Initial Claims Climb Back Above 400

The headline initial claims number rose 27k WoW to 410k (25k after a 2k upward revision to last week’s data). Rolling claims rose 1.75k to 417.75k. On a non-seasonally-adjusted basis, reported claims fell 17k WoW. NSA claims in 2011 to date has been less volatile than typical.

We have been looking for claims to hit the 375-400k range and remain there or lower before unemployment begins to improve. That said, it is worth highlighting an important caveat. This recession has been different in that it has pushed the labor force participation rate down by ~200 bps, which has had a correspondingly positive improvement on the unemployment rate. In other words, the unemployment rate isn't really 9%, it's 11%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 11% actual rate as opposed to the 9% reported rate.

One of our astute clients pointed out the relationship between the S&P and initial claims shown below. We show the two series in the following chart, with initial claims inverted on the left axis.

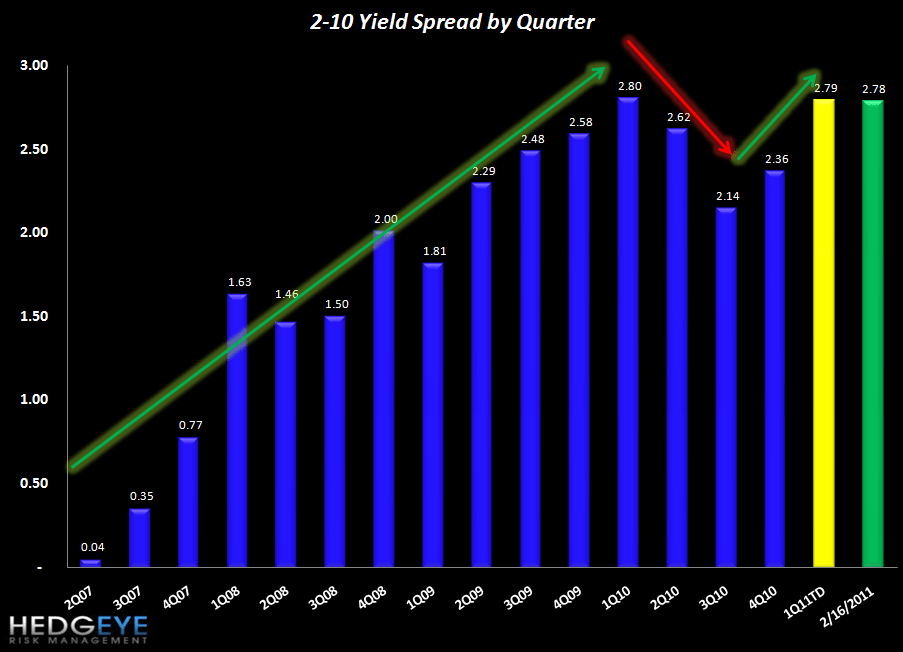

Yield Curve Continues to Widen

We chart the 2-10 spread as a proxy for NIM. Thus far the spread in 1Q is tracking 43 bps wider than 4Q. The current level of 278 bps is slightly tighter than last week (284 bps).

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur