This note was originally published at 8am on February 17, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We are firmly convinced that monetary and fiscal policy will continue to debase the dollar.”

-Ted Kelly (CEO of Liberty Mutual)

Liberty Mutual is an American insurance company that was founded in 1912 and currently sits at #71 on the Fortune 500 list. It has over 45,000 employees servicing global insurance products worldwide and has over $100B in consolidated assets. Their CEO made the aforementioned comment in a Bloomberg article yesterday by Noah Buhayar. No, Liberty didn’t pay me an advertising dollar for this paragraph.

Unlike The Ber-nank attempting to trade US Treasury bonds, this isn’t Ted Kelly’s first rodeo. He’s been CEO of Liberty Mutual since 1998 and his job is to manage bond market and duration risk. On the topic of real-time risk management, he went on to add that, “we are positioning our portfolio and our business to respond if inflation emerges.”

Notice Kelly didn’t say “when inflation emerges.” He said “IF” - and that’s a critical differentiator between a proactive risk manager (a portfolio manager) and a reactive one (a professional politician). Kelly isn’t alone in this line of thinking. Almost every world class risk manager in the world understands that governments that debauch their fiat currencies will impose an inflation tax on their citizenry.

The US Dollar Index backed off hard right where it should have yesterday. It closed down another -0.54%, keeping it below its intermediate-term TREND line of $78.98. Call me lucky or call me right in understanding how to manage risk around the price of the world’s reserve currency. Since starting the Hedgeye Portfolio 3 years ago, I’ve gone 18 for 18 in making profitable long/short calls on the US Dollar (UUP).

I’m not calling this out to pump my own tires. I’m calling this out so that the pundits who are out there cheering on Bernanke’s stock market inflation policy pay attention. Making calls on US Dollar declines helped predict bubbles in both US stocks (2008) and US bonds (2010). Sadly, unless President Obama starts listening to the likes of Ted Kelly, Bill Gross, and Jim Grant, it may very well take another US Dollar currency crisis to stop these Big Keynesian Central Planners in their tracks.

As a reminder, we first made our call on Global Inflation Accelerating in October of 2010, and from here on in we’ll be acutely monitoring the slope of inflation accelerating or decelerating with the following assumptions:

- IF we debauch the US Dollar, Global Inflation will accelerate

- IF we stabilize the US Dollar, Global Inflation will decelerate

That’s it. That’s the deep simplicity we’ve found in our multi-factor, multi-duration model. Remember, in principle Chaos Theory is grounded in uncertainty – so every risk management exercise starts with IF and every decision follows the THEN that’s driving correlation risk.

On our most immediate-term duration, some of the correlation risk associated with US Dollar Debauchery has burned off in the last 2 weeks. That’s primarily because the US Dollar was UP for the first week out of the last four. IF we debauch it from here, THEN that will change. Correlation risk gets fired up when the Buck Burns.

On the heels of yesterday’s US Dollar decline, here were some important Global Macro reactions to consider:

- Commodities – CRB Commodities Index inflated back up to its YTD weekly closing high level of 338

- Bond Yields – US Treasury Yields on the short-end of the curve popped back up to +0.84%

- Emerging Markets – Asian Equities ended their 3-day rally to lower-highs

Again, this isn’t complicated. Debauched Dollar is bullish for inflation (Commodities) and bearish for Bonds and Emerging Markets…

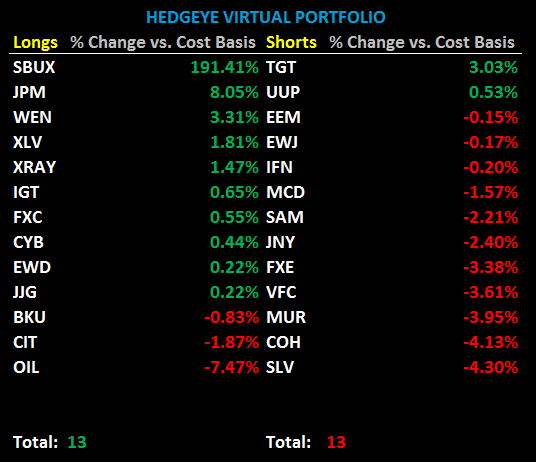

As you can see in the Hedgeye Portfolio (attached), alongside re-shorting the US Dollar this week, we re-shorted the following Macro positions:

- Indian Equities (IFN)

- Emerging Market Equities (EEM)

- Japanese Equities (EWJ)

Now as sure as the sun rises in the East, you can bet your Madoff that The Ber-nank won’t be talking about the interconnectedness that his Central Planning Policies and a Debauched Dollar have on Asian and Emerging Market currencies and/or their exports.

Let me illustrate this point (generally) with the example of how the USD is affecting South Korea:

- South Korean Won strength (born out of US Dollar weakness) = hurts SK Exports (50% of GDP)

- South Korean Import Price Inflation zoomed to +14.1% in January vs +12.7% in December = hurts SK Exporter margins

- South Korean Equities (KOSPI) have dropped every day this week and are now down -3.6% for 2011 YTD

South Korea’s stock market isn’t what we’d call an “emerging market.” Per capita GDP is 10x that of China and it’s an economy levered to both US Tech and Industrial demand (bearish leading indicators?). Since it’s the world’s 12th largest economy, the KOSPI recently moving to bearish TRADE and TREND in our risk management model is something worth paying attention to as you watch Bernanke and Geithner continue to erode the credibility of America’s currency today.

My immediate term support and resistance lines for the SP500 are now 1324 and 1339, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer