“The quality of the imagination is to flow and not to freeze.”

-Ralph Waldo Emerson

For those of you who dial into the Hedgeye Morning Macro Call every morning at 830AM EST, you know that the title and topic of this Early Look note is dear to my Canadian heart – The Flows.

In institutional investor speak, The Flows are where the fees are. For bulls, they foster the imagination. For bears, they focus the mind. The Flows represent your moneys. In a world “awash with liquidity” and sovereign debt, we don’t think you should trust. Bernanke Bubbles beware.

Last year, they flowed you into US Treasury Bonds and Emerging Markets. This year, outflow-you-go into the “safe havens” of US and Japanese stocks. Like the promise of Bernanke “buying bonds” in 2010, the promise of not “fighting the Fed” bears US stock market fruits from the heavens. Do not freeze men and women of the risk management gridiron. The chase for the last Dollar Debauched drop of equity returns is on.

The problem, of course, arises when The Flows run into these little critters called The Fundamentals. Understanding full well that our view of The Fundamentals is often 3-6 months ahead of Wall Street/Washington consensus (yes, sadly, they are now one and the same) is what it is – since October, our Global Macro view of the fundamentals remains Global Growth Slowing as Global Inflation Accelerates.

Thankfully, not every institutional investor understood the repercussions of Quantitative Guessing II (QG2) on Global Inflation Accelerating back then. Now those who bought US Treasury Bonds and Emerging Markets are being reminded that what flows into a said haven, flows out…

From EPFR Global, here’s the latest on The Flows (per their February 18th report):

- USA/Japan/Europe (Equities) - “Investors pumped $47 billion into equity funds in the U.S., Europe and Japan this year after pulling $17 billion in 2010 and $28 billion in 2009.”

- Bonds Funds - “Investors added $2.44 billion to bond funds globally this year as of Feb. 16, down from $11.1 billion during the same period in 2010.”

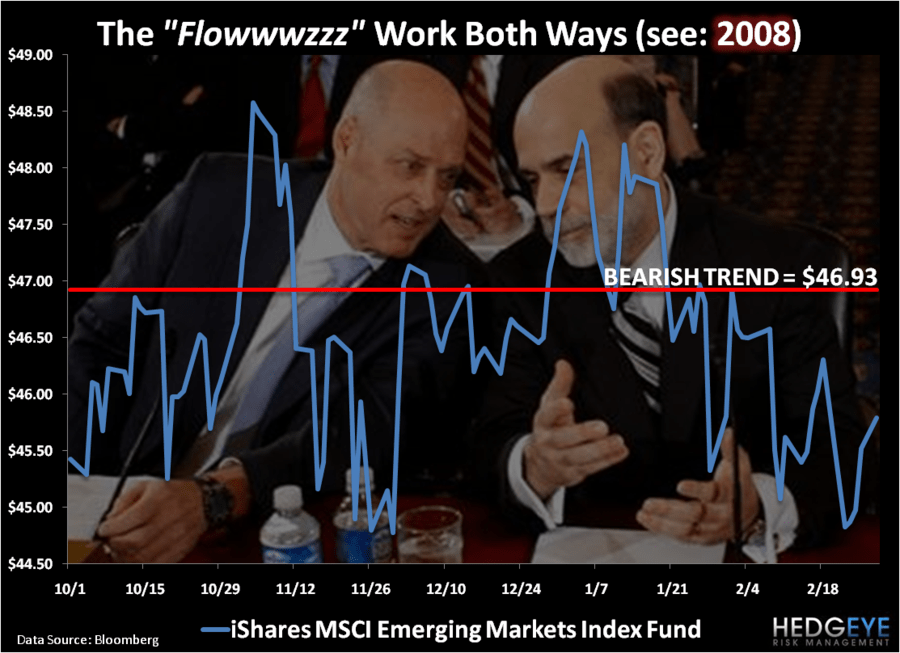

- Emerging Markets - “Investors pulled $1.9 billion from developing nation stock mutual funds in the week to Feb. 23, the fifth week of outflows.”

Now, as we like to say at Hedgeye, what happens on the margin in Global Macro matters most. And on the margin, The Flows into the stock markets of Developed Economies have been huge. The most important risk management part of that last sentence is “have been.”

How long can The Flows trump The Fundamentals? How much risk gets entrenched into an asset class when the storytelling starts to follow the natural confirmation bias of positive price momentum? How many times do we need to see this movie before we learn the lesson?

These are all questions that have a much clearer answer now versus then. Whether you look at the opportunities to short US and Emerging Market Equities into the peaks of fund flows of 2007 or shorting the mountain tops of a bond market bubble in 2010, history writes itself as of last price.

As a risk manager who is shorting things almost every day, I need to be really sharp on timing and price. While many institutional marketing messages preface their buy-and-hold strategy with “you can’t time markets”, we should all be very thankful for that – many of them can’t. What we’re doing is preserving capital and making probability-weighted decisions, daily, with a fundamental Global Macro research overlay.

On the scoring of Growth and Inflation, this morning’s Global Macro Grind has some positives, but more negatives:

POSITIVES

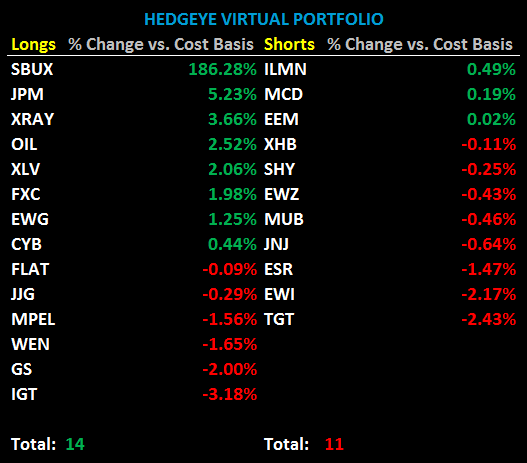

- Germany – unemployment fell to another new low of 7.4% and German Equities continued higher to +6% YTD (we’re long EWG)

- Canada – unlike US growth which was revised down again last week, Q4 GDP growth surprised to the upside (we’re long FXC)

- India – the government cut taxes and sent the stock market up +3.5% (we covered our short position in IFN at last week’s low)

NEGATIVES

- China – Producer Manufacturing Index (PMI) hit a new 6-month low of 52 last night (we’re long CYB as China continues to tighten)

- Mexico – Unemployment continued higher sequentially to +5.4% versus 4.9% last month (we’re short EWZ on Latin American inflation)

- Iran – Consumer price inflation (CPI) was up to +15.8% in JAN vs 12.8% in DEC (that’s before this massive oil spike and is instigating tensions)

- Japan – Industrial Production slowed again sequentially in JAN to +2.4% y/y vs 3.3% DEC (we covered our short position in EWJ last week)

- Spain – Consumer price inflation (CPI) was up again sequentially in FEB to +3.4% versus +3.0% in JAN (we have no position in Spain)

- USA – US Consumption in JAN, adjusted for inflation, was negative for the 1st month in a year (we’re short MCD, TGT, and XHB)

But there is no but in The Flows. They are what they are until they stop. All the while, I’m most certainly not going to freeze with a strategy to short-and-hold. For the last decade, that hasn’t worked inasmuch as buy-and-hold hasn’t . Not in a market where professional politicians are sponsoring a Burning Buck, The Inflation, and Price Volatility… We have America’s sad State of political leadership to thank for that.

My immediate-term lines of support and resistance for the SP500 are now 1311 and 1343, respectively. The US stock market should make another lower-high today – one that you should outflow from, provided that US Dollar Debauchery continues to sponsor Global Inflation.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer