From the Global Oil and Gas Patch: February 10, 2011

Current Long Positions in Hedgeye Virtual Portfolio……

- Oil (via the etf OIL) – Initiated 2/2/11 @ $25.21

- CNOOC (CEO) – Initiated 2/9/11 @ $210.25

Current Short Positions in Hedgeye Virtual Portfolio……

- Murphy Oil (MUR) – Initiated 2/3/11 @ $42.65

Chart of the Day……

Key Metrics……

Must Know News……

PetroChina and Encana Team Up in Western Canada……PetroChina Co. (PTR), China’s biggest energy producer, agreed to buy a 50% stake in Encana Corp.’s(ECA) Cutbank Ridge gas assets in Canada for C$5.4 billion ($5.4 B-billion) in its largest overseas acquisition. PetroChina would get daily production of 255 MMcf of natural gas from 635,000 acres in the provinces of Alberta and British Columbia, Encana said yesterday. Proven reserves are 1 Tcfe. The companies will also form an equal venture to increase output, the Beijing-based producer said in a statement today. Each company would contribute 50/50 to future development capital requirements. Encana will initially operate the joint venture's assets and market the production. (Bloomberg, Street Account)

Hedgeye Energy’s Take: ECA has been marketing for a partner since early 2010 to secure development of these assets. The Chinese have deep pockets and need reserves; ECA wanted to spread the development/capital risk and has found a willing partner in PTR willing to pay top dollar. The price appears high for natural gas assets in Canada at roughly ~C$8,500/acre, or ~C$5.40/Mcf of proven reserves, and marks PTR’s entry into North American gas assets. Asian partners, primarily the Chinese, have invested ~C$15 B in Canadian resources. Indeed, since the beginning of 2010, Chinese Companies have spent nearly ~$46 B in global resource acquisitions.

Chevron Buys Shale Gas Assets……Oil giant Chevron Corp. (CVX) said Wednesday it has recently acquired about 200,000 acres of land in the Duvernay shale gas formation in Alberta, Canada. "This has established an important core land position for Chevron Canada in shale gas," said Kurt Glaubitz, a company spokesman. Chevron is planning to commence appraisal drilling during the second half of this year, he added. The Duvernay shale sits nearly four kilometres below the surface. In its broad reach across central Alberta, it underlies fully 10 other rock zones that contain commercial quantities of natural gas. Also, compared to more proven areas, Duvernay land remains abundant enough that major companies can make a large bet on it. It lies in an area thick with pipelines and other infrastructure, making it potentially cheaper to develop than plays in the northern hinterland. (Company statements, The Globe and Mail)

Hedgeye Energy’s Take: We expect CVX to step up its activity in North American shale development as CVX pursues production growth at a lower political risk profile. While the production is not immediate for 2011, CVX is seeking to become gassier with a greater footprint in North America, and it has the deep pockets to invest through the price cycles. CVX is thinking long-term.

Chinese Oil Demand Growth to Slow…… China’s oil demand growth may slow “noticeably” this year as the economy expands at a reduced pace and the country improves energy efficiency, according to the International Energy Agency. China, which consumes more oil than any country except the U.S., may boost efficiency as it burns more natural gas and restricts car use, according to the energy security adviser to the Organization for Economic Cooperation and Development. Fuel demand may increase 6% this year, from 12% in 2010, the IEA said today in its monthly Oil Market Report. “The economy should cool down slightly, gasoil shortages ease and oil intensity fall,” the Paris-based agency said. “New sources of energy should provide some degree of inter-fuel substitution.” “China’s oil demand outlook has become increasingly crucial for global oil balances,” the IEA said. “We remain cautious so far, expecting China’s oil demand to rise by a much more modest but nonetheless significant 570,000 barrels a day.” (Bloomberg)

Hedgeye Energy’s Take: Indications are that China will slow its economy in 2011, as recent interest rates hikes are pointed at curbing rising inflation. A slowing economy will ease oil consumption demand, which depending on how fast inflation accelerates and the global economic situation deteriorates will put downward pressure on crude prices, particularly Brent marker crudes, which Chinese refineries rely upon.

