CAKE reported earnings for 4Q10 after the close, announcing revenues of $416.7 million versus $400.6 million for the same period one year prior. Earnings came in at $0.36 versus the Street at $0.35. This was a low quality quarter, however, with the tax rate coming in at 23.8% due primarily to a higher manufacturing tax deduction on the significant increase in the production of bakery products. Bakery sales were a bright spot for CAKE this quarter, surprising management, coming in at $31.9 million, or up 22.3% on last year. Of course, this level is unsustainable and management said as much during its commentary, stating that Bakery sales should remain at approximately 5% of sales.

Turning to the company’s costs, cost of sales increased to 26.3% of revenue for 4Q10 compared to 25.3% of revenue for 4Q09. This increase was attributed to higher bakery sales as well as continued pressure from dairy costs, as expected. Labor costs were a major help to earnings during 4Q, ending up at 30.8% of revenue for the fourth quarter, down 120 basis points from 32% in the prior year. Of this, management stated that perhaps 30 bps was due to improved management of labor while approximately 90 bps was due to two unusual items: lower equity compensation and a benefit from the Federal Hire Act, which resulted in lower FICA costs. The 90 bps was split fairly evenly between these two factors.

G&A expenses decreased 60 bps to 5.9% of revenues due to lower bonus accruals and depreciation was 4.3% of revenues versus 4.8% a year prior. This favorability was due to sales leverage and an impairment charge in 4Q09. In addition, net interest expense was $1.5 million versus $5.4 million a year ago; a $2.2 million expense to unwind an interest rate collar a year prior, as well as a higher debt balance, resulted in this year-over-year decline.

Clearly this quarter, by happenstance, several factors fell into place for CAKE. Operating margins improved by 90 bps year-over-year to 7.4%.

Outlook was obviously the primary interest, given that comps had been preannounced in January. For 1Q11, diluted EPS guidance was given as $0.29 to $0.33. Full-year 2011 guidance was reiterated at $1.55 to $1.70, based on a comparable store sales projection of 1-to-3%. Clearly the implication here is that management is hoping for a pickup in earnings power after the first quarter. The first quarter, management said, is being impacted by record snowstorms in the Midwest and Northeast as well as elevated food costs. Dairy sales have continued to skyrocket since January 1st and, quarter-to-date, management estimates that weather has cost CAKE 1% from a comp perspective.

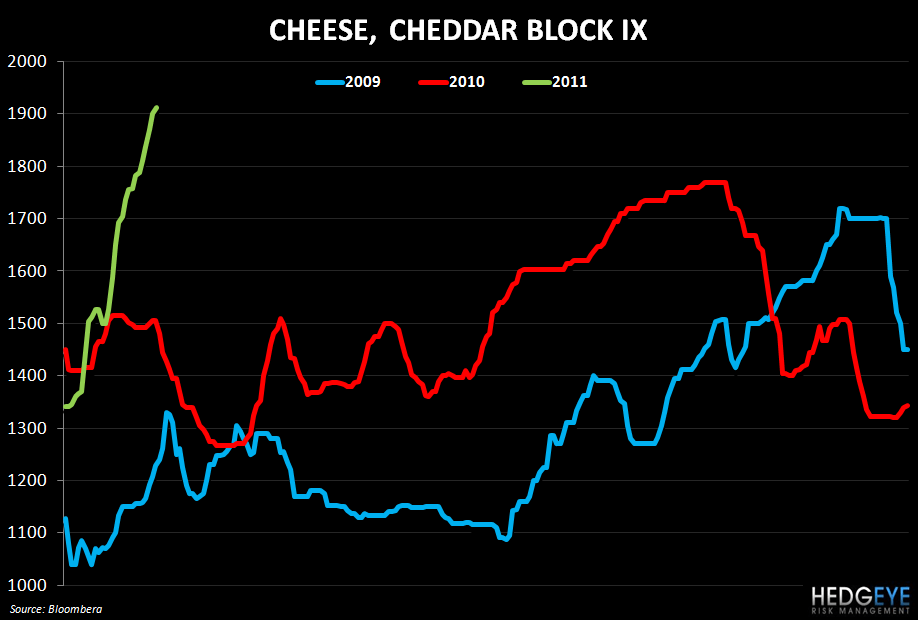

Management is forecasting food inflation of 4% in the front half of the year followed by 3% in the second half. Since management first gave FY11 guidance in October, their outlook for food costs alone has risen by “at least” $0.05. Nevertheless, management unconvincingly stated that by “actively managing our cost structure, including ongoing improvements in labor productivity and tight G&A controls”, the company will absorb these costs. In my experience, a nearby penny is worth a distant dollar – I certainly was less than convinced by management’s assurance.

Firstly, their comparable-restaurant sales guidance may prove difficult. While mix is trending less negative than it did for the first three quarters of 2009, the compares facing top line trends step up meaningfully from 1Q onward.

The company is implementing a 0.7% menu price increase in their winter 2011 menu change, lapping a 0.6% menu price increase from the winter of 2010. This will leave 1.4% pricing on the menu by the end of the year. With only 60% of its food basket on contract, it seems that the company may have to ponder taking additional pricing. Management knows from experience that The Cheesecake Factory’s customer is fairly price sensitive, hence the average check problems that have hurt the top line for the last number of quarters.

Secondly, the cost outlook is less-than-positive. As of now, dairy, cheese, and fresh fish are not contracted. Rather than proactively passing costs along to the consumer, unsurprisingly, management stated that it would prefer to be a follower than a leader in this regard. Depending on how spot markets behave throughout the year, some competitors may be better insulated from food inflation than CAKE; the company may have difficulty waiting for other chains to blink first.

It is instructive to bear in mind that, for CAKE, as management stated at the Cowen Conference, “every 1% increase in annual comparable sales is about an incremental $0.08 in earnings per share, based on 40% flow through, although many times we have been able to achieve a flow through better than 40%.”

The labor cost initiatives intended to make up the $0.05 of food costs (from what management knows of the quarter so far) may also prove a stretch. Management stated that the magnitude of labor savings in 2011 will depend on what comps are; “At the higher end of our range, we should be able to sustain some improvement in the labor line. At the lower end, it’s going to be a little more challenging.” Given the difficult comps ahead from a top-line perspective, exposure to food inflation and management’s revealing hesitancy to proactively raise prices, I believe that the outlook for 2011 is decidedly negative for CAKE.

Howard Penney

Managing Director