Casual Dining results have been fairly mixed so far this earnings season. Knapp Track data shows that 4Q saw a period of sequentially slowing monthly same store sales trends. From 3Q to 4Q also, comparable restaurant trends slowed by 30 basis points. By contrast, a simple average of casual dining comparable restaurant sales reported for 4Q thus far shows a marginal improvement from 3Q. It will be interesting to see if 4Q results reported from here follow more of a negative sequential direction from 3Q.

In October, during the 3Q10 earnings call, CEO Bert Vivian effectively threw in the towel on the target of $2 in EPS for 2010. The more likely scenario, according to Vivian, is EPS of $0.57, which would imply EPS for the year approximately “a nickel less” than the prior $2 guidance. The Street is expecting $0.57 cents and while some casual dining companies have surprised to the upside, I think there is some downside risk to forward guidance given the drastic changes in the commodity markets since the last quarter. See my note, “THEY SEE INFLATION”, from last night for more details. Below I offer a quick run through of forward-looking statements from the October earnings call:

“We believe that both concepts are well positioned for the fourth quarter and we have our fingers crossed that the holiday season will be a good one.”

“We've been paddling pretty hard since our less than stellar first quarter to achieve our annual earnings goal of $2. While $2 is still possible, I would not assign a high probability to that outcome. The more likely scenario is about a nickel less.”

“New unit development will be very modest at the Bistro. We would like to allocate more capital to that brand. However the development landscape has only provided about three to five opportunities for next year. At Pei Wei, we expect to open 25 to 30 new restaurants over the next two years, roughly 10 to 12 next year with the balance in 2012.”

“EPS growth should be around 10% as a result of slightly better restaurant margins, improved profitability at our global brands division and a smaller share count.”

“Right now, we have 200 domestic Bistros and we continue to play with a target number of about 250. And now again, we won't be exactly correct with that. It may be a little bit more, may be a little bit less.”

“Having Christmas on Saturday at the margin is probably not helpful to us. However, I will say that the last two weeks of the year in particular the last 10 days or so, every day is busy, almost regardless of when Christmas falls. So to a degree the calendar shift is negative, but I don't think it's that big of an impact.”

“As we look forward into next year, we do think there's going to be a little bit of cost pressure.”

“From then on, I think it's going to be a little bit of a battle for us. We do intend to take a little bit of price in the first part of next year to help offset increases where we think we'll see increases in labor as well as a slight increase in our cost of goods sold basket. As we push forward into some of the non-operating lines, we are anticipating as much as $0.10 of additional pressure related to our equity incentive comp program. So that's holding it back just a little bit in terms of where I would guide you today.”

“We thought about the back half of the year this year, we felt like we would see positive traffic and positive comps at the Bistro. We're early on in the fourth quarter, we remain positive. I think as we move into the holiday season, I think that strength will continue to grow.”

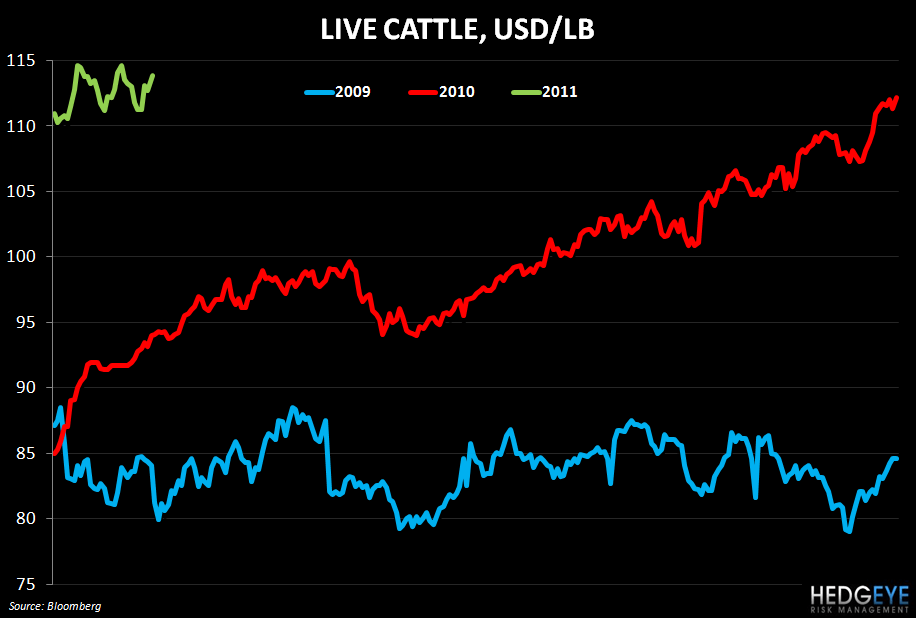

“The biggest wildcard unknown that we had last time we talked to you was on beef. We began to lock some of that into 2011 now. That's coming in a little bit higher than 2010. So obviously our overall commodity basket will probably be up slightly next year.” [see beef chart below]

“Our thoughts with respect to pricing, I'm estimating and guestimating that it's going to be similar to what we did this year, which means roughly 1% to 2% at both concepts.”

“We expect to see higher utilities that's been running a little bit higher for us, property taxes and so forth, which just brings it slightly lower than we saw in 2009.”

“We shifted the spend to October, primarily along the lines of Bert's thought that September is not necessarily the best month in the restaurant industry that we might get a greater impact by shifting the spend to October, which is traditionally a better month”

“So with that learning, we will craft our next LTO launch, which will happen sometime in the middle to the end of the first quarter next year.”

Howard Penney

Managing Director