheese are in the $1.70 to $1.75 range. And – you know so what you're looking at is kind of a $0.25 to $0.30 move and I think we've said in the past a $0.40 move in cheese is equal to a point at the store level P&L.

PZZA:

We expect the favorable impact of early year sales results to substantially mitigate the unfavorable impact of currently projected commodity cost increases, most notably cheese, throughout the remainder of the year.

DPZ is 95% franchised and, as such, management claims a degree of insulation from commodity costs. Of course, to the extent that price needs to be taken and royalties slow, the company is not immune from inflation. Add to that the inevitable impact of higher gas prices (up 6% week-over-week!) and inflation is meaningful to company and franchise revenues alike.

Looking at the chart below, the trend in cheese prices seems to be levelling out. Nevertheless, even if cheese prices were to trend horizontally throughout the rest of the year, at it’s most benign, cheese price inflation would be 13%.

Beef prices are a concern for almost all restaurant stocks. Given the increasing demand for meat on a global basis, the impact of natural disasters, the increase of corn prices and, of course, the downward trajectory of the dollar, beef prices look set to continue downward. For steakhouse concepts like MRT, RUTH, and TXRH, this is a concern. The concepts that are most able to pass on price to the customer will best weather this storm, while the concepts most dependent on price point and traffic for top line growth will likely suffer.

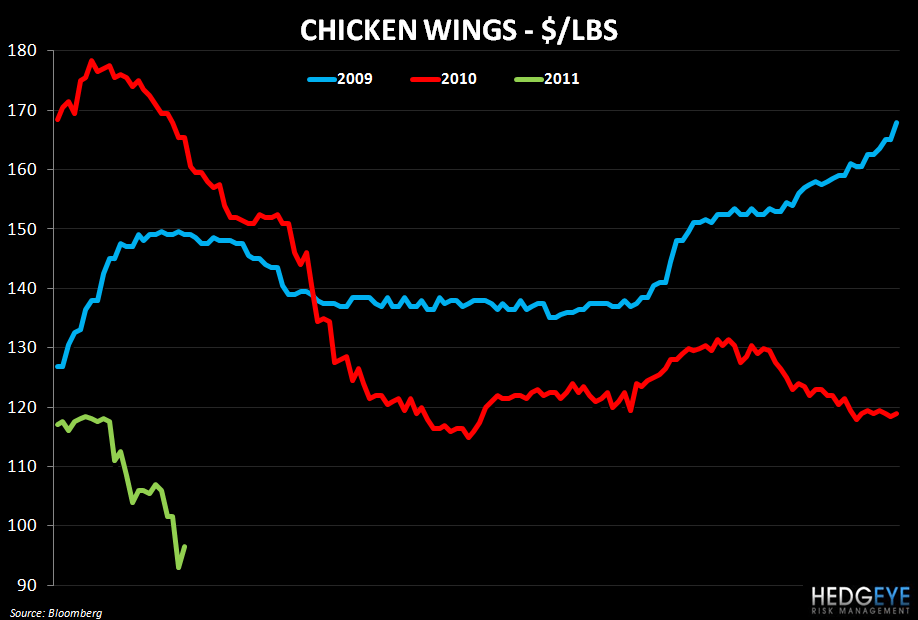

Chicken wing prices definitely deserve a callout again this week. The 5% week-over-week decline in wing prices spells further good news for BWLD margins.

Oil prices have been capturing all of the headlines of late and with good reason. The obvious implications for retail gasoline prices in the United States impact consumer discretionary stocks and restaurants in particular. As the chart below clearly shows, the inverse correlation between CBRL’s stock price and Oil over the past couple of weeks has been extremely high. CBRL is especially sensitive to gasoline prices given that its customer is typically derived from highway traffic. However, I suspect that other restaurant chains such as TXRH, CAKE, SONC, and many others will be impacted by this gain in prices at the pump.

Howard Penney

Managing Director