In looking at the upcoming quarter for PSS after the market close on Wednesday, we remain positive on the fundamentals (in fact, Keith just added to the Hedgeye virtual portfolio). Making a call into the quarter for such a high-beta stock rarely sits well with us – especially for a company that is hardly afraid to miss a number. But the reality is that we’re seeing good signs out of PSS’ PLG business, and the comp on the core Payless business seems to be holding its own.

As a reminder, our call on this name is that its two primary growth brands (Sperry and Saucony – which account for about 30% of EBIT) are fueled by an annuity revenue stream out of the base business. Trends in those segments are nothing short of robust (see chart 1 below).

All in all, we’re at a loss of $0.15 this quarter versus the Street at ($0.19) – its seasonally lowest quarter of the year.

Next year we're shaking out between $2.00 and $2.10 vs street at $1.76 -- but will need some questions answered w the print.

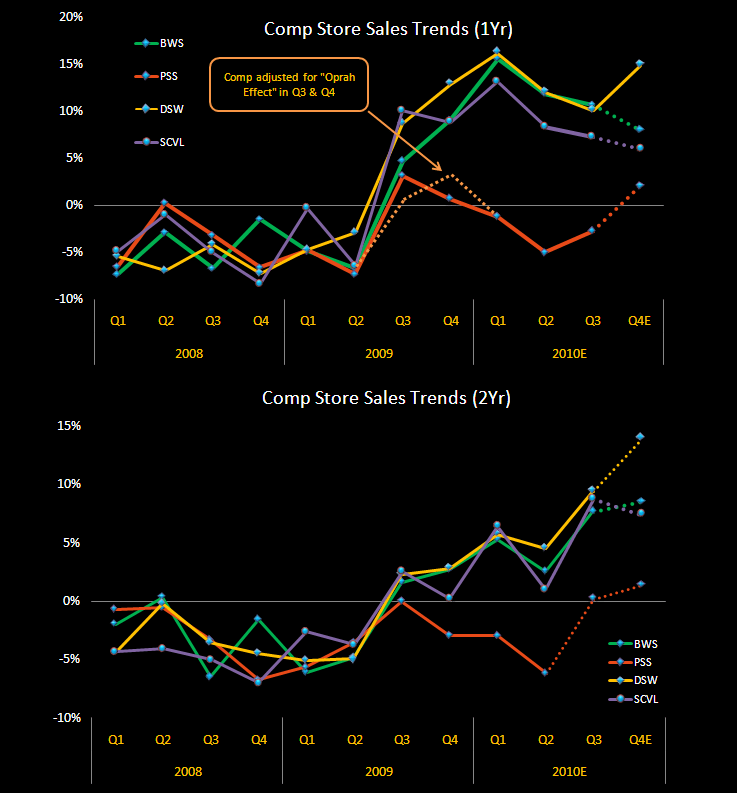

The charts below have had a good directional impact in the past