Position: Short Italy (EWI); Short Euro (FXE)

Conclusion: Our current short positions in the Hedgeye Virtual Portfolio of Italy via the etf (EWI) and the Euro (FXE) are working against us as Europe gets a confidence boost from Asian debt demand, positive speculation on a future bailout package for the region, and increased sentiment from ECB President Trichet to fight inflation (ie raise rates) which is supportive for the common currency.

We see this development potentially continuing to play out in the immediate-term, however over the intermediate-term TREND our negative outlook on Europe, especially for the countries with high fiscal imbalances (Italy, Spain, and Portugal), remains intact; the credit market and recent fundaments provide supporting evidence. Our TRADE (3 weeks or less) range on the EUR-USD of $1.35-$1.37.

Don’t Fight these Forces, Near-Term

As an update on our recent work on Europe, it’s clear that European equities (especially the PIIGS) and the EUR versus major currencies (particularly the USD) are getting a sizable near-term boost. While our thesis remains intact that the region’s debt imbalances will weigh to the downside on capital market performance over the next 3-5 years, recent strength in European equities and the common currency can’t be ignored, and we think they’re primarily a function of:

1. A pledge by Japan and China to buy European debt in the first half of January:

- And Asian investors followed through on their promises – in the first auction from the European Financial Stability Facility (rated AAA) on January 25th of €5 Billion 5-year bonds @ 2.89% the Japanese government bought 20% of the issue, with Asian investors snapping up a full 38%. The auction drew considerable demand at €44.5 Billion!

2. Bullish speculation on a “comprehensive package” to tackle Europe’s sovereign debt crisis:

- European Ministers have said that a package to revise the EFSF and map out a permanent mechanism to replace it in 2013 and tighten fiscal rules should be decided on by late March when the European Summit convenes.

- Proposals for this package include:

- boosting the region’s €750 Billion EFSF rescue fund

- helping countries buy back their bonds; and

- lowering interest rates on bailout loans

3. Hawkish commentary from ECB President Jean-Claude Trichet:

- Following the ECB rate decision on 1/13 and in recent interviews at Davos, Trichet is signaling to the market that he 1.) Recognizes rising inflation (particularly in commodities), and is 2.) Determined (as ever) to maintain price stability over the “medium term” to address these pressures. This position diverges greatly from Bernanke’s stance in the US!

- In a separate note we’ll be addressing the timing of an ECB rate hike, however the chart below of the 2YR German Note provides a telling inflection that a hike in the near-term is being priced in. The yield is up a full +50bps since the end of last year.

Here’s the equity performance of the PIIGS since 1/10:

Beware: Long-Term, Sovereign Debt Issues Persist

Over the long term we see significant headwinds from the developing sovereign debt crisis in Europe. We think this “crisis” has a tail of 3-5 years. We don’t see politicians allowing for the failure of the Eurozone member states or the Euro, however what’s clear is that the long road to tighten up the fiscal imbalance of member countries, and construct frameworks to more effectively govern the unequal economies joined under monetary policy and currency will be a great challenge.

