Based on Q4 dollar RevPAR, January should've been stronger.

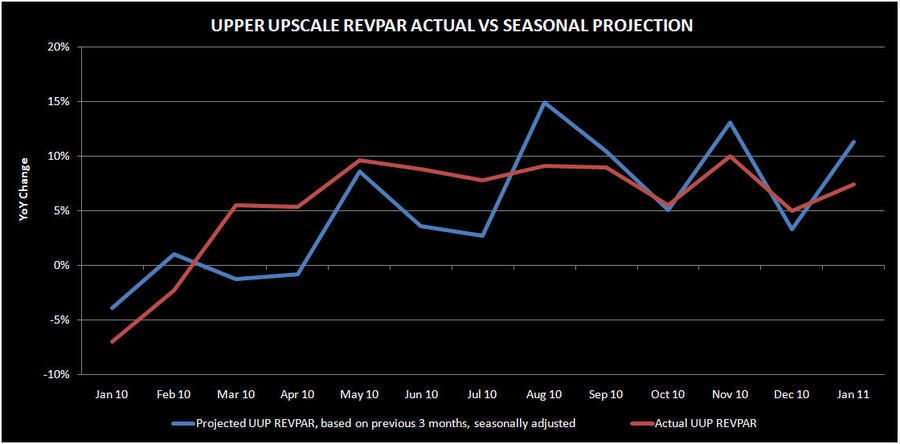

Following up on our 1/26/11 post, "HOTELS; BLAME THE WEATHER", January Upper Upscale Revpar grew 7.4% YoY. While that may appear strong on the surface, it was actually a deceleration from Q4. Seasonally adjusting Q4 dollar RevPAR produces January RevPAR growth 4 percentage points higher than actual. It's hard to believe poor weather could explain that magnitude of a miss. Given the high RevPAR volatility over the last three years, we track RevPar on a sequential, absolute dollar basis, adjusted for monthly seasonality.

Reflecting November-January RevPAR, we project RevPar growth of 10% for February 2011, assuming no sequential growth in seasonally adjusted dollar RevPAR. Anything below 10% will be indicative of a slowdown. Thus far, the weekly February RevPar have been trending a tad lower than that. We continue to believe that February will be the near-term peak for RevPar growth with contraction risk in Q2.