The guest commentary below was written by David Root, CFP®, Founder and CEO at DBR & CO, a Pittsburgh-based wealth management firm. This piece does not necessarily reflect the opinion of Hedgeye. You can follow DBR & CO on Twitter here.

“I’m only in the middle of my first retirement.” - David Lee Roth, lead vocalist, Van Halen

We have a client in the Western United States that is world-renowned for groundbreaking life-prolonging orthopedics and health and wellness therapies. Their mission is to not just sustain but improve the quality of life as we age, at a time when we are all living longer.

Through a highly sophisticated series of tests, the researchers are able to analyze current and future physical attributes of patients – providing a blueprint for increased and improved longevity. They are in a unique position to meet the needs of a growing older population that stands to live longer than all previous generations.

To learn more, I went through the testing process myself. It involved the creation of a cellular footprint, mapping in real time what is happening in my body at the cellular level. The output helps determine our susceptibility to health incidents such as stroke, heart attack, or cognitive issue.

Their insight is that as we age, we accumulate dead cells in our system. The goal of this specific treatment is to rid those dead cells, and actually reverse the aging process. This is called senescence.

The most important aspect of this research is that by reversing the aging process at a cellular level, aside from potentially extending lifespan, it could very likely extend our ‘health span’ too. In simple terms, this treatment may enable you to actually become biologically younger over time. Additional medical advancements, married with this new technology, very well may push the boundaries of the aging process as we know it.

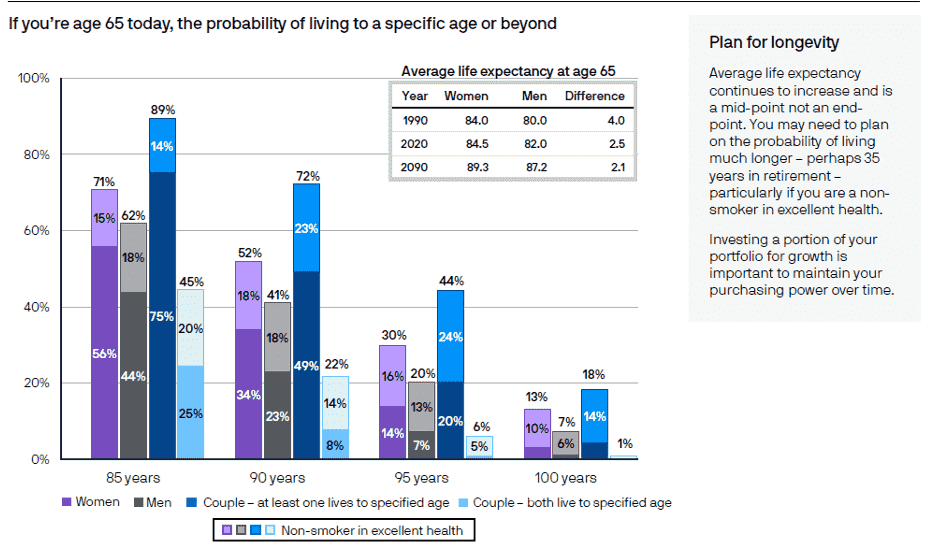

After going through this process, I had a simple question: what are the financial implications of this new frontier? Statistics show that Americans have 20 healthy years after age 60, on average.

The fastest-growing population segment in the United States is the 85-plus age group. Today, should current life expectancy trends hold, it is projected that half of the babies born in wealthy nations will live to age 100. Some research even suggests that 142 years may be the "new normal" life expectancy in the future.

Source (chart): Social Security Administration, Period Life Table, 2018 (published in the 2021 OASDI Trustees Report); American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, http://www.longevityillustrator.org

More years requires more money with which to live. This will have a major impact on money management. The truth is, like our client’s literally life-changing research, it all comes down to understanding and analyzing the data in front of you.

Extended lifetimes will require today’s investment and financial planning to evolve into something larger – longevity planning. It will require extending the amount of money retirees need over more decades, potentially multiple more decades, than many have been accustomed to projecting in the past.

Stretching retirement funds until age 100 and working until age 80 just may become more common in the not-too-distant future.

Our firm takes a similar approach for institutional clients, as we manage corporate retirement plans, corporate pension plans, endowments, and foundations, all of which have perpetual time horizons.

Such longevity not only means we all will need to work together to create a new, deeper, and more comprehensive vision of retirement for longer lifespans, but also longer work spans.

Issues like post-retirement careers, continuing education and training, and living arrangements are now part of the advisor-client dialogue, as longer lifespans give retirees more opportunities to ask, "What's next?" Armed with those insights, advisors can then outline the strategies to best support this vision, as it inevitably grows and evolves over time.

As the over 65 population continues to grow, one-person households are growing fastest—with 43% of women over 65 today living by themselves. Nearly one-third (30%) of couples over 65 now live without their children nearby. So, it could be important to consider how independent you can remain in later years. You may need to plan for expenditures beyond the obvious such as healthcare, food, and housing.

Our wellness client made my testing experience as comforting as possible by assigning me a knowledgeable relationship manager to educate me on their technology and explain their efforts to extend one’s health and well-being for a longer life.

Our firm and our advisory team must be just as determined to educate clients on our efforts to extend their wealth in order to serve them longer than what has been expected in previous eras.

This also requires our clients to adjust their thinking about retirement. Imagine how you would like to live longer in your later years. Ask yourself life-planning questions such as: What do I want out of life? What gives me joy? How do I plan to afford it? Identifying what brings you joy, security and purpose will help you plan for and make the most of your extended retirement years, which may last three decades or more.

Beyond staying healthy and having enough money to sustain your retirement, it is also important to maintain a positive outlook. The future will almost certainly include better times, and that is something worth planning for.

Now, as for my test results, they fortunately provided me with some peace of mind. But just as we need to respond to challenges to our financial plan, I still have some things to work on for my long-term health and wellness plan. And I can say, I’m excited to get started.

Thanks for reading.

David Root, CFP®

Founder and CEO

DBR & CO