This note was originally published at 8am on January 26, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Man’s tongue is soft, and bone doth lack; yet a stroke therewith may break a man’s back.”

-Benjamin Franklin

Sputnik was a Russian space program that launched its first satellite into orbit on October 4th, 1957. A month later, since the Russian translation for the word literally means “travelling companion”, the animal rights folks from Siberia sent a female dog named “Laika” along for the ride.

Notwithstanding that Sputnik was originally designed to carry nuclear weaponry, I found it somewhat ridiculous altogether that the President of the United States tried his best to say this country is having its “Sputnik moment” last night, with a straight face.

No mention of the US Dollar. No mention of inflation. Just space dogs and spending…

There is no doubt that we have an outstanding orator leading this country. When it comes to differentiating between Bush and Obama, that might be it – both of them are all about Big Government Intervention, Big Government Spending, and Big Time US Dollar Debauchery – Obama just makes government “investing” (spending) sound a lot more hopeful.

Hope is not an investment or risk management process.

Back to the interconnected global market’s take on this, the most important real-time market quote I was watching throughout last night’s speech and this morning’s Global Macro trading (which includes currency and bond markets) was the US Dollar Index.

Sputnik, we have a problem. The Bone is Burning again.

As a reminder, given that a country’s currency reflects the overall health of its economy (including employment), monetary policy (including inflation), and fiscal strategy, both the President of the United States and the Fiat Fools who advise him are best served watching what America’s currency is doing both into and out of this speech (down for 4 of the last 5 weeks into it).

Here’s your real-time price and risk management update for Obama’s Burning Bone (quoted down -15bps this morning at $77.80):

- Immediate-term TRADE line of resistance = $79.64

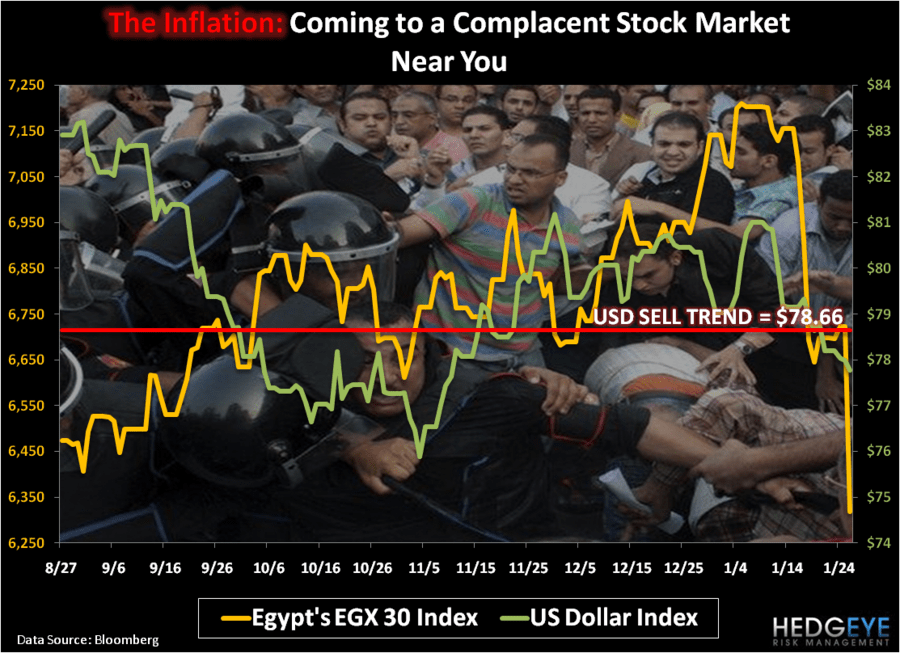

- Intermediate-term TREND line of resistance = $78.66

- Long-term TAIL line of resistance = $81.62

In summary, this means the Burning Bone is bearish (broken) across all 3 of Hedgeye’s core risk management durations (TRADE, TREND, and TAIL). This is not good. And I’ll be selling my US Dollar long position today as a result (we bought it on November 4th when fiscal reform was being promised).

Remember, for some people, the inflation is good.

As Ludwig von Mises said in Argentina in 1959, “if one devalues the currency and the workers are not clever enough to realize it, they will not offer resistance against a drop in real wages, as long as nominal wage rates remain the same.”

That’s America today. High-Low Society 2.0.

And again, I get it – I am long inflation (short bonds) and I will, alongside America’s affluent, get paid on that today.

- We’re long Healthcare Inflation (XLV), which your government says is only 6.5% of your CPI basket (not a joke)

- We’re long Oil (OIL), which is rallying this morning as the Bone Burns

- We’re long Canadian and Chinese currency (FXC and CYB) which track with a positive correlation to global inflation

But the other HALF of Americans who don’t own a damn thing that’s levered to inflation can take Obama’s Burning Bone to the gas pump this morning and rotate on the idea that this is good for them.

Sure, Washington’s dogmatic aristocracy of policy making thinks they are “clever enough” to pull this off. They must think Americans are as stupid as the “investing” ideas of the 112th Congress. If you call Big Government Spending “good for business”, maybe they’ll all sing sweet nothings to each other around their fire places tonight and pray for Lassie to come home.

*Note: this morning’s weekly readings on the US Consumer confidence (after a +91% stock market inflation):

- ABC Consumer Confidence drops for the 2nd week in a row to minus -44 (versus minus -40 two-weeks ago)

- MBA weekly mortgage applications drop another -8.7% this week (vs. -1.9% last wk) as mortgage rates push higher

In the end, inflation kills stocks and bonds. It’s already killing emerging market stocks and US Bonds. And, yes, Egypt’s +12% reported inflation rate is massively understated by a politically oppressive government and that’s contributing to this morning’s civil unrest.

The Bone Burners will tell you that rising US Treasury Yields this morning (2-year UST yields are breaking out above their immediate-term TRADE line of resistance of 0.61%) are all about “growth.”

The Chinese, Indians, and Brazilians, will tell you that rising Municipal and UST bond yields also have something to do with both Burning Bone driven inflation and US credit quality risk.

As India’s sober central banking Governor, Subbarao, said last night, “monetary policy works most efficiently while dealing with an inflationary situation, when the fiscal situation is under control.”

Sorry, Mr. President – good oration of the speech, but you’re not in the area code of enough spending cuts to keep Sputnik’s Bone from looking like it wants to be buried alongside the already broken promises of America’s Mid-term elections.

My immediate-term TRADE lines of support and resistance for the SP500 are now 1286 and 1295, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer