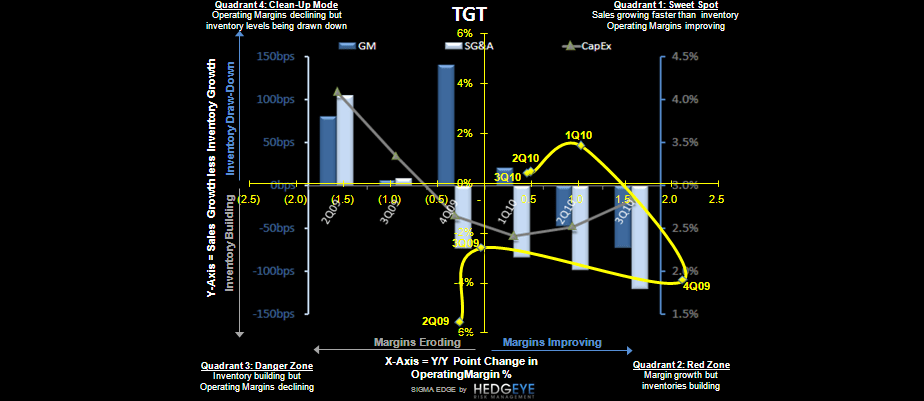

Back in mid-August, we published a note articulating the Bull and Bear cases on TGT. At that time, I was admittedly in the Bullish camp with Brian centered on the other side. So far, many of the bullish underpinnings of the Target outlook have not materialized as I expected- at least not as consistently and not as quickly. That’s not to say that over time the company’s strategies to drive topline growth in an uncertain macro environment are a complete failure. Instead, it is likely that these strategies will take time to materialize and will result in a choppy topline along the way. This, in conjunction with Keith’s bearish stance on the name, leaves us far less optimistic in the near term on TGT shares. Below we YouTube our original bullish thesis (in white) and update each point accordingly (in blue).

Topline has more drivers now, ex-macro, than it has had in some time. The company’s focus on rolling out the 5% rewards/loyalty program and the continued rollout of P-Fresh is accretive to sales. Management says each could be worth 1-2 pts of comp on an annualized basis. Clearly there is something they are seeing in the Kansas City test market (loyalty) and in the P-Fresh remodels to give them confidence. Either way, both company led initiatives offer internally generated sales drivers that others (i.e. WMT) don’t appear to have.

Update: With disappointing same store sales growth of just 0.9% in December and January’s expectations racheted down (in part due to weather) we believe the topline is not likely to show a material snap back in such a short post-holiday period. Yes, we’re aware that electronics and toys were in large part the culprit for underperformance over the holidays, but these categories don’t go away now that Christmas has passed. With the market expecting an acceleration in sales, categories beyond food have to work.

Traffic is the key here, an TGT clearly has momentum. More food and consumables=more traffic. This also leads to opportunity, which in this case may mean a customer picks up an additional non-food item on any given trip. Probably works.

Update: Perhaps the consumables-driven traffic enhancing strategy will take longer to materialize. This concerns us primarily because inflation is now here and most anecdotes suggest that WMT and others are likely to become more aggressive on price. More food does in theory mean more visits. However it also means more competition. In this case, we believe the competitive environment is heating up on the margin, not good for any major player in the space let alone a growing one in TGT.

Management disciplined about opening new units in this environment, instead using capital to fund .com infrastructure and P-Fresh remodels. We like the conservative approach and discipline in not growing for the sake of growth. Yes international is still on the table, but we suspect that means Canada first. There is no rush here and this is a positive for cash flow.

Update: Canada expansion came sooner than we expected and we applaud the move. Yes this will be the biggest use of company’s cash in many years and we think it will be worth it. However, this really has no bearing on the intermediate or near-term as the timing of the deal makes this more noise than anything else over the next couple of quarters. Stores are slated to open in 2013 which means we should expect 2012 to be a year in which start-up costs weigh on the P&L. Keep in mind that the less competitive Canadian market has provided a backdrop for WMT, COST, and BBY to operate their most profitable divisions. This will ultimately be a net positive, but for the longer term.