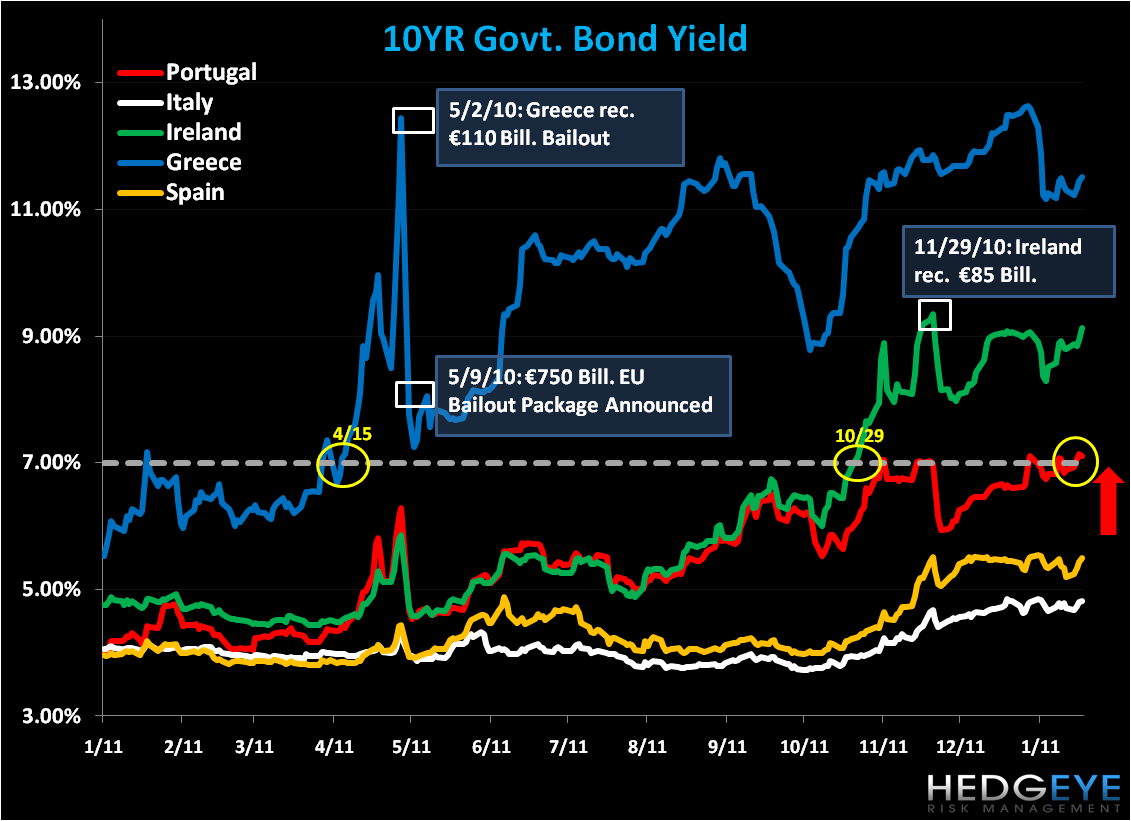

We’re not of the opinion that governments across the region will be able to meet their debt and deficit reduction targets over the next 2-4 years. One clear signal we’ve witnessed for the last year is a trend of rising credit yields for the PIIGS despite bailouts in Greece and Ireland. We think Portugal, Spain, and Italy are next on the block.

As the chart above demonstrates, rising yields put increased pressure on the sovereigns as they issue new debt, and so begins the viscous cycle of nations chasing yields higher to capture demand to meet future obligations. We’ve seen, using Greece and Ireland as examples, that a yield of 7% or above is a critical inflection line -- in both cases after the line was violated to the upside, a bailout came in mere weeks.

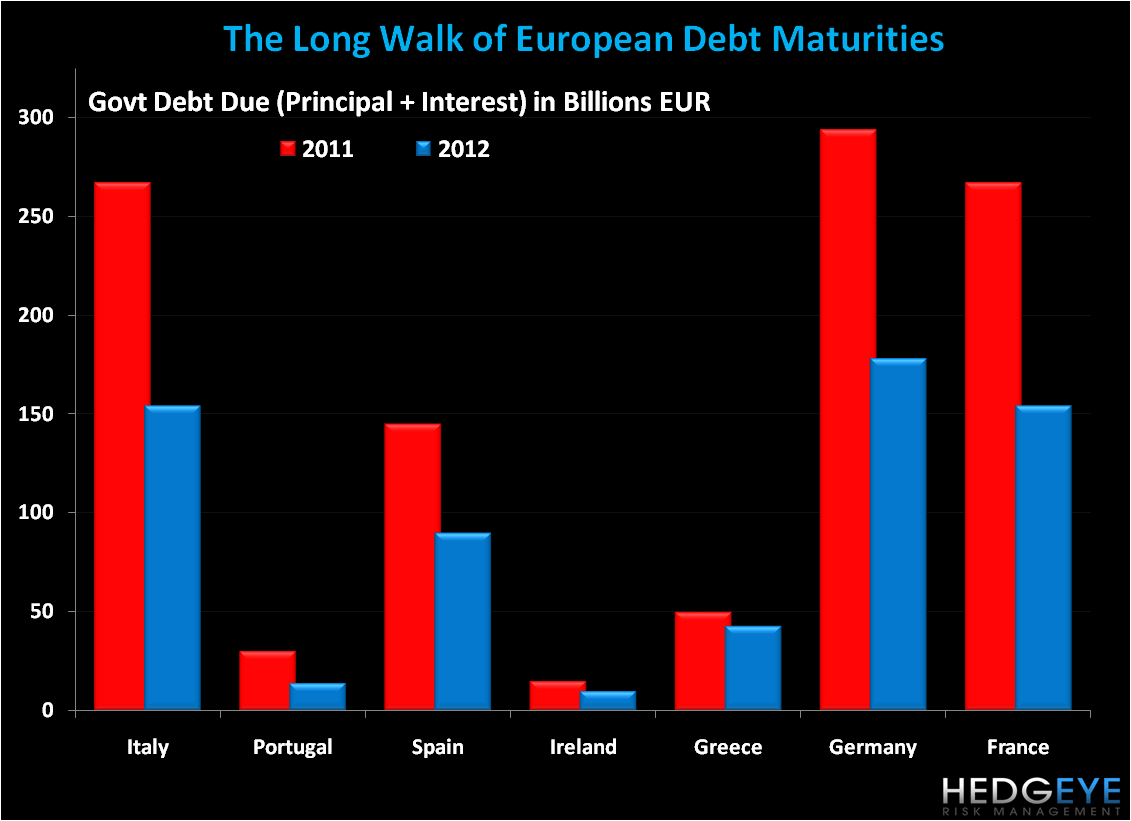

While we applaud the concurrent austerity programs throughout Europe to suppress spending and increase revenue vis-à-vis tax hikes, slower growth (and therefore less revenue) should follow, another headwind for fiscally imbalanced countries (and their equity markets) that have sizable debt obligations due this year and next (see chart).

Matthew Hedrick

Analyst