TODAY’S S&P 500 SET-UP – March 2, 2011

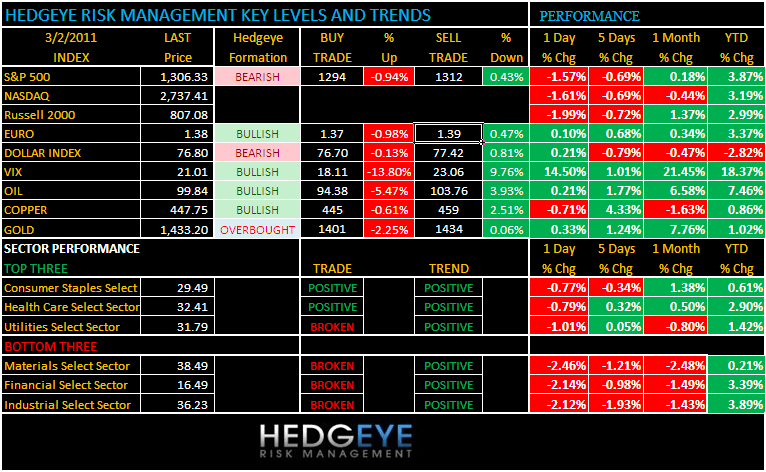

Equity futures have traded mixed to fair value, indicating a preference for risk aversion, amid rising geopolitical tensions. Violence in Iran yesterday, the world's fourth largest oil producer, helped push the Nymex oil contract back above $100/barrel. As we look at today’s set up for the S&P 500, the range is 18 points or -0.94% downside to 1294 and 0.43% upside to 1312.

MACRO DATA POINTS:

- MBA Mortgage Index Drops 6.5%; Purchases, Refis Down; MBA mortgage applications index fell 6.5% week ended Feb. 25.; Purchases slid 6.1%, refis down 6.5%

- 30-yr fixed rate 4.84% vs prior 5.00%

- 7:30 a.m.: Challenger Job Cuts

- 8 a.m.: Fed’s Hoenig speaks on Council on Foreign Relations

- 8:15 a.m.: ADP Employment Change, est. 180k, prior 187k

- 10 a.m.: Bernanke testifies before the House

- 10:30 a.m.: DoE inventories

- 2 p.m.: Fed Beige Book

- 2:15 p.m.: Fed’s Lockhart speaks on economic outlook in Atlanta

- 8 p.m.: Bernanke speaks on state, local challenges in New York, no Q&A

EARNINGS/WHAT TO WATCH:

- Yahoo! is in talks to dispose of its 35% stake in its Japanese J-V with Softbank, according to two people briefed on the matter

- Amazon.com threatens to sever ties with >10,000 affiliates in California amid a dispute with the state over proposed taxation of Internet purchases

- The U.S. Senate will vote on a stopgap budget bill need to prevent a government shutdown; it passed the House yesterday 335-91 vote; Ontario public hearings to discuss TMX/ LSE deal begin today

- FDA advisory panel members discuss draft report on menthol cigarettes

- NFL collective bargaining agreement is scheduled to expire tomorrow

PERFORMANCE:

We have 4 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

- One day: Dow (1.38%), S&P (1.57%), Nasdaq (1.99%), Russell 2000 (1.99%)

- Month-to-date: Dow (1.38%), S&P (1.57%), Nasdaq (1.61%), Russell (1.99%)

- Quarter/Year-to-date: Dow +4.15%, S&P +3.87%, Nasdaq +3.19%, Russell +2.99%

- Sector Performance: - Materials (2.3%), Industrials (2.2%), Financials (2.2%), Consumer Disc (1.8%), Telecom (1.7%), Tech (1.7%), Energy (1.5%), Utilities (1%), Healthcare (0.7%), Consumer Spls (0.5%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1590 (-2681)

- VOLUME: NYSE 1187.03 (-5.60%)

