TODAY’S S&P 500 SET-UP – February 1, 2011

Equity futures are trading above fair value in a continuation of Monday's gains with geopolitical concerns more than offset by a mix of corporate earnings, ongoing M&A and positive economic data. Overnight, China's PMI data fell to a 5-month low suggesting the government's fiscal tightening policy is starting to filter into the manufacturing component. As we look at today’s set up for the S&P 500, the range is 21 points or -0.79% downside to 1276 and +0.85% upside to 1297.

MACRO DATA POINTS:

- The ISM factory index probably grew for an 18th consecutive month, to 58 in Jan., and construction spending probably rose 0.1% in Dec., economists said. Due 10 a.m. ISM prices paid, Jan. 73.5, prior 72.5

- 10 a.m. Construction spending, Dec., est. 0.1%, prior 0.4%

- 11 a.m.: U.S. buys $1b-$2b TIPS

- 11:30 a.m.: U.S. sells 4-wk bills

- 4:30 p.m.: API inventories, Jan. 28

- 5 p.m.: Domestic vehicle sales, Jan., est. 9.55m, prior 9.46m; total vehicle sales, Jan., est. 12.60m, prior 12.53m

- 5 p.m.: ABC consumer confidence, Jan. 30, prior -44

TODAY’S WHAT TO WATCH:

- Anadarko (APC)4Q adj. EPS 29c vs est. 21c

- Eastman Chemical (EMN) 4Q EPS miss, sees 1Q EPS above est.

- Fifth Street Finance (FSC US) will sell 10m shrs

- Hologic (HOLX) 2Q EPS forecast below est.

- Hovnanian (HOV) will offer $150m of notes, $50m class A common stock, 3m tangible equity units

- ICU Medical (ICUI) sees 2011 EPS $2.25 vs est. $2.22

- Lincoln Electric (LECO) acquired Arc Products. No terms

- McKesson (MCK) sees 2011 EPS $4.82-$5.02. Est. $4.83

- Parexel (PRXL) sees 2011 EPS $1.24. Est. $1.27

- Rent-A-Center (RCII) sees 2011 EPS $2.90-$3.10. Est. $3.01

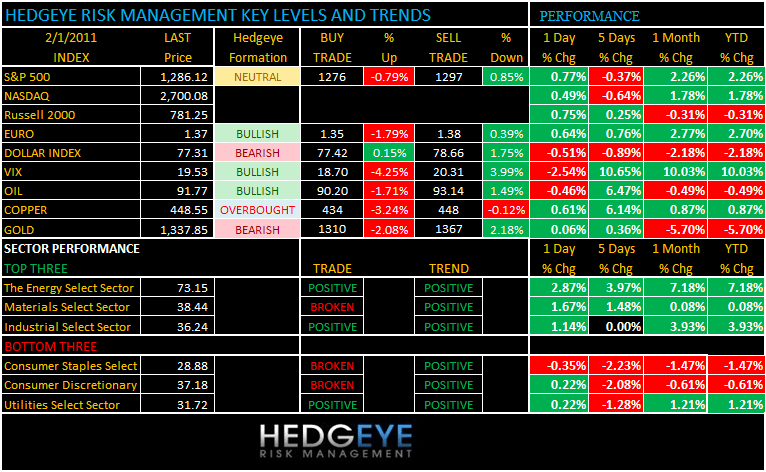

PERFORMANCE:

5 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

- One day: Dow +0.58%, S&P +0.77%, Nasdaq +0.49%, Russell +0.75%

- Month/Quarter/Year-to-date: Month/Quarter/Year-to-date: Dow +2.72%, S&P +2.26%, Nasdaq +1.78%, Russell (0.31%)

- Sector Performance - (6 sectors up and 3 down): - Energy +2.87%, Materials +1.67%, Financials +0.92%, Industrials +1.14%, Tech +0.62%, Healthcare +0.22%, Consumer Discretionary +0.22%, Utilities +0.22%, and Consumer Staples (0.35%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1155 (+3232)

