Financial Risk Monitor Summary (Across 3 Durations):

- Short-term (WoW): Positive / 4 of 10 improved / 2 out of 10 worsened / 5 of 10 unchanged

- Intermediate-term (MoM): Positive / 7 of 10 improved / 2 of 10 worsened / 2 of 10 unchanged

- Long-term (150 DMA): Positive / 4 of 10 improved / 3 of 10 worsened / 3 of 10 unchanged / 1 of 10 n/a

1. US Financials CDS Monitor – Swaps were mixed across domestic financials, tightening for 15 of the 28 reference entities and widening for 13. The moneycenters saw the greatest tightening of the group, while widening was concentrated in mortgage insurers.

Widened the most vs last week: PMI, MTG, RDN

Tightened the most vs last week: BAC, C, WFC

Widened the most vs last month: MTG, ACE, CB

Tightened the most vs last month: LNC, MET, MBI

2. European Financials CDS Monitor – Banks swaps in Europe tightened across the board last week. Swaps tightened for 38 of the 39 reference entities.

3. Sovereign CDS – Sovereign CDS continued to fall last week, retracing to their levels of late November.

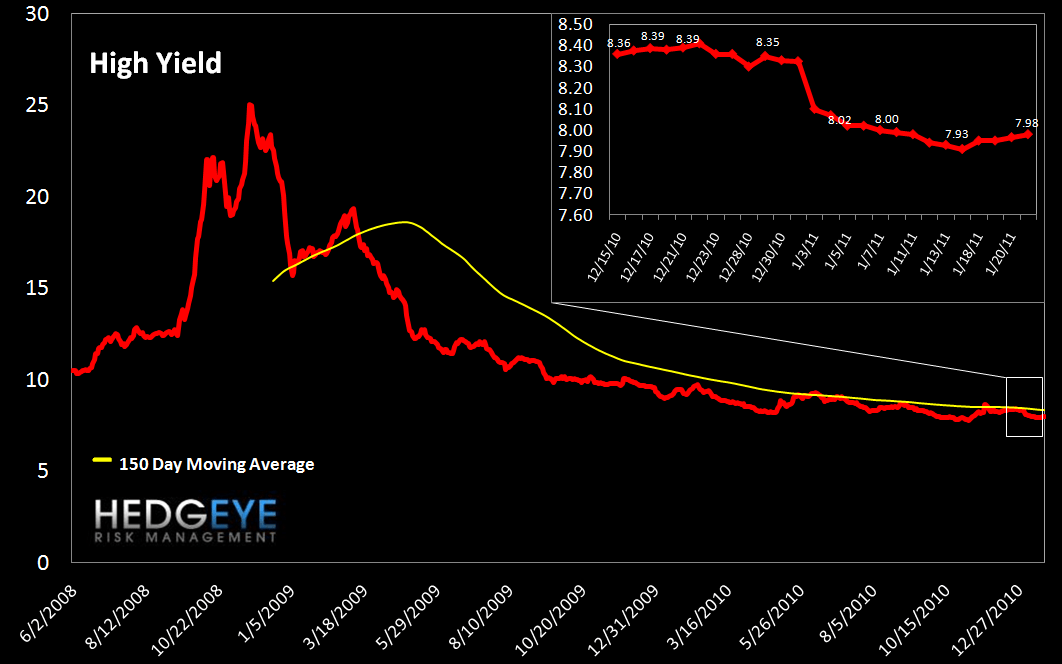

4. High Yield (YTM) Monitor – High Yield rates rose 7 bps last week, closing at 7.98 on Friday.

5. Leveraged Loan Index Monitor – The Leveraged Loan Index continued to rise, closing at 1605, 6.5 points higher than the previous week.

6. TED Spread Monitor – The TED spread held nearly flat, ending the week at 15.3 versus 15.8 the prior week.

7. Journal of Commerce Commodity Price Index – Last week, the index fell 3 points, closing at 32.6 on Friday.

8. Greek Bond Yields Monitor – We chart the 10-year yield on Greek bonds. Last week yields rose 19 bps.

9. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on four 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. Our index is the average of their four indices. Spreads fell last week, dropping 21 bps to 198.

10. Baltic Dry Index – The Baltic Dry Index measures international shipping rates of dry bulk cargo, mostly commodities used for industrial production. Higher demand for such goods, as manifested in higher shipping rates, indicates economic expansion. The index fell to a new low of 1370 as flooded coal mines in Australia continued to pressure demand.

