Nowhere was that more evident than with LVS which puts a lot of perspective into Sheldon's comments last night.

Total revenues grew 32% YoY in January, a little short of the 40% pace where the month was heading in the first part of January. We estimate that direct play was 8% this January vs. 7% last year. Adjusting for direct play, hold for both periods was high, just north of 3%, so there was no impact on market growth.

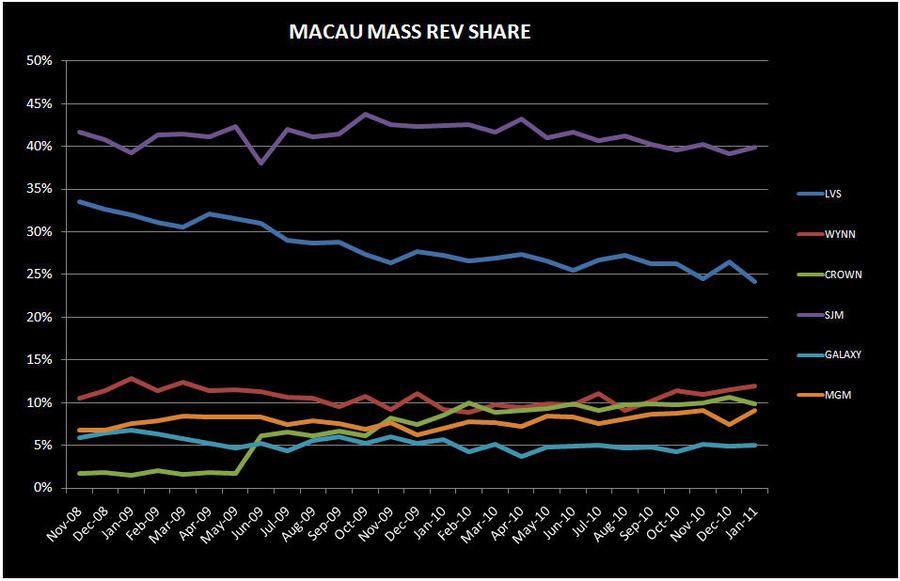

Sheldon was very bullish about January on the LVS call but after looking at the detail, the enthusiasm may be fleeting. It’s all hold percentage yet market share wasn’t even that great. As we noted earlier this week, LVS’s market share was almost 18%, above Q4 but still well below the 2010 average of 19-20%. LVS’s hold percentage was through the ceiling, especially at Four Seasons. However, Rolling Chip (VIP volume) market share was very low- at 1.1% in line with the last two months. Mass market share declined to 24.2%, the LVS' lowest share since we've been tracking the numbers (early 07'). Rolling Chip share was 11%, in-line with December but also the lowest since pre-Venetian. The underlying January metrics just were not good for LVS despite Sheldon’s assertions.

Wynn’s lower share looks like it was a combination of weaker hold relative to the last 2 months and lost VIP volume share. Mass market share actually increased sequentially to 11.9%, its highest since March 2009. That should bode well for profitability. MPEL’s Mass share was a strong 9.9%, below Nov/Dec but well above the average of rest of the year. MGM continues to perform very well, posting its 3rd highest Rolling Chip share since August 2009 ever and its 2nd highest Mass share ever, in January.

Of course all eyes are now focused on Chinese New Year…

Y-o-Y Table Revenue Observations:

LVS table revenues grew only 8% in January compared to market growth of 33%

- Sands was up 11.6%, driven by a 25% increase in VIP which was offset by a 10% decrease in Mass

- Although hold, adjusted for 15% direct play (in-line with 4Q10), was about 3.3%, last’s year’s comparison using a 10% direct play estimate was even higher at 3.4%

- Junket RC increased

- Venetian was the only property to see revenues decline 7.5%, with VIP down 20% somewhat offset by Mass up 14%

- Junket VIP RC decreased 4.2% but hold was weak and up against a tough comp. Assuming 19% direct play, in-line with 4Q10, we estimate that hold was 2.63% compared to 3.50% hold in Jan 2010