- VOLUME: NYSE 1198.78 (-9.42%)

- VIX: 19.53 -2.54% YTD PERFORMANCE: +10.03%

- SPX PUT/CALL RATIO: 3.06 from 2.32 (+32.49%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were weaker with slight steepening; 2s10s widened ~4bps

- TED SPREAD: 15.33 -0.609 (-3.823%)

- 3-MONTH T-BILL YIELD: 0.15%

- YIELD CURVE: 2.84 from 2.82

COMMODITY/GROWTH EXPECTATION:

- CRB: 341.42 +1.78%

- Oil: 92.19 +3.19% - trading -0.79% in the AM

- COPPER: 445.85 +1.96% - trading +0.44% in the AM

- GOLD: 1,337.07 -0.45% - trading +0.04% in the AM

OTHER COMMODITY NEWS:

- The Thomson Reuters/Jefferies CRB Index of 19 raw materials extended a rally today to the highest since October 2008. This month, cotton and copper rose to records, while hogs climbed to a 24 year-peak. Adverse weather has slashed global crops, and the U.S. and Europe kept borrowing costs low to bolster economic.

- Oil surged to the highest price in more than two years and Brent crude topped $100 a barrel as a seventh day of unrest in Egypt raised concern that supplies may be disrupted.

- Copper rose to a record in London after metal inventories had the biggest decline in almost 11 months, signaling demand is redounding in the U.S.

- Wheat rose in Chicago for the first time in three sessions as North African and Middle East importers may take advantage of lower prices to build supplies in an effort to keep food prices stable amid political unrest. Wheat fell 3.6 percent in the two sessions before today.

- Coffee rose to the highest price since 1997 in New York and reached a 28-month high in London on signs that supplies will fail to keep up with demand. Stockpiles monitored by the New York Board of Trade fell to 1.64 million bags for Jan. 27, the exchange said the next day.

CURRENCIES:

- EURO: 1.3738 +0.64% - trading +0.29% in the AM

- DOLLAR: 77.737 -0.51% - trading -0.35% in the AM

EUROPEAN MARKETS:

- FTSE 100: +0.47%; DAX: +0.68%; CAC 40: +0.66%

- European markets mostly trade higher with the periphery lagging as worries over Egypt took a back seat and sentiment was helped by Wall Street's solid close, firmer markets in Asia and constructive regional economic data.

- Major indices saw session highs early before modestly paring gains. Advancing sectors lead decliners 17-1, with oil & gas +1.8% (though BP trades lower (1.7%) post its update) and chemicals +1.3% leading gainers and financial services and retail leading laggards trading little changed. US futures trade higher

- UK Jan house prices (1.1%) y/y vs con (1.0%)

- Jan Manufacturing PMI, France 54.9 vs con 54.3, Germany 60.5 vs con 60.2, EuroZone 57.3 vs con 56.9, UK 62 vs con 57.9

- Germany Jan unemployment rate +7.4% vs con +7.5%; jobless change (13k) vs con (10k)

- UK Dec mortgage approvals 42.6k vs con 47.0k

ASIAN MARKETS:

- Asian Markets: Nikkei +0.36%; Hang Seng +0.2%; Shanghai Composite +0.3%

- Most Asian markets edged up to follow Wall Street this morning, as worries about Egypt took a back seat in people’s minds.

- In Japan, Honda rose on strong earnings.

- Technology and carmaker stocks rose, but South Korea finished flat.

- Australia finished flat, though resource stocks gained on higher commodity prices. Australia leaves interest rates at 4.75%, as expected

- Taiwan is closed until 8-Feb.

- China January Purchasing Managers Index 52.9 vs December 53.9. January input prices subindex 69.3 vs December 66.7. HSBC January Purchasing Managers Index 54.5 vs December 54.4.