Position: We are long oil via the etf OIL

Conclusion: We are long OIL in the Virtual Portfolio as price continues to confirm this position, but longer term, as history shows us, political liberalization could actually support growing production.

The price of oil is already indicating to us that the current turmoil in the Middle East will not be resolved in the short term. Since tensions heightened in Libya over the past week, the prices of most major grades of oil are up roughly $10 per barrel in just a couple of days. Today oil is flat after a volatile day of trading motivated by rumors surrounding the demise of Moammar Gadhafi.

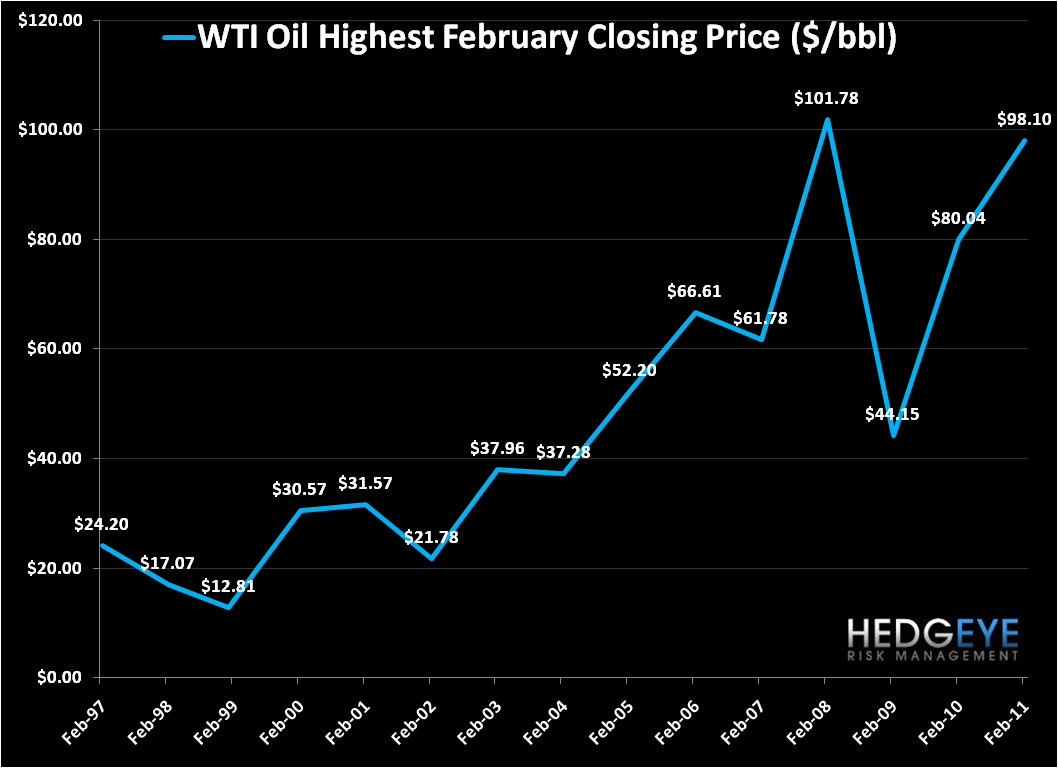

Further to this point, we’ve outlined in a chart below the highest closing price in February going back the last 15-years. Typically, February would be a relatively slower seasonal month for demand in the United States (the world’s largest consumer) as the need for winter heating oil diminishes and summer driving season hasn’t picked up. Interestingly, while the price of oil is still more than $40 from its all time high, it is very close to highest February close of $101.78 in February 2008. This abnormal and non-seasonal price movement emphasizes the powerful price move we are seeing.

On February 16th, we called out this potential impact of popular unrest in Libya and Iran in a note that underscored our long position when we wrote:

“We are starting to see Egyptian and Tunisian type popular tensions spread to some key oil producing states, which should provide a key support under the commodity. Specifically, both Iran and Libya have seen an increase in protests. This is relevant because, based on the most recent data, Iran is the second largest producer of crude oil in OPEC, at 3.7MM barrels of oil per day, and Libya is a sizeable producer as well at 1.6MM barrels of oil per day.”

Given that Libya is less than two percent of global production and that the IEA has over 1.6BN barrels of oil in storage, clearly the current price movement is about more than Libyan disruption. Even if Libyan oil production were completely turned off, the IEA has enough oil in storage to offset that lack of production decline for a full year. Further, it is estimated that OPEC collectively has between 4 – 6MM spare barrels of daily production. So, why has oil gone parabolic over the past couple days? Simply put: oil is now trading on fear.

In effect, this is fear that popular upheaval goes well beyond Libya and into more significant producers in the Middle East (like Iran) and that the ultimate outcome is a transition in government, or armed conflict, that leads to a broad decline in oil production. An associated fear is that OPEC ultimately doesn’t have the spare capacity they claim, which could lead to a global oil supply tightening quicker than most expect. Ultimately, this fear will continue to buoy and lead the world oil markets until we have some resolution or clarity in the Middle East, which certainly does not seem imminent.

Longer term there is a scenario, which certainly isn’t consensus on a week like this, that vast liberalization and democratization in the Middle East could be positive for oil production. Russia is probably the prime example of this occurring.

In the late 1980s, Russian oil production reached a peak of production of 12.5MM barrels of production per day. Due to a decline of investment during the Soviet era, Russian oil production gradually fell thereafter and had fallen to around 6MM barrels per day by the mid-90s. The collapse of the Soviet Union combined with a privatization of the oil fields initiated a turnaround in production starting in 1999. Currently, Russia is back to near peak production levels due to privatization and subsequent modernization of her oil assets.

Iraq looks to be on a very similar path to that of Russia. Not surprisingly, with the Iraq War and the ensuing chaos following the removal of Saddam Hussein from power, Iraq oil production fell dramatically and was mired in the 1.5MM barrels per day level of production until early 2007. By then, post Saddam Hussein modernization and investment started to pay off and Iraqi oil production began to climb. In January of this year, Iraqi oil production hit a post war peak in production of ~2.6MM barrels per day and is expected to be near 3MM barrels per day by year end, a level not seen since the late 1970s. In fact, as reported late last year in the Wall Street Journal, some Iraqis believe that growth in production could be meaningful in the coming decade:

“In all, Iraq hopes the work will boost output capacity from the current 2.5 million barrels a day to 12 million barrels a day in less than a decade. That would be a feat unrivaled in the history of the modern oil era. Last month, Fatih Birol, the International Energy Agency's chief economist, called Iraq a potential "game changer" for global oil markets.”

In fact, Royal Dutch Shell, who was awarded one of the Iraqi contracts last year, recently upped its Iraqi production from the Majnoon field from 45,000 barrels per day to 70,000 barrels per day. A small change, but incremental.

No doubt this is a long tail type scenario, and a lot would have to happen for Western Oil companies to up investment in less stable regions like Iran and Libya, but both Iraq and Russia do provide some credence to the idea that production, over the longer term, could grow if the ultimately outcome is the spread of democracy and rule of law.

Daryl G. Jones

Managing Director