Notable news items/price action moves over the past twenty-four hours.

- KKD gained 6.5% on strong volume, outperforming the space on news that Robert Stiller, GMCR chairman and founder, was disclosing a 5% stake in the company.

- BAGL gained 5.2% on accelerating volume yesterday. News also hit the tape that CEO Jeffrey O’Neill filed to sell 8,200 shares on 1/18/2011.

- MCD UK President and CEO, Jill McDonald, told the Daily Mail that the company is looking at expanding the range of hot drinks on offer at MCD stores. She says that 90% of the firms increase in sales has been due to traffic rather than any increase in average check. She stressed that there are savings MCD can make in their operational processes, but conceded that prices may have to be a “tiny little bit” more expensive due to higher food prices.

- MCD estimates at Goldman Sachs cut today.

- SBUX estimates cut at Janney Montgomery.

- RRGB refuted Oak Street Capital Management’s demand for new board appointees and more shareholder-friendly management practices yesterday, stating, “We…have been working to incorporate the views of multiple key constituencies including our shareholders and franchisees”.

- EAT reports today and investors will eager to hear how the company’s sales have performed during the most recent quarter and how its cost-cutting initiatives have been working.

- PNRA underperformed on strong volume.

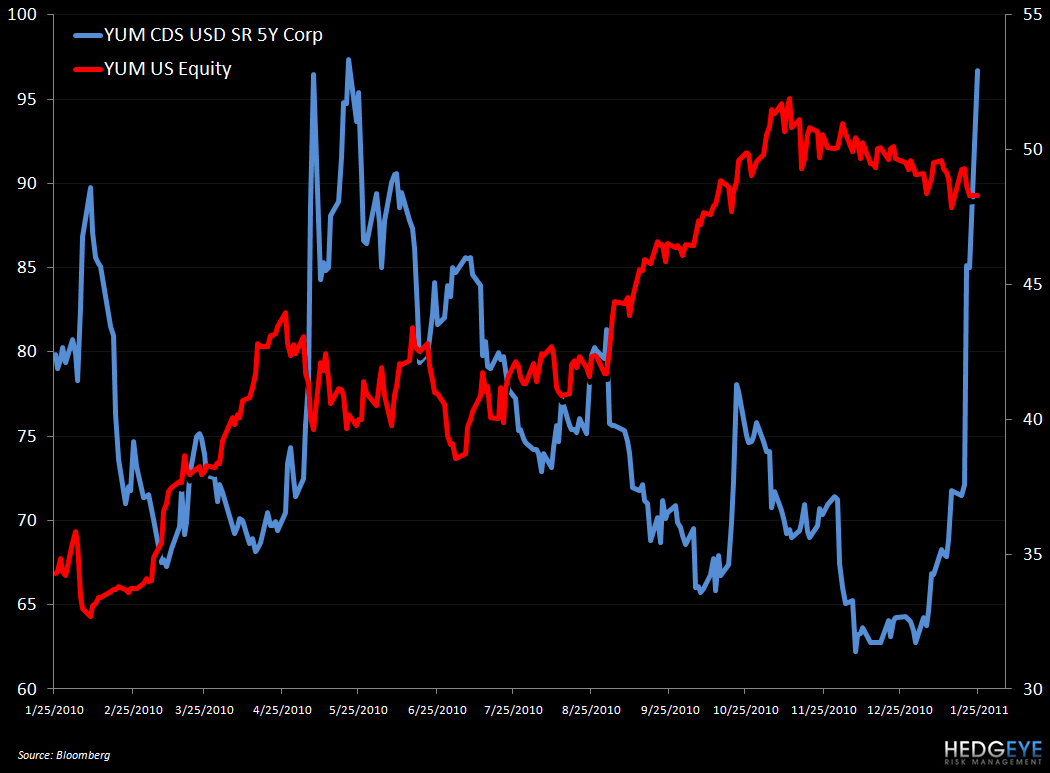

- YUM stock performance has slowed slightly over the past month. I was interested to observe the company’s 5 YR CDS blow out over the past couple of days (chart below).

- DRI have opened a combination Red Lobster/Olive Garden in Flagler County, Florida (picture below). The county has the highest unemployment rate in Florida, at 15.7%.

Howard Penney

Managing Director