Aggressive pricing activity from Wal-Mart seems to be a perpetual thorn in the side of traditional grocers and now BJ’s. However, TGT has clearly found a way to compete effectively. The introduction of the “Up and Up” private label brand and differentiated store and merchandise assortment seems to be keeping Target relatively insulated from pricing pressure issues. Perhaps this past quarter is the best example of this, where core retail gross margins were up 5 bps while WMT and BJ both saw pressure as they took prices down. We don’t need to remind anyone of the trend in grocery margins. The bottom line here is Target’s success away from commodity consumables affords better margins.

Update: In the short run, we can’t underestimate the rhetoric and the reality of a more aggressive WMT. Whether you believe the NY Post article from this morning, or the one from last week highlighting WMT’s fear of dollar stores, there is an increasing amount of concern for MORE aggressive pricing activity from the world’s largest retailer. Short of a price war, lowering prices in an inflationary environment is a dangerous spot for TGT to follow, especially when they price against a spread on national brands with WMT.

Credit card portfolio risk gradually dissipating for two reasons. One, the overall credit environment is improving leaving opportunity to reduce reserves. Secondly, Target is shrinking its receivables base as tighter credit restrictions and increased government restrictions no longer allow for unabated growth. Target also discontinued its co-branded Visa program, which leaves future receivables growth entirely tied to store sales.

Update: In conjunction with Canadian expansion comes an announcement that TGT is looking to actively pursue a sale of its credit card receivables portfolio. This would clearly offload a majority of the risk associated with “owning” the portfolio’s receivables and also leave the company with a slightly less complex corporate structure. However, this is not a simple sale, as management notes that such a transaction would need to retain operational control of the financial services business. In other words, a sale is possible but it’s not likely to be a 100% break with the retail business. Still, selling the assets now rather than waiting for credit quality or the regulatory environment to deteriorate makes sense. Still we think near term sales and margins trump the risk of being short if this transaction takes place.

Expense pressure from investments in dot.com will remain through 2011 as the company carries duplicative costs during the transition away from Amazon (TGT’s outsource partner). The flip side here is we should see leverage on such investments begin to materialize in 2012, the year in which Target.com becomes fully operated in-house.

Update: This still holds true but with a new twist. Costs to ramp up Canada in 2012 are more than likely to trump any benefits resulting from a wholly owned and operated .com infrastructure. Longer-term both assets are a positive.

Management has clearly articulated the benefits of adding incremental food/consumables sales into their boxes via the P-Fresh remodel. However, the result over time will be lower gross margins and commensurately lower SG&A. Net, net EBIT rate should remain unchanged. While in theory this makes sense, we know that investors are not fully onboard with trading margin for expense savings. Over time, this will become more clear. In the nearer term, headline gross margins could remain under pressure from this mix issue alone.

Update: In the absence of an accelerating topline, we may be setting up for a situation where both gross margins AND sg&a are under pressure as the company goes up against tough 2010 comparisons in the first quarter. Inflation should not be a surprise to anyone at this point, but the confluence of food/consumable increases and price hikes on apparel and home out of Asia (internally sourced goods) make for a challenging earnings leverage situation.

While TGT offers a more discretionary play vs. WMT, it also offers greater visibility over the intermediate term in my view. The two strategies currently underway to drive topline results have been tested. We already know that inventory management coupled with differentiated product helps Target to drive a higher EBIT structure than WMT. While the Street may be excited to learn that WMT has dialed back rollbacks (after they didn’t work to drive demand elasticity), the non-consumables part of the story is still very much in limbo. This is the single biggest wild card in the WMT story and one that in our view, has not been answered by a few mid-game personnel changes.

Update: Target is quickly becoming a show-me story after having the benefit of the doubt on topline initiatives heading into 4Q. We don’t disagree with management’s strategy over the longer term and believe the company’s merchandising expertise still differentiates the box from WMT and others. However, the margin structure here is changing due to mix and the topline is beginning to show signs of volatility at a time when then the relative outperformance and consistency was expected to take hold. The risks outweigh the reward here in the near-term, especially with January sales being reported later this week and the company having already pre-announced 4Q EPS. Official results and 2011 guidance will come on February 24, long after the debate about WMT’s woes and rub-off impact on TGT become more commonplace.

Eric Levine

Director