The guest commentary below was written by longtime Hedgeye "Power User" Jeff Tyburski, Founder of Your Financial Sherpa. Jeff began his career as an engineer for 13 years, then worked as a senior analyst and portfolio manager for over two decades. He graduated from University of Rochester where he earned an MBA in finance and is a CFA Charterholder.

An Epiphany on Saving Money?

An epiphany moment is a lightning bolt of insight that changes you in some way. The chances of having an epiphany moment increase when you break with conventional wisdom and look at an old issue in a new way. Let’s take a look at ‘how to save money’ from a new perspective. Maybe, just maybe, you will have an epiphany moment.

How to save?

Pilots have checklists. Chefs have recipes. Athletic teams have playbooks. Is there a repeatable method to successfully save?

Conventional Thinking on How to Save Money

The chart below captures a traditional approach to saving.

To save, spend less than you earn. While simple, traditional, and even intuitive, this approach is flawed. The problem is that the focus is on spending and not saving. Some months you succeed, spending less than you earn. The result is you save.

Other months, you are surprised at an unexpected expense (e.g., a car repair bill) or you didn’t plan for an expected, but not monthly, expense like car insurance (typically billed twice per year). Or you just failed to control discretionary spending and went out to eat too many times or spent too much on activities and entertainment.

On the months when you came up short, you probably kicked yourself and swore you’d budget better going forward. But budgets are tedious and work about as often as New Year’s resolutions. The problem with budgets is that people try a line-item approach and get confused or frustrated not knowing how to handle activities they do inconsistently or bills that are variable.

A Better Approach on How to Save Money

I am an advocate for a different approach ... the ‘Save First’ approach. The chart below illustrates this better way to save.

Here, the focus is on saving not spending. Here, from your earnings, save first, literally pay yourself first, then live off what remains. It sounds deceptively simple, but you’d be surprised how doable it is.

It is not only doable, but also potentially life changing.

One of the oldest books in personal finance, the classic The Richest Man in Babylon, recommends this approach. If you earn 10 coins (recall, the story was in the time of Babylon), pocket one, and structure your life around the other nine.

It is more achievable than you’d guess.

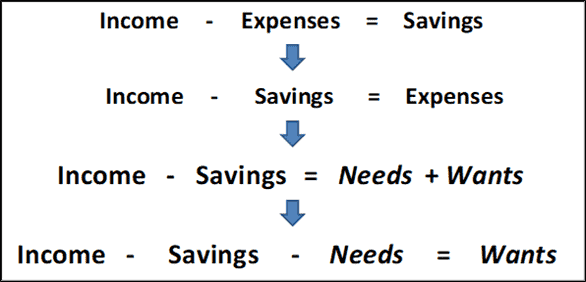

A Formula for Success

‘Save First’ and live off what remains. This is obviously easier said than done. A little algebra goes a long way in giving you more of an action plan. Start at the top of this graphic and work your way down:

The top formula is the traditional (yet flawed) approach in which you focus on spending.

With a minor bit of rearranging, the second formula is the ‘Save First’ approach.

The third formula from the top simply acknowledges that ‘Expenses’ consist of ‘Needs’ and ‘Wants’.

One final rearrangement produces the bottom formula, a formula to live by.

Income minus Savings minus Needs equals Wants. Earn. Save first. Meet your true Needs. Spend ‘what is left’ on some Wants. We can have future conversations on how to set and achieve savings goals and how to assess and fine tune your true Needs, but one initial take-away is how ‘what’s left’ for Wants is simpler to picture than with a budget. With a pile of money left over after saving first and meeting true Needs, you can simply count down on discretionary purchases until you know it is time to pack your lunch or hunker down until the next paycheck. Picture ‘what’s left’ for Wants as an indicator that starts out green, flashes yellow, then hits red.

Is a Formula for Success a Guarantee of Success?

While ‘Income – Savings – Needs = Wants’ can lead to success, it is no guarantee of success. Even if you have high income, you may fail to set good savings goals or pay yourself first. Even with high income, you could still spend too much (on Needs that are actually luxuries and excessively on Wants).

In the end, while there is no guarantee for success, there is a guarantee for failure. That is, if you earn very little, you are unlikely to be able to meet your true Needs, let alone ‘Save First’ or have money left for Wants.

We began by saying “you can’t invest if you haven’t saved”. That is true. But it is also true that “you can’t save if you don’t earn”. Thus, financial literacy educational content, if it is to succeed, needs to delve deep into how to get and hold onto a good job, with growing earnings potential, in our competitive and changing world. Financial literacy must also help you set good savings goals and understand your true spending needs.

* * *

About Your Sherpa

Your Sherpa has a unique approach to teaching financial literacy, offering a roadmap from start to finish (a true personal process with the life skills and mindset to succeed). Click here to visit the website.