VFC front-loaded a lot of good ‘ol fashioned optimism. But you need a lot of Hope and Luck to get ’11 guidance. The risk/reward here looks flat out bad.

VFC isn’t the kind of company that tends to surprise us on the average EPS print. After all, it’s a $14bn portfolio of brands (about the same size as Gap) that spans just about every relevant category out there. In other words, the company realistically should not dramatically outperform the industry, because it IS the industry.

We understand the ‘quality of management’ factor. But two days ago, if you’d have asked me what the probability is of VFC beating the quarter, AND taking up estimates to a level suggesting 10% sales AND EPS growth in 2011, I’d have said (and did say)…

“Even if they think they can do these numbers, there’s 87% of the year left to go. They do themselves no favors by doing this now.” That’s particularly the case due to VFC’s expectation for success in large part to a consumer and retailer-led price increase.

I sat here for two hours on this VFC model, and I legitimately cannot find a way to get above $7.00 for the year. I’m shaking out at about $6.45 (flat year/year).

Here’s what you’ve got to believe to get their numbers

- There has been only one year in VFC history where it printed 10% annual organic growth. That was 2006, where VFC benefitted from a healthy consumer, and solid organic growth from building out The North Face stores (which is a 2x gross-up in sales dollars from cost, to wholesale, to retail). In other words, '11 needs to be VFC's best year ever.

- The former algorithm from 2003-2008 was for hsd top line growth, split evenly between organic growth and acquisitions. There’s no mention of acquisitions now. That either means that the REAL expected organic growth is over the top of historical peak, or the company will come back with a deal and say ‘that’s included in our prior guidance.’ They’ve done it before, and the market was often split on sentiment.

- Levi’s remains rational in 2011. If VFC Jeanswear Coalition’s top competitor starts to buy market share, then there’s no way that VFC is hitting these numbers.

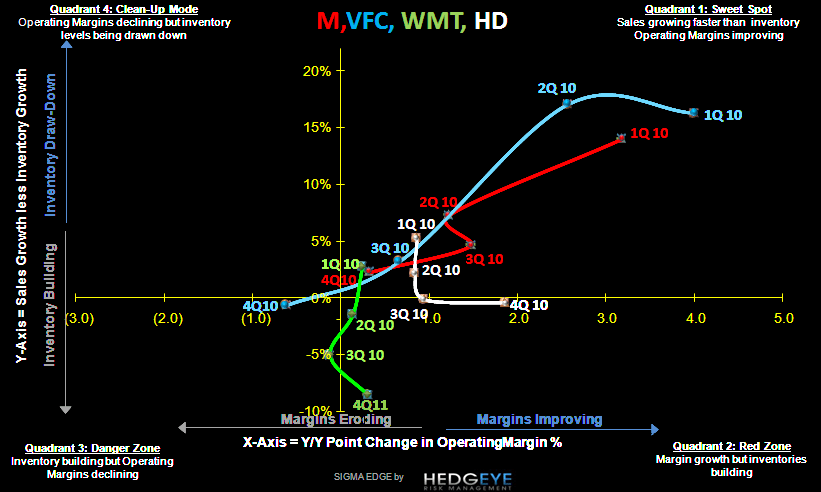

- The SIGMA looks awful. Check out the chart below. We show the past four quarters for Macy’s VFC, Wal-Mart and Home Depot – all companies that reported today. VFC not only is headed in an unhealthy place, but the yy comps starting quite difficult (ie squarely in ‘sweet spot’ for past three quarters. You've got to believe that they can turn this around -- and fast.

And lastly, I’ve got to point out something related to cost inflation that we published earlier today. It’s quite relevant here. There are three stages we think companies are (or are not and should be) concerned about cost inflation. Let’s go in order of simplicity.

1) Control what you can control. The companies see the same tape we do and where prices are headed, and they plan accordingly with their own procurement. Focusing solely on this will blow them up.

2) Workup a strategic plan as to how they think their supply chain partners will react when faced with a meaningful change in their cash flow. I’m referring to how a brand like Lee, Wrangler and North Face react when price is altered by Levi’s or Columbia, respectively.

3) In addition to the two preceding points, the most successful companies are planning for how a supply chain partner will look to squeeze when it’s hurt in other categories. For example…what happens if the ‘food inflation pass through’ is maxed out and Wal-Mart needs to face a food price increase at risk of losing additional traffic?

Why not push it through to more discretionary and highly fragmented categories like apparel and toys?

Go out and ask a CEO of a ‘basics’ apparel company if he has ever knowingly funded markdowns in fresh fruit. He’ll say no, and he’s not lying. He’s simply unaware.