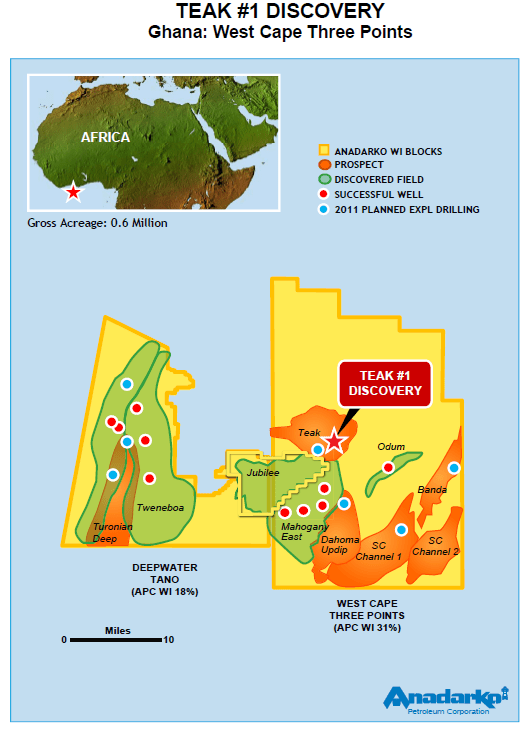

Anadarko Announces Discovery Offshore Ghana……APC announced a discovery at the Teak-1 exploration well in the West Cape Three Points Block offshore Ghana, where Anadarko owns a 30.875% working interest. The Teak-1 well encountered a total of approximately 240 net feet of oil, condensate and natural gas pay in five separate Campanian and Turonian-age reservoirs. More specifically, the well encountered approximately 70 net feet of oil pay and almost 108 net feet of natural gas pay in the Campanian, and about 46 net feet of gas condensate pay and 16 net feet of oil pay in the Turonian reservoirs of a similar age to the Jubilee field. Oil samples recovered from the Teak-1 well indicate oil of approximately 40 degrees API gravity in the Campanian reservoirs and 32 degrees in the Turonian reservoirs. The Teak-1 discovery well, which is located more than two miles northeast of the Mahogany-2 well, was drilled to a total depth of approximately 10,400 feet in water depths of approximately 2,850 feet. The partnership plans to suspend the well for future use and mobilize the rig to drill the Teak-2 prospect. West Cape Three Points Block, is operated by Kosmos Energy (30.875%), Tullow Oil plc (TLW LN)(22.896%), the E.O. Group (private) (3.5%), Sabre Oil & Gas Holdings Ltd (private) (1.854%) and the Ghana National Petroleum Corporation (10%). (Street Account)

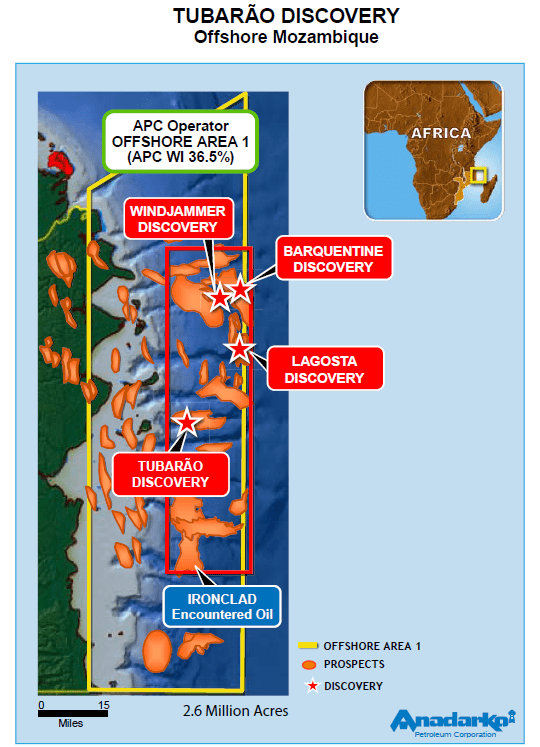

Hedgeye Energy’s Take: APC has had considerable exploratory success offshore West Africa in Ghana and offshore East Africa in Mozambique. In Mozambique, APC made a fourth gas discovery offshore Mozambique in the Rovuma Basin, the discovery well was at the Tubarao prospect. Appraisal drilling is expected within the year for offshore Ghana, but initial indications are the hydrocarbon potential i as Ghana has become a core area of development for APC and its partner TLW. First oil at the massive Jubilee Field in Ghana, with reported ~1 B bbl of resource potential was achieved in December 2010, with gross production targeted at 120,000 b/d by mid-2011. See our charts of the day above for maps of APC's recent discoveries.

Lou Gagliardi

Kevin Kaiser