MCD reported global sales of 5.3% which surpassed consensus expectations of 4.4%. By region, it seems that the U.S. slowdown I have been anticipating for 2011 may be kicking off. MCD beat the consensus in every region of the world but the USA. As you know, I believe that MCD has issues in the USA that have not been fully addressed by management.

Despite an easy -0.7% compare, MCD printed a 3.1%, which implies two-year average trends sequentially decelerated by 60 basis points. On a calendar-adjusted basis, two-year average trends accelerated slightly (by 17.5 bps) from December’s disappointing result. January’s result for the U.S. was significantly lower than the Street’s expectation of +4.4% for the U.S.

The decline in MCD's two-year average trends to 1.2% clearly puts a same-store sales decline of 2-3% in play for March 2011.

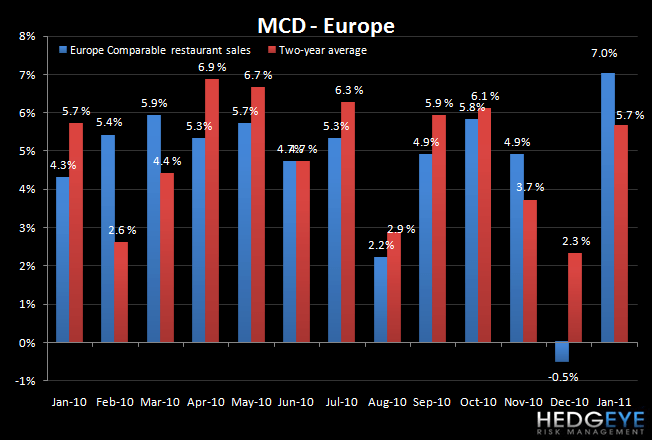

Europe saved the day for MCD, printing a +7.0% comp, which implies a 335 basis point sequential acceleration in two-year average trends from December. On a calendar-adjusted basis, two-year average trends accelerated 412.5 basis points.

APMEA results came in above my expectations and those of the Street. Two-year average trends decelerated sequentially on a two-year average basis by 20 basis points. On a calendar-adjusted basis, APMEA two-year average trends accelerated by 57.5 basis points.

Howard Penney

Managing Director