- VIX: 21.01 +14.50% YTD PERFORMANCE: +18.37%

- SPX PUT/CALL RATIO: 2.31 from 2.30 (+0.69%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 18.27 0.812 (4.649%)

- 3-MONTH T-BILL YIELD: 0.13%

- 10-Year: 3.41 from 3.42

- YIELD CURVE: 2.75 from 2.70

COMMODITY/GROWTH EXPECTATION:

- CRB: 355.18 +0.74%; YTD: +6.72%

- Oil: 99.63 +2.74%; YTD: +7.48% (trading +0.32% in the AM)

- COPPER: 450.95 +0.29%; YTD: +0.86% (trading -0.49% in the AM)

- GOLD: 1,428.55 +1.18%; YTD: +1.02% ( trading +0.34% in the AM)

COMMODITY HEADLINES:

- JPMorgan Takes Delivery of Almost 1 Million Tons of Sugar, Most Since 2009

- Cotton Jumps by Daily Limit, Rises for Fourth Day as Supply Remains Tight

- Crude Oil Advances a Second Day in New York on Middle East Supply Concern

- Farming in Australia Seen `Vulnerable' to Climate Change, Dryness in West

- Palladium Seen Rising 15% in 2011 as Russian Cargoes Drop: Freight Markets

- Gold Buying in China Jumps as Inflation Flares, Boosting Demand, UBS Says

- Copper, Corn May Slump on Mideast Unrest as Gold Jumps to $1,500, UBS Says

- China's Wheat-Growing Areas May Be Dry After Wetter-Than-Normal February

- Pan Pacific May Deepen Copper Production Cut on Scarce Raw-Material Supply

- Soybeans Advance as Rain, Flooding May Delay Brazil Harvest, Wheat Drops

- Glencore Is Said to Brief 11 Banks as Commodities Trader Weighs Share Sale

- Gold May Decline as Record Prices Prompt Sales, U.S. Job Prospects Improve

- Milk Powder Climbs to Record on China Demand, Increasing Global Food Costs

- Cocoa Arrivals From Brazil's Bahia Decline in Latest Week, Hartmann Says

CURRENCIES:

- EURO: 1.3806 +0.10% (trading +0.20% in the AM)

- DOLLAR: 77.049 +0.21% (trading -0.33% in the AM)

EUROPEAN MARKETS:

- FTSE 100: (0.43%); DAX: (0.66%); CAC 40: (0.82%) (as of 07:00AM ET)

- European markets fell on increasing concerns over the political unrest in the Middle East and North Africa.

- Bunds and Gilts were buoyed by safe-haven buying though investors remained cautious ahead of the ECB meeting on 3-Mar and the possibility of increased anti-inflation rhetoric.

- Peripheral debt was pressured ahead of Portuguese T-bill auction and by S&P's warning they may still cut Greece and Portugal's debt rating further depending on the outcome of EU leaders talks over the crisis fund.

ASIAN MARKTES:

- Nikkei (2.43%); Hang Seng (1.49%); Shanghai Composite (0.18%)

- Though off their lows for the day, Asian markets closed lower following yesterday's declines in the US markets as higher oil prices and the turmoil in MENA returned to front-and-center.

- China Railway Construction is among the biggest decliners, down 7.8% after saying it halted work on three projects with combined value of $4.24b in Libya.

- The Nikkei suffered its worst percentage drop this year.

- Airlines and automobile manufacturers led shares lower across the region, with All Nippon Airways down 3.05%, Cathay Pacific down 2.51%, Qantas down 2.15%, Toyota down 2.85%, and Honda down 2.49%.

- Sands China closed down 6.2% after Las Vegas Sands (LVS) said it received a subpoena from the SEC regarding its Macau operations.

- Yahoo Japan closed up almost 3.7% after Reuters reported Yahoo (YHOO) was in talks to sell its stake.

- India said it would hold local elections in five states between 4-April and 10-April; the states send a cumulative 116 lawmakers to the lower house of Parliament.

Howard Penney

Managing Director