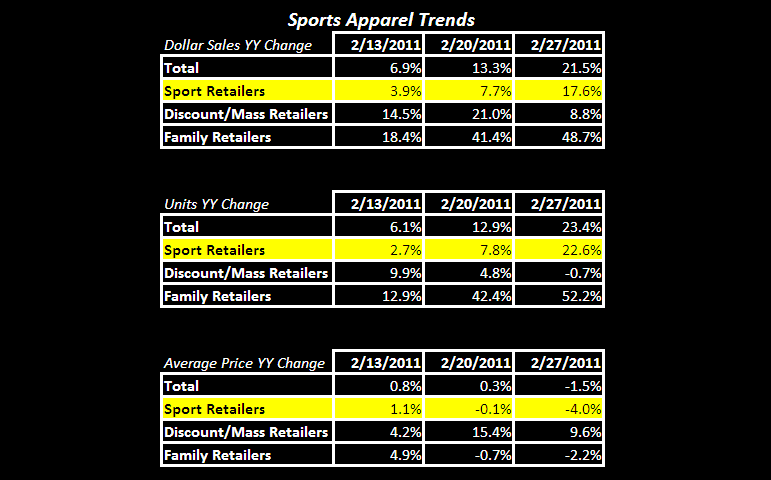

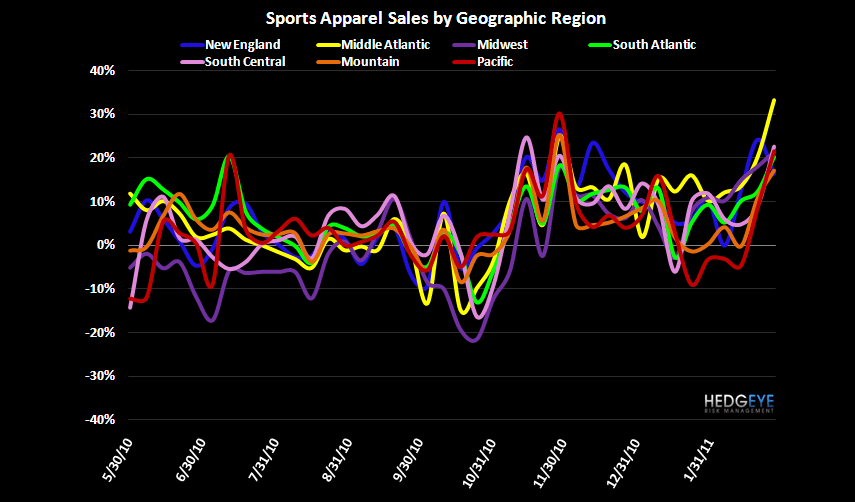

Weekly athletic apparel sales continue to accelerate on a sequential basis, confirming a rebound in sales activity through the end of February. Both the athletic specialty and family channels continue to strengthen while sales at the discount/mass channel slowed on the margin last week. Under the surface it’s worth noting that ASP’s decelerated in both the athletic specialty and family channel for the second consecutive week. However, unit volume more than made up for slight y/y ASP declines. Price increases in the discount/mass channel appear to be curbing sales momentum a bit, as unit growth has decelereated each of the past few weeks. Lastly, sales growth was robust across all regions with New England standing out as the only region to decelerate on a sequential basis. More noteworthy however, is the sharp rebound in the Pacific/Mountain regions that have been underperforming since mid-January. As always, week to week weather patterns can certainly have a short term impact.

Casey Flavin

Director