- Four Seasons was up 65% y-o-y driven by 79% VIP growth and 13% Mass growth

- Junket VIP RC decreased 36%, but the massive hold which we estimate was north of 5% (assuming 4Q10 54% direct play levels) more than made up the difference, especially compared to the low 2.2% hold in Jan 2010 (assuming 43% direct play)

Wynn table revenues were up 43%

- Mass was up 54% and VIP increased 40%

- Junket RC increased 20% and an easy hold comp helped comparisons

- Assuming 12% of total VIP play was direct, we estimate that hold was 3% compared to 2.7% last year (assuming 10% direct play)

Crown table revenues grew 21%, with Mass growing 38% and VIP growing 18%

- Altira was up 36.6%, with Mass up 27% and VIP up 37%

- VIP RC was up 13% and hold comparisons were favorable. We estimate that hold was 3.3% compared to 2.8% last year.

- CoD table revenue was up 10%, entirely driven by Mass growth

- Mass revenues grew 41% while VIP only grew 3%

- VIP growth was negatively impacted by a difficult hold comparison. Junket VIP RC grew 44%, Jan 2010 hold was 3.8% vs. 2.8% this month, assuming 15% direct play

Despite the family drama, SJM revs grew 38%

- Mass was up 11.6% and VIP was up 54%

Galaxy table revenue was up 50%, driven almost entirely by 57.6% VIP growth while Mass grew only 5.4%

- Starworld continued to perform well with table revenue up 64%, driven by 71.5% growth in VIP revenues and 4% growth in Mass win

MGM table revenue was up the most in January, growing 58%

- Mass revenue growth was very strong at 54%, while VIP grew 59%

- Junket rolling chip was up 73%

Market Share:

LVS share ticked up to 17.8% from 16.7% in December, but was still below its 2010 average of 19.5%

- Sands' share was flat sequentially at 6%

- Venetian’s share decreased to 8%. All-time low market shares for the property were set this month in Mass, VIP, and Junket RC volume

- Mass share declined 160bps to 14.7% from 16.3% in December

- VIP share declined 1.1% to 5.8%

- Junket RC declined to 5.4%

- FS share increased to 3.4% on the back of massive hold

- Junket RC share of 1.1% remained at the bottom- in-line with the last 2 months

- VIP share increased to 3.8% from a low of 1.0% in December

- Mass share was flat sequentially at 2%

WYNN's share at dropped 3% to 13.9% from 16.9% in December

- Mass market share ticked up 40bps to 11.9%- its best share month since April 09

- VIP market share decreased to 14.6% or 3.9% sequentially, compared to its 2010 average of 16%

Crown's market share increased to 14.5% from 14.2% in December

- Altira’s share increased to 6.7%- 1.8% sequentially - the properties’ best share month since September 2009. The share gain was entirely from gains on the VIP side.

- CoD’s share decreased 1.5% sequentially to 7.8%

- Mass market share declined to 8.1% from a high of 8.8% in December

- VIP market share declined 1.8% to 7.8% while Junket RC share only decreased 20bps sequentially to 7.8%

SJM's share increased 1.5% to 32.2% from December levels, with share gains coming mostly from Mass

Galaxy's share also increased 1.5% sequentially to 11.8%

- Starworld's market share grew to 10.1% from 9.1% in the previous month

MGM's share decreased to 10.3%, from 11.6% in December

- Mass share increased 170bps to 9.1%- which was the property’s second highest share

- VIP share declined 2.2% sequentially to 10.7% but VIP chip share only decreased 50bps

Slot Revenue:

Slot revenue grew 26.7% YoY in January to $102MM, the second best month on record after October 2010 when slot revenues hit $111MM.

- MGM slot revenues grew the most at 123% reaching $17MM – a record for the property

- At 39% YoY growth, WYNN had the second highest growth with slot revenue reaching $22MM in-line with October levels and a high for the property

- Crown’s slot revenues grew 26.6% reaching $19MM

- SJM grew 17.9% to $14MM

- LVS slot revenues were flat YoY at $28MM

- Galaxy was the only operator with negative YoY, declining 7.7% to just $2MM