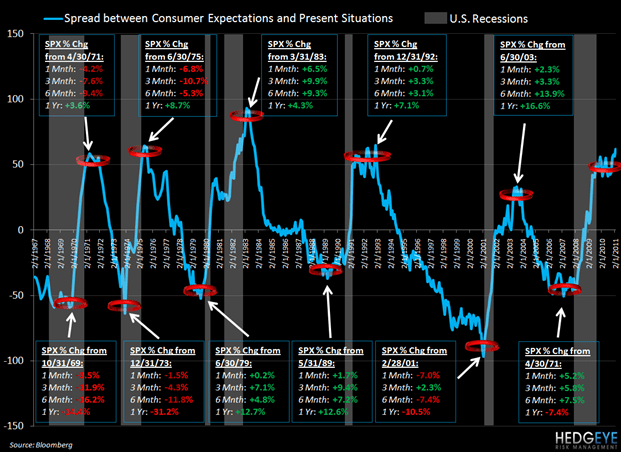

Headline consumer sentiment is on the mend, but there is once again a dramatic divergence between consumer expectations and present situation which is driving the over-all improvement. The divergence between the two is what we call the Optimism Spread.

The Conference Board Expectations Index has gained rapidly since the trough in February 2009 and is now merely 1% from its most recent peak of December 2006. Coincidentally, the Conference Board Present Situation Index has moved largely sideways since early 2009, remaining a staggering 76% off its most recent high of March 2007.

The topic of the U.S. consumer is foremost in investors’ minds and is of ten used by management teams to express when business may be good or bad in any given quarter.

The recent uptick in consumer sentiment is being driven by the increase in expectations of better times ahead and not by the “present situation.” On Monday, the inflated optimism was exposed for what it is as the government reported that “real” spending fell 0.1% in January, following a 0.3% increase in December and a 0.2% rise in November. Importantly, January’s decline was the first since April and puts real spending at 1.2% at an annualized basis in January 2011. We estimate that the current pace of annual spending needs to double to drive GDP growth above 3%.

Consumption drives approximately 70% of GDP and we have been uncomfortable with the bullish case for consumer spending since the introduction of the Consumption Cannonball theme in September of last year. We sometimes present themes that can are early, but in this case it is clear that there are acute risks pertaining to the consumer that are largely being ignored by investors. We are more comfortable with our belief that consumption is set to slow following Monday’s consumer spending data, and are further encouraged by the fact that Hedgeye’s bearish thesis on housing continues to play out. Although housing hasn’t spooked the market of late, if our Financials team’s forecast continues to play out as it has been, it will have a serious impact in 2011.

In January, personal consumption expenditure was weak despite a 1% surge in personal income. January’s gain was mainly due to a number of special factors including a $100 billion reduction in contributions for government social insurance. Social security withholdings were reduced as part of the Tax Relief, Unemployment, Insurance Reauthorization and Job Creation Act of 2010. Although employment grew by just 36,000 jobs in January, wages and salaries also expanded at a fairly strong and steady pace, increasing by 0.3%. The personal savings rate reached 5.8%; the first time since June 2010.

Rising food and energy prices are a drag on real spending and can influence expectations that the economy is getting better. In addition, the prospect of public sector cutbacks is looming large over broad swathes of the workforce. With so much inflation uncertainty inherent in the system today, why are consumers so much more about the future versus the current situation?

(1) Bernanke/QE is working?

(2) The republican takeover of Washington?

(3) Tax cuts?

(4) The jobs picture’s gradual improvement?

(5) The S&P 500 being up 5 of the last 6 months?

While our cautious stance on consumer spending appears warrented looking at the January data, it is too early to claim victory. Winter weather was a drag on January spending. As we look forward, anything less that 0.7% in personal spending for the next two months will likely lead to the consensus to reduce its GDP forecast.

Below, we attempt to interpret the usefulness of our Optimism Spread from a market standpoint and the results are interesting but less-than-conclusive. While the consumer’s rosy expectations have generally been prescient indications of recessions coming to an end, the track record from a market perspective has been less impressive.

The question I believe is most pertinent from here is whether or not we are in an economic environment that is more anomalous to the 70’s or the period following Volcker hiking rates and the ensuing equities bull market that played out as rates were cut to zero.

Howard Penney

Managing Director