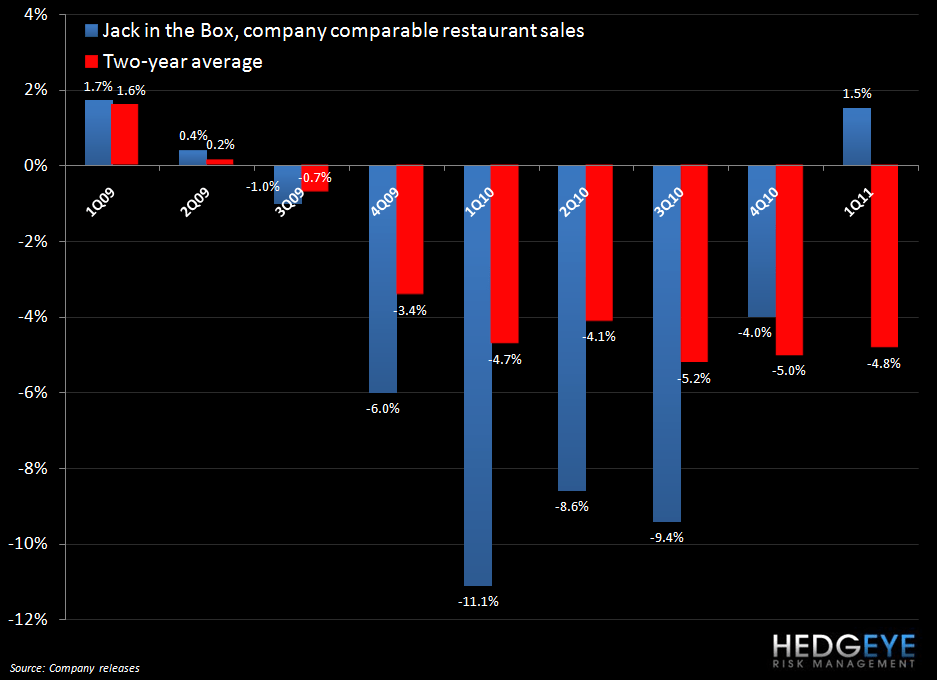

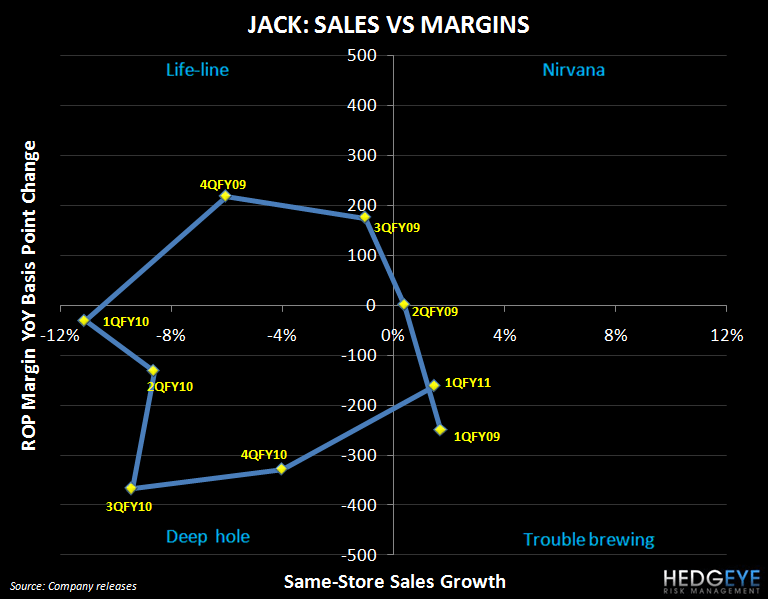

Fiscal 1Q11 earnings of $0.61 per share came in $0.13 per share better than street expectations (only about a $0.02 per share benefit from a lower tax rate), but the company slightly lowered its full-year EPS guidance to $1.40-1.65 from $1.41 to 1.68. Despite the better-than-expected same-store sales growth of +1.5% at Jack in the Box company restaurants (versus the street’s +1.2% estimate and management’s guidance of -1 to +1%) and the fact that 1Q11 marks JACK’s first quarter of positive comp growth at Jack in the Box after six quarters of decline, investors will likely be disappointed that there is no flow through to guidance from the first quarter earnings surprise.

Although management is likely being cautious, and maybe even practical, it will also be viewed negatively that the company did not raise the low end of its -2% to +2% full-year comp growth guidance at Jack in the Box company restaurants as a -2% result would imply a sequential slowdown in two-year average trends from 1Q11 levels. Given the changes in guidance, higher commodity costs are the primary driver of the lower earnings guidance for the balance of the year.

Below I outline the positive and negative offsets included in the current guidance versus the company’s prior outlook.

Positives:

- Qdoba system same-store sales growth now expected to be +3-5% (from prior guidance of +2-4%)

- Tax rate: targeting 35-36% (versus 37-38%)

- Anticipated refranchising gains: $0.70 to $0.82 per share (versus prior range of $0.66 to $0.78 per share)

Negatives:

- Commodity costs are expected to be up 3-4% (from prior expectation of +1-2%)

- Restaurant operating margin expected to range from 13 to 14% (had said 14 to 14.5%)

Neutral:

- Jack in the Box company same-store sales growth guidance unchanged at -2 to +2%

- New unit development plans are mostly unchanged (only expected to open 19 company-owned Jack in the Box restaurants versus prior guidance of 25)

- SG&A expense unchanged in the mid-10% range

We will be back with more details after the company’s earnings call tomorrow.

Howard Penney

Managing Director