The guest commentary below was written by Joseph Y. Calhoun, III of Alhambra Investments on 5/8/21. This piece does not necessarily reflect the opinions of Hedgeye.

Something very important happened last week. No, it had nothing to do with the stock market, at least not directly. There was a lot of volatility in stocks last week but in the end, the S&P 500 was down a mere 21 basis points (0.21%).

Yes, growth stocks continued their march toward reality with the NASDAQ 100 down 1.25% but even that isn’t much of a move in the big scheme of things. No, the really big news happened in a part of the market that doesn’t get a lot of attention but is actually quite important.

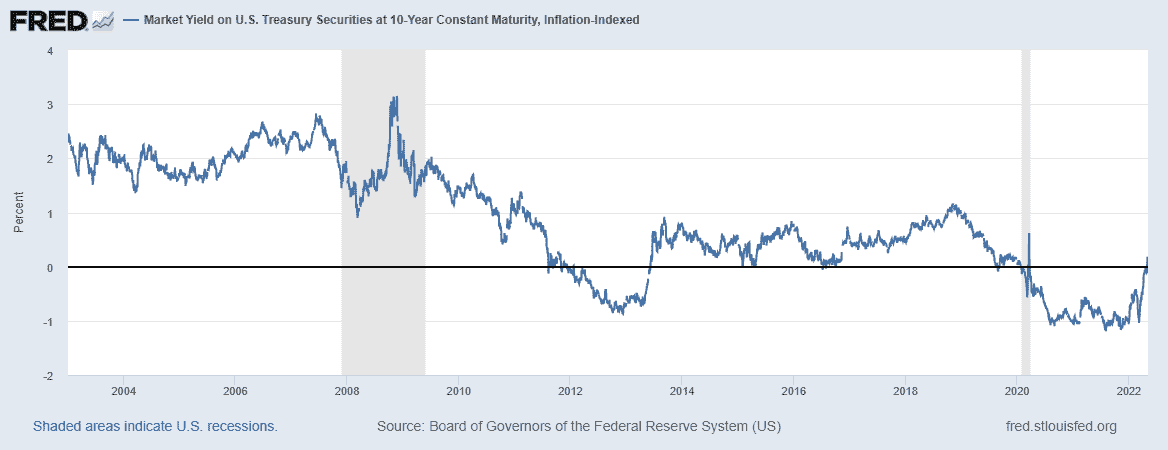

Real interest rates, as measured by 10-year TIPS yields, turned positive last week. Except for a brief spike during the onset of COVID, 10-year TIPS yields have been negative since late January of 2020.

With markets supposedly on edge about inflation, it seems like pretty important news that investors have been aggressively selling inflation protection for the last month.

Real interest rates are the intersection of savings and investment and in general, higher real rates are associated with higher rates of investment in the economy. A lot of economists – especially at the Fed – seem to think that low real rates will induce more investment – cheaper to borrow – but the evidence doesn’t support that view.

Low and negative real rates were a feature of the 1970s while high and positive real rates were the default in the 1980s which really settles that debate in my opinion. Low real rates are generally associated with inflationary eras so investors are preoccupied with preserving their purchasing power and neglect investments in the real economy.

I don’t think it is coincidence that real rates have been low since the GFC (and falling since the 1980s although not in a straight line) and we find ourselves stuck in a low growth environment.

Why real rates have been falling – and near zero or negative for large stretches of the last decade plus – is debatable, a discussion that could include demographics, monetary systems, tax policy, trade policy, immigration policy, and any number of other variables.

But we don’t need to know the reason to know that negative real rates are an obvious negative signal about the real economy. Or that positive real rates are an improvement.

In the long term, if investment in the real economy follows real rates higher, the result should be higher productivity, higher rates of growth, and lower rates of inflation.

Of course, that won’t happen immediately as investments take time to produce results, but positive real rates is certainly a step in the right direction. Inflation expectations, as measured through the TIPS market, haven’t really come down much yet as nominal rates have been rising right along with real rates but if history is a guide that should come soon.

Of course, real rates are still quite low – just 26 basis points on the 10-year – and this is very tentative as yet. There is a long way to go before we can say that this inflation episode – or supply shock or whatever you want to call it – is over. But getting to positive territory is good news and we shouldn’t ignore it.

There are potentially two important implications for investors. First, if real rates stay positive and continue to rise, I would expect value stocks to continue to outperform. The speculative areas of the market have come down a lot but don’t think that means they can’t come down more.

Those of us who invested through the dot com bust can certainly attest to that – and to the benefit of owning value stocks in such times. Second, if investors’ inflation fears are abating – and I think that is the obvious deduction if they are selling TIPS – then a peak in nominal rates is probably near.

And if inflation expectations fall as rapidly as they rose, the fat pitch referenced in the title of this post will come in the bond market. The upside from current levels is, in my opinion, considerable.

A pullback in the nominal 10-year rate to 2.5% – a rate we saw as recently as the end of March – could produce returns on longer duration bonds from 5 to 10% in a very short period of time.

For moderate investors with a large allocation to bonds, that could represent a big recovery in the value of their portfolios. And rates could easily fall more than that, down to the low 2s, and still be in a solid long-term uptrend. Returns in that case could easily approach 20% for long-term bonds.

It probably isn’t coincidence, by the way, that the last time we saw a similar surge in real rates was during the so-called Taper Tantrum back in 2013. The public perception of QE, regardless of the reality, is that it is inflationary and the obvious way to protect yourself is by buying TIPS.

With the end of QE, investors’ fears of inflation ebb and so does their appetite for TIPS. The irony is that the Fed got what it wanted from QE – lower real rates – but the result wasn’t higher growth because the fear of inflation pushed investment into non-productive areas.

Gold also rises during QE and when real rates are falling and negative. It isn’t coincidence that gold peaked in November of 2013 when real rates started to rise and it isn’t coincidence that the yellow metal has struggled recently.

All of this is very early and could easily be reversed. And merely, barely positive real rates do not mean we are headed for a boom. Take a look at that chart above. It is a visual representation of a decade of weak growth.

Real rates never even approached the levels of the period prior to the GFC. Real growth didn’t either and that wasn’t even a particularly good period for growth.

To get out of the malaise of the last 14 years we need to see real rates get back to the 2 to 3% rates we saw in the 80s and 90s.

What combination of economic policies would produce that outcome? I don’t know for sure but it seems rather obvious that monetary policy alone – and especially QE – won’t get the job done.

|

Click HERE if you want to continue reading the full note. |

EDITOR'S NOTE

Joe Calhoun is the President of Alhambra Investments, an SEC-registered Investment Advisory firm doing business since 2006. Joe developed Alhambra's unique all-weather, multiple asset class portfolios. This piece does not necessarily reflect the opinions of Hedgeye.