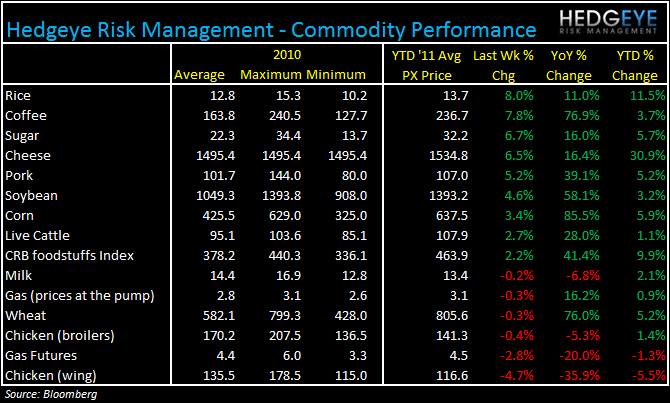

The increase of commodities continues to be fairly broad-based with most of the items we follow gaining significantly week-over-week. With the exception of Chicken Wings, all of the foodstuffs in the table below show either flat or significantly positive week-over-week price changes.

Egypt is obviously front-and-center of the geopolitical picture at the moment and commodity investors obviously keep a keen eye on geopolitical proceedings. There is speculation about food shortages due to a lack of access or movement of ships. At Egyptian ports, an absence of customs officials is exacerbating the disruption.

Rice gained 8% after trading flat last week, and relative to the other commodities at the top end of the table, its year-over-year price change is quite benign. PFCB locks in rice and, as of most recent guidance on the item, management stated that the commodity was locked in slightly favorably for 2010 and the contract continues through September of 2011.

Wheat narrowly missed out on the top spot this week, gaining 7.8% over a week ago. There is speculation that Egypt unrest may delay shipments and that is why prices have come down. However, it is unlikely that the recent pullback will persist if one shares Hedgeye’s bearish view of the dollar and if speculation that the cold snap in the central U.S. plains may adversely affect dormant crops is to be believed. PNRA expects wheat costs for 2011 to be roughly flat versus 2010, as the company currently has nearly 75% of its wheat costs locked in for 2011, modestly below the 2010 price. Looking at the chart below, it is clear that the company is hoping that the easier comps, from a wheat cost perspective, offer them some relief. If prices go higher, wheat could cause some margin pressure for PNRA in 2H11.

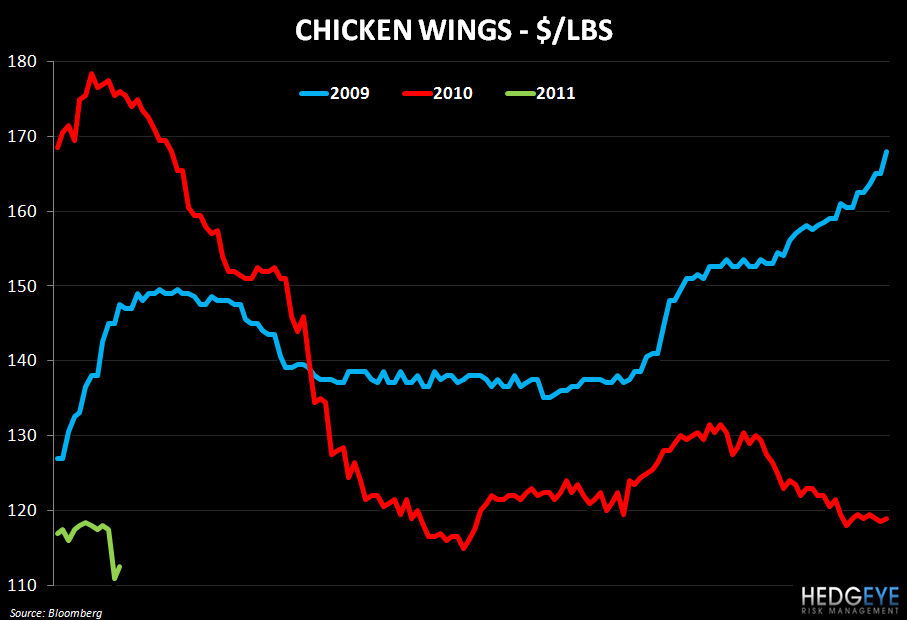

Chicken Wings continue to offer BWLD a nice boost here in 2011. Following a decline of almost 5% on the week, prices are lagging those of a year ago by 36%. The chart below shows clearly that this favorability is likely to continue for BWLD through the first half of the year if prices remain roughly stable.

Howard Penney

Managing Director