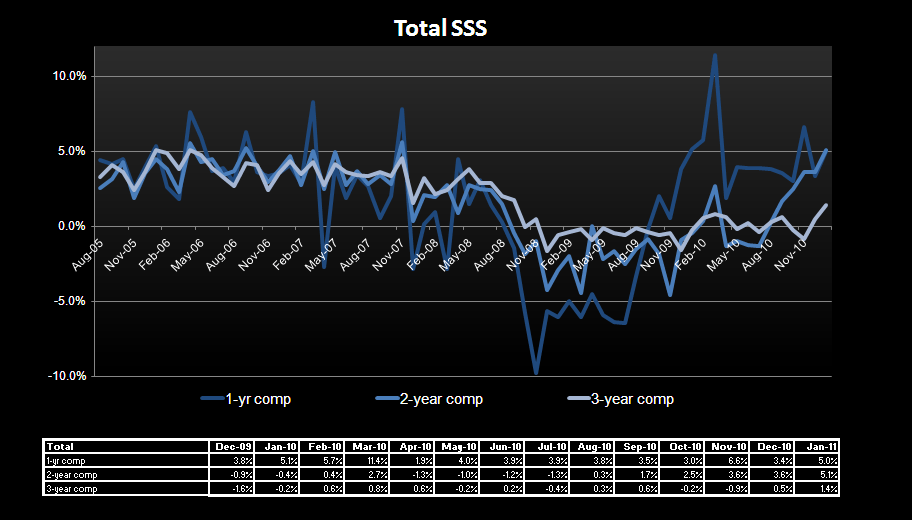

January sales results provided a surprisingly solid end to the retail fiscal year, with about two-thirds of today’s sales reports surpassing (tempered) expectations. With January sales volumes amongst the lowest of the year, the relevance of such results can be debated. However, the reality of the sequential uptick has two important takeaways. First, most retailers end the year with clean inventories and less clearance on a year over year basis. This sets up well for the Spring transition. This is also the reason why we saw some companies raise their EPS guidance, even in some cases with lower than planned sales results (JCP, KSS). Second, the weather was barely mentioned as an excuse. Only a handful of retailers including Costco, BJ’s, JCP, and HOTT cited the impact of stormy weather on the month and actually quantified it. Despite this, COST and BJ still exceeded expectations. Others with winter apparel and footwear exposure likely benefited, leaving little reason to mention record snowfalls and deep freezes as an excuse.

We do not expect this strength to continue, especially as first quarter compares are challenging and prices at retail are beginning to creep higher. With that said, the facts are the facts and the two-year same store sales run-rate for the broad index reached its highest level since 2007. Time to focus on 2011 with full attention and unfortunately less clarity than we’ve seen surrounding the retail environment in well over a year.

Callouts from today’s reports:

- While e-commerce sales remained robust for most, sales were actually down 6% at hottopic.com and only up 2.6% for jcpenney.com. Sites with strong growth included Kohl’s (+60%) and Macy’s (+27.2%).

- ROST continues to take advantage of the environment to secure closeouts at favorable (current) prices ahead of cost increases. The company ended January with pack-away up 900 bps y/y to 47%. Inventories did increase slightly since December as well going from up 19% in total to up 25%.

- Consumer electronics remained weak for the month as measured by performance at COST and TGT. COST noted that TV unit sales were flat while overall dollars were down in the mid single digit range. Target noted that overall hardlines declined by mid single digits, driven by weakness in electronics, music, movies, and books.

- Comparisons are still overrated- for Nordstrom. The company reported its 17th consecutive month of traffic increases.

- Men’s apparel was cited as a leading category for the month by: JWN, KSS, and TGT.

- COST noted that while inflation is tracking about 1% for food and sundries, the levels of increases have subsided a bit relative to recent months. Meat and deli showed the highest levels of inflation, up mid single digits.

- KSS noted that clearance levels were down 9% year over year. Clearly a help to margins and a potential headwind for sales.

- Aeropostale noted that average unit retail decreased in the low double-digits, primarily due to increased promotional activity vs. last year.

- American Eagle noted that less promotional activity and a higher mix of accessory sales resulted in a flat average unit retail price for the month.

- Big Lots noted that the later timing of income tax refunds and the reduced availability of income tax refund anticipation loans, impacted a portion of their customer base and certain discretionary categories, particularly furniture.

- Next month’s sales day will be even less hectic, with all three teen retailers (ARO, AEO, & ANF) ceasing to report monthly sales. Let the speculating begin!

Eric Levine

Director