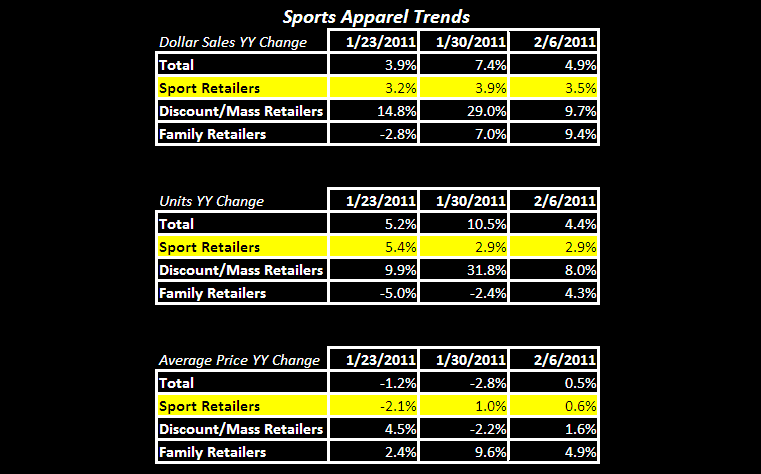

The weekly athletic apparel data reflects positive sales for the week adding to a more stable trend of positive sales observed for each of the last four weeks. The family retail channel continues to strengthen posting the only sequential improvement on the week. It’s also worth noting that prices firmed up, with ASP’s increasing across each of the channels. This marks a change in trend for the first time since the week before Christmas and coincides with recent anecdotes coming out of January that inventories may indeed be in healthy shape.

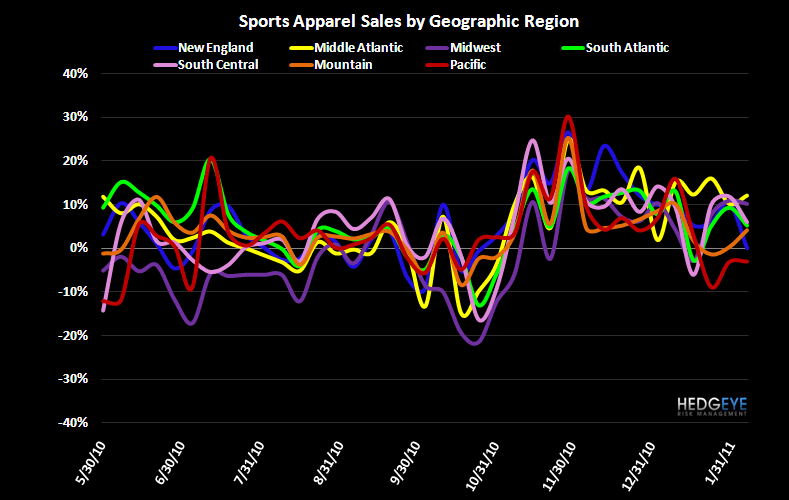

In looking at the brands, we highlight the disparity in outerwear between the growth in The North Face at up +10%, while Columbia continues to decline down -1% posting the only such loss on the week. Lastly, the Pacific region continues to underperform all other regions for the third week in a row – a trend worth noting in our book and unfavorable for retailers over-indexed to the west coast such as BGFV. It just so happens the company cited negative comps in December as the reason for negatively preannouncing last month. A trend that may have continued so far in 2011.

Casey Flavin

Director