TODAY’S S&P 500 SET-UP - January 25, 2011

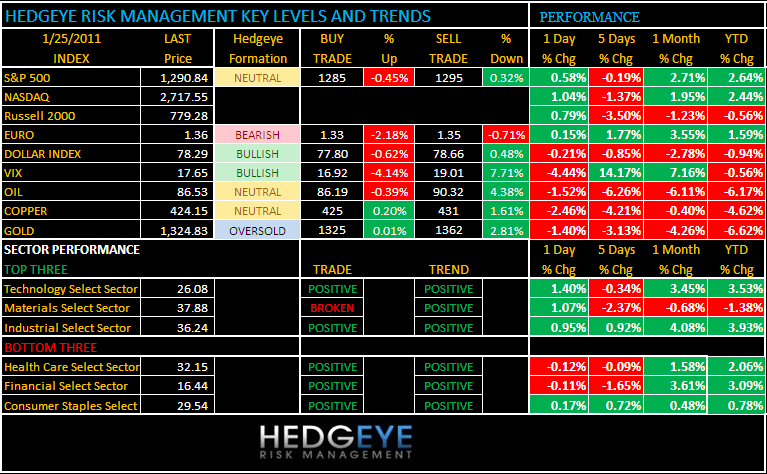

Equity futures are trading below fair value in reaction to an unexpected decline in UK Q4 GDP, which has knocked down some European markets. Today's calendar shows a marked pick up in data releases with S&P/Case-Shiller House price index, Consumer Confidence, Richmond Fed Manufacturing index due out ahead of President Obama's State of the Union address tonight. As we look at today’s set up for the S&P 500, the range is 10 points or -0.45% downside to 1285 and +0.32% upside to 1295.

MACRO DATA POINTS:

- ICSC-Goldman Chain Store

- Redbook Chain Store

- Nov Case-Shiller Home Price Index

- Jan Consumer Confidence

- Nov FHFA House Price Index

- API Crude Inventories

- US ABC Consumer Comfort

- President Obama delivers State of the Union Address

EARNINGS:

- Companies due to report before the open: AKS, BHI, BTU, COH, DD, DGX, EMC, GLW, GWW, HOG, JNJ, KEY, KMB, MDD, 3M, NEE, RE, SHW, TLAB, TRV, VZ, WAT, X

- Companies due to report after the close: ALTR, BXP, CA, DV, GILD, JNPR, MOLX, NSC, SYK, TSS, YHOO

PERFORMANCE:

The XLB remains the only sector that is broken on the Hedgeye TRADE - 8 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

- One day: Dow +0.92%, S&P +0.58%, Nasdaq +1.04%, Russell +0.79%

- Last Week: Dow +0.72%, S&P -0.76%, Nasdaq -2.39%, Russell -4.26%

- Year-to-date: Dow +3.48%, S&P +2.64%, Nasdaq +2.44%, Russell (0.56%)

- Sector Performance - (7 sectors up and 2 down): - Tech +1.40%, Materials +1.07%, Industrials +0.95%, Consumer Discretionary +0.40%, Utilities +0.56%, Consumer Staples +0.17%, Energy +0.37%, Healthcare (0.11%), and Financials (0.12%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1220 (+1609)

- VOLUME: NYSE 961.93 (-24.01%)

- VIX: 17.65 -4.44% YTD PERFORMANCE: -0.56%

- SPX PUT/CALL RATIO: 2.06 from 1.57 (+31.50%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were little changed.

- TED SPREAD: 16.11 +0.811 (5.303%)

- 3-MONTH T-BILL YIELD: 0.16%

- YIELD CURVE: 2.78 from 2.81

COMMODITY/GROWTH EXPECTATION:

- CRB: 332.70 -0.39%

- Oil: 87.87 -1.39% - trading -1.58% in the AM

- COPPER: 434.85 +0.92% - trading -2.50% in the AM

- GOLD: 1,343.68 +0.02% - trading -1.41% in the AM

COMMODITY HEADLINES:

- Gold falls to a 2 month low

- Coca tests the 1979 peak on Ivory Coast political unrest

- Oil fell to the lowest level in five weeks as Saudi Arabian Oil Minister Ali al-Naimi signaled OPEC may bolster production to meet increasing fuel demand.

- French President Nicolas Sarkozy said regulation of commodity markets will be a priority as he leads the Group of 20 nations this year, and inaction may cause food rioting in the world’s poorest countries.

- Natural gas producers increased bearish bets to the highest in almost three years, joining hedge funds amid forecasts that near-record output will swell a fuel surplus.

- Hedge funds are unloading bullish bets on gold as a slide in prices sends the metal to its worst start to a year since 1997.

- Copper output in Zambia, Africa’s biggest producer of the metal, jumped 17 percent in 2010, beating government forecasts, said Kanguya Mayondi, head of public relations at the Lusaka-based central bank. The preliminary estimate showed production climbed to 819,159 metric tons compared with 697,700 tons in 2009, Mayondi said in an e-mailed response to questions on Jan. 21.

- CORN - This past Friday the legacy (three-line) report showed commercials net-short 396,212 corn contracts, a 52-week low.

- Cotton prices have risen to a record as mills face extremely low supplies. ICE March cotton, the US benchmark, rose by the 5 cent daily allowable limit to $1.6194 per pound on Monday, the highest in the 141-year history of the New York exchange and its predecessors.

CURRENCIES:

- EURO: 1.3642 +0.15% - trading -0.18% in the AM

- DOLLAR: 78.050 -0.21% - trading +0.16% in the AM

EUROPEAN MARKETS:

- FTSE 100: -0.62%; DAX: +0.29%; CAC 40: +0.05% (AS OF 6:30 AM EST)

- European markets are mixed and in the case of the FTSE100 reversing gains after an unexpected contraction in UK economic growth in Q4.

- The regions corporate results were broadly well received led by Siemens and Ericsson.

- Declining sectors lead advances 10-8. Banks (2.3%) and insurers (1.0%) led fallers, with autos +1.2% and industrials +1.1% leading gainers.

- UK Q4 preliminary GDP +1.7% y/y vs con +2.6% and prior +2.7%, (0.5%) q/q vs consensus +0.5% and prior +0.7%

- Germany Feb GfK 5.7 vs con 5.4

- France Dec consumer spending +0.6% vs con +0.4%

ASIAN MARKTES:

- Nikkei +1.2%; Hang Seng (0.1%); Shanghai Composite (0.68%)

- Asian markets are mixed after India raised interest rates, although the move had been expected.

- Exporters, consumers rally on overseas demand outlook.

- Techs climb after Texas Instruments earnings beat estimates.

- Materials gained as metal prices rose earlier.

- All 33 sectors went up in Japan +1.15%, with the mining sector performing best. Japan leaves overnight call rate at 0.0-0.1%.

- Australia rose +0.46% when inflation came in below expectations, reducing the chance for a rate hike. Australia Q4 CPI +0.4% seq vs 0.7% consensus, +2.7% y/y vs 3.0% consensus.

- South Korea rose +0.22%, with financial firms higher on bargain-hunting.

- Hong Kong ended flat despite the fact that Tencent Holdings rose 5% on reports it will launch a CNY5B fund to invest in games.

- China fell (0.68%) again on worries about a rate hike. Sinopec lost 1% and was the biggest drag on the market. Most banks rose in reaction to the central bank’s trying to put some liquidity into the system.