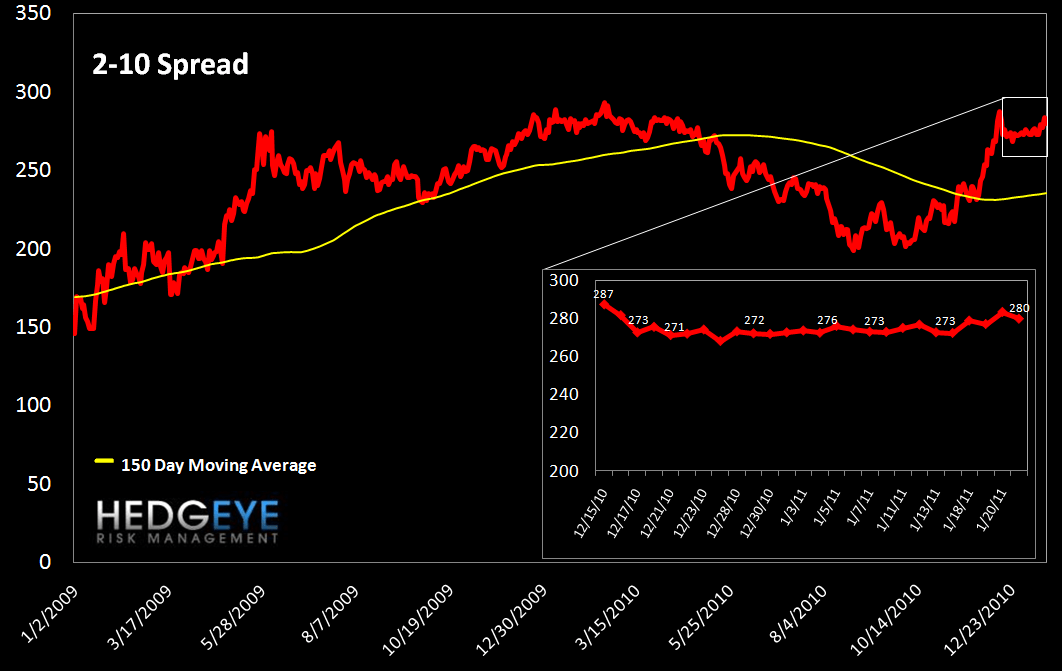

11. 2-10 Spread – We track the 2-10 spread as a proxy for bank margins. Last week the 2-10 spread widened slightly to 278 bps.

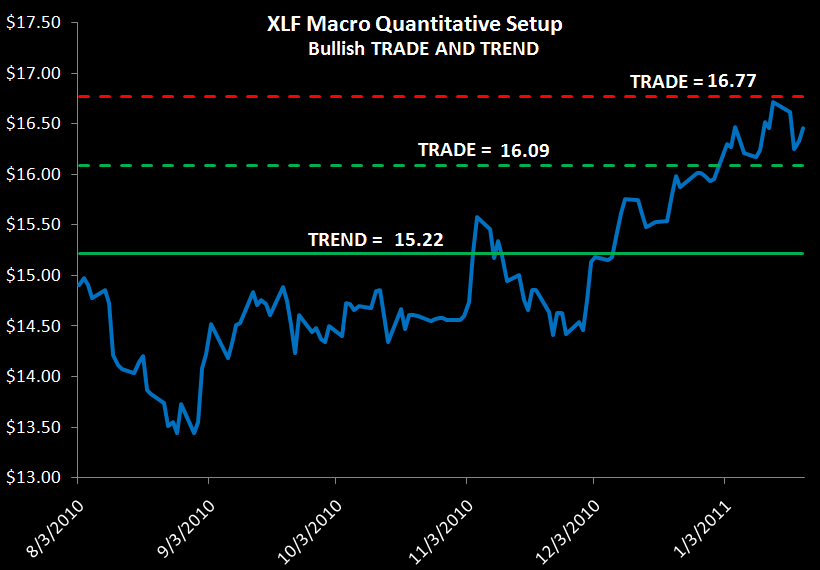

12. XLF Macro Quantitative Setup – Our Macro team sees the setup in the XLF as follows: 1.9% upside to TRADE resistance, 2.3% downside to TRADE support.

Joshua Steiner, CFA

Allison Kaptur