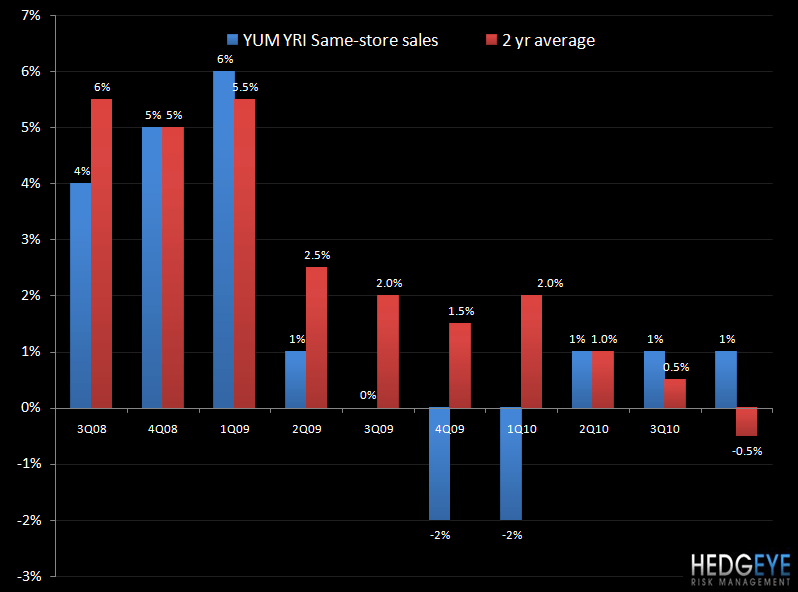

YUM finished 2010 strong with 4Q10 results that came in better than expectations on both the top and bottom line. Earnings of $0.63 per share easily beat the street’s $0.60 per share estimate and the reported 8% comp growth in China and 5% comp growth in the U.S. came in much better than the street’s 6.0% and 2.8% estimates in China and the U.S., respectively. YUM’s YRI segment was the only division to fall short of same-store sales expectations with the company reporting 1% comp growth versus the nearly 3% consensus estimate. That being said, the company’s restaurant margins during the quarter were stronger than street estimates across the board.

YUM’s CEO David Novak opened his remarks on the earnings call by saying, “I'm especially pleased to announce that 2010 was one of our best years as a company. We reported 17% full-year EPS growth excluding special items, marking the ninth straight year that we exceeded our annual target of at least 10%. In fact, 17% EPS growth is our best ever and what makes us even more impressive is that it was driven by a 15% increase in operating profit including gains across all three of our business divisions.” These comments, alone, set the stage for a more difficult 2011 on a relative basis as the company will be lapping these strong results.

Although the company maintained its confidence in its ability to grow EPS by at least 10% in 2011, management did highlight expected headwinds, which will hurt operating profit growth and margins in 2011:

- Commodity inflation – guided to +5% in China, +4% in the U.S. and +3% for YRI. Management is hedged for about 6-9 months, but still has about $40 million of commodity exposure in China and the U.S. if prices don’t improve from current levels.

Hedgeye thought: These incremental costs will definitely have a negative impact on margins in 2011, but this is not a problem that is unique to YUM.

- Continued labor inflation in China – guided to a mid-teen increase in wages. Labor increases are not a new phenomenon in China but there were two wage rate increases in 2010, which had a sizeable impact on the labor expense line in 4Q10 and should continue to impact it, particularly in the first half of 2011.

Hedgeye thought: Again, this higher wage inflation is not unique to YUM. That being said, YUM investors have become accustomed to restaurant-level margin growth after seven quarters of growth prior to the slight decline reported in 4Q10. The company already implemented a price increase in China in early 1Q11, which management said should cover about three-quarters of the expected inflation impact, but margins are expected to decline YOY. Specifically, in 1Q11, the company is lapping 1Q10’s 26% margin, which management said is not a sustainable level.

- China: Lapping 2010’s one-time $16 million benefit from participating in the World Expo in Shanghai and facing $25 million in incremental tax expenses in 2011 from a new business tax – Combined, these two items are expected to have a 5% negative impact on China’s 2011 profits.

Hedgeye thought: These one-time items only exasperate the already difficult operating profit and margin comparisons the company faces in 2011. Although management has tried to set reasonable margin expectations, investors may not react positively to reported margin declines in what is now YUM’s most important segment from a profit contribution standpoint.

These headwinds will take a toll on YOY growth in 2011, but again, most of these issues are beyond management’s control. Going beyond the expected $20 million foreign currency benefit in both China and YRI, margins should be supported in FY11 and beyond by the company’s current refranchising strategy in the U.S. and YRI and growth in emerging markets.

U.S.: I typically have a hard time finding anything positive to say about YUM’s U.S. business, but the company’s significant progress on refranchising company units in the fourth quarter, combined with the recent announcement that YUM intends to sell its entire Long John Silver’s and A&W restaurant business, is a definite step in the right direction. The company does not expect the eventual sale of this business to have a material impact on its ongoing earnings, but it signals that management wants to better align its focus in the U.S. on what matters to profitability and that is Taco Bell.

To that end, the company sold 306 company-owned units to franchisees during the fourth quarter and 404 for the full year. The bulk of those units (330) were Pizza Hut and KFC restaurants, which again lessens YUM’s profit exposure to those concepts in the U.S. The company plans to refranchise another 500 units in 2011, with KFC expected to drive the majority of those sales. With KFC same-store sales down about 4% in 2010, following on the heels of the prior three years of declines, this decreased company ownership will be welcomed by investors. Given the current state of business, these KFC sales may not yield the highest of proceeds for YUM, but at least it will allow the company to shed some of the restaurants which have been a drag on margins.

Management attributed the 60 bps of U.S. restaurant-level margin improvement in 4Q10 and 30 bps for the full year to refranchising. With most of the refranchising occurring during the fourth quarter, in addition to the continued refranchising initiatives planned for 2011, YUM should see an even greater benefit to margins going forward.

YRI: Restaurant margins increased 80 bps in 2010 and 190 bps in 4Q10, driven primarily by YUM’s equity business in Thailand and the refranchising of the company’s Taiwan business in the first quarter. 2011 margins will be helped even further by the fact that the company completed the refranchising of its Mexico business during 4Q10. Specifically, management stated that the Mexico refranchising should have a positive impact on 2011 operating profit of about $10 million. YUM will focus on the U.K. market in 2011 to further execute its refranchising efforts.

Sales were sluggish overall for YRI during 2010. System sales grew 9% in the company’s emerging markets, however, far outpacing the 4% growth in its developed markets in 4Q10. YUM opened 548 of its total 884 new YRI units in 2010 in emerging markets so sales growth should improve as the company further accelerates its development in these higher growth markets.

In conclusion, on top of the expected outlined headwinds and the fact that the company is facing difficult comparisons in 2011, I am somewhat concerned about the company’s current same-store sales guidance, which seems quite aggressive across the board given reported trends during the fourth quarter. Despite the same-store sales growth upside reported in China and U.S. during the fourth quarter, two-year average trends actually decelerated slightly from the third quarter for China, YRI and Taco Bell in the U.S. The 2011 comp guidance for China (up at least 4%), YRI (up at least 2-3%) and U.S.’s Taco Bell (+3%) all assume a significant acceleration in two-year average trends from 4Q10 reported levels.

Howard Penney

Managing Director