“As the shark lunged for his head, Louie bared his teeth, widened his eyes, and rammed his palm into the tip of the shark’s nose.”

-Laura Hillenbrand, "Unbroken"

That’s a quote from an outstanding non-fiction novel that I’m reading by Laura Hillenbrand titled “Unbroken: A World War II Story of Survival, Resilience, and Redemption.” It’s a story of a selfless American Olympian by the name of Louis Zamperini who sacrificed more than this modern day man can begin to comprehend. They’ll turn this into a movie – and if they do it right, it may win an Oscar trophy someday too.

The story of American Sacrifice is one that we all know well. Alongside our Trashing Treasuries and Housing Headwinds Macro Themes for Q1 of 2011, it’s also something that we talk about during each and every one of our research team’s Morning Meetings here in New Haven.

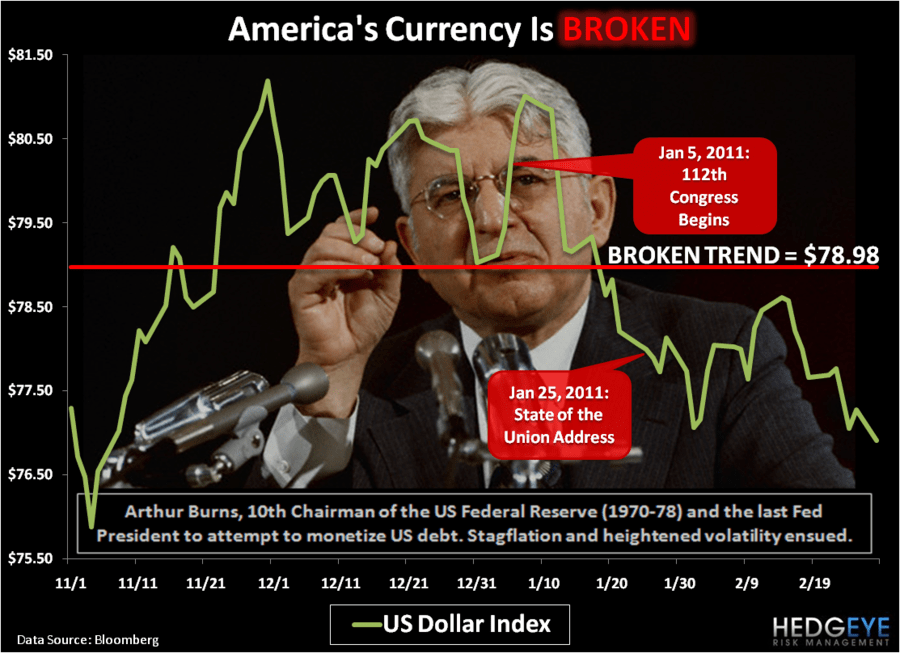

Fundamentally, we do not believe that this country’s political leadership (Republican or Democrat) has it in itself to deliver on American Sacrifice. Since the introduction of the 112th Congress, handshakes and promises to the American people of cutting deficits and debts have already been broken. The credibility of America’s currency is broken too.

What remains Unbroken is the passion and faith that Americans who aren’t tied to a Washington compensation structure hold in their hearts and minds. From Wisconsin to New Jersey, that’s what you see rising to a boil. If it takes punching these political sharks in the proverbial nose, so be it…

We recognize what Washington and Wall Street’s Easy Money Elite want. They want us to keep doing what we’ve allowed them to do since Nixon abandoned the gold standard. He, not unlike Charles de Gaulle, moved to a deficit and devaluation strategy so that he could win the 1972 election.

Washington wants us to roll over and take it in The Inflation. They want to fear-monger us. They want to sell us. They want to lunge at us with the price volatility born out of the crises that they created.

Well, that might work for a select amount of the compromised, conflicted, and constrained few. But it doesn’t work for me and it doesn’t have to work for you or The Rest of the World either.

China’s Premier announced to the world last night that he’s willing to sacrifice short-term growth for price stability. In the 12th Five-Year Plan, China outlined an economic growth rate expectation of 7% annualized from 2011 to 2015. Sure, if they wanted to drop free moneys from the Eastern heavens and perpetuate The Inflation that would consume their citizenry, they could. But they aren’t. The Chinese don’t have to be re-elected.

After all that America has been through to fortify its individual rights and civil liberties, it’s both frightening and sad to see a State-managed economy like China’s manage The Inflation with more respect than we do. Tomorrow you’ll have our Almighty Central Planner outline to the world that he sees no inflation – or at least he sees none in his conflicted and compromised calculation.

Ahead of The Ber-nank’s semi-annual report on US Monetary Policy tomorrow, the US Dollar Index is hitting a fresh 4-month low. Sadly, this is more of the same in terms of intermediate and long-term trends. The US Dollar Index was down another -0.5% last week. It’s been down for 7 of the last 9 weeks. It’s a mess.

Surely, the US Government will blame last week’s inflation on a nut-bar in Libya. But don’t disrespect for one minute that for the last 3 years The Rest of The World has started blaming us too. Standing as the world’s fiduciary of the world’s reserve currency isn’t the next entitlement that our professional politicians can abuse – it may very well be the last.

On a week-over-week basis, this is The Inflation and Price Volatility that The Ber-nank will ignore:

- US Dollar Index = DOWN -0.5% (down 7 of 9 weeks)

- CRB Commodities Index = UP +2.9% (hitting fresh 2-year highs)

- Volatility (VIX) = UP +16.3% (up 22.5% in the last 2 weeks)

In the face of inflation and price volatility, growth signals continued to slow week-over-week:

- US Treasury Yields = DOWN across the curve last week

- Copper = DOWN -0.9% (despite Commodities being up)

- Yield Spread = DOWN 9 basis points to +270 bps (10s vs 2s)

But, have no fear, the US stock market remains Unbroken from an immediate-term TRADE perspective:

- SP500 TRADE line support = 1309

- NASDAQ TRADE line support = 2760

- Russell2000 TRADE line support = 803

So, Bernanke is doing his job, inflating the stock market - and you have nothing to fear other than his fear-mongering itself. Right.

In the Hedgeye Asset Allocation Model, my teeth are barred with Cash and my eyes are wide open:

- Cash = 58% (up 3% week-over-week from 55%)

- International Currencies = 24% (Chinese Yuan and Canadian Dollar – CYB and FXC)

- Commodities = 6% (Oil and Grains – OIL and JJG)

- International Equities = 6% (Germany and Sweden – EWG and EWD)

- US Equities = 6% (Healthcare – XLV)

- Fixed Income = 0%

My immediate term TRADE lines of support and resistance for the SP500 are now 1309 and 1325, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer