This note was originally published at 8am on January 14, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The fact that we are today to debate raising America’s debt limit is a sign of leadership failure.”

-Senator Barack Obama, March 2006

Our CEO Keith McCullough has been out most of this week recovering from a surgery to reattach his Achilles tendon. I’ve known Keith for upwards of fifteen years, including three years as college hockey players, so I can rightly say that I’ve seen the man in a few precarious situations, but never did I think he would injure himself on the squash courts. So when it comes to risk management for the aging college athlete, leave the squash to those that grew up playing it at prep schools is my advice on a go-forward basis.

With Keith out, I’ve had to live a week in his shoes. I’m not prone to giving the proverbial tire pump, but, candidly, it’s not easy to write a morning strategy note and prep for a morning call every morning starting at 5 a.m. As it relates to President Obama and the quote above, I think he is now realizing what it’s like to live in another man’s shoes, as well. (Life as President is much different than as a member of Congress it seems.)

Members of Congress in Washington basically have free rein to chirp. While Presidents can chirp as well, they also have to make decisions. Obama’s quote (chirp) above was prescient back in 2006, but in the coming weeks he will have to push to get the debt ceiling raised because, as President, he needs to keep the country running. The advisors hired to chirp on his behalf have been out in full force making sure he has the political cover to get this done.

Specifically, White House economic advisors Austan Goolsbee recently had this to say about the debt ceiling:

"This is not a game. You know, the debt ceiling is not something to toy with. … If we hit the debt ceiling, that's essentially defaulting on our obligations, which is totally unprecedented in American history. The impact on the economy would be catastrophic. I mean, that would be a worse financial economic crisis than anything we saw in 2008."

Now, if that’s not chirpy, I don’t know what is.

Freshman Senator Rand Paul was not to be outdone though, and chirped back his own proposal:

“I can't imagine voting to raise the debt ceiling unless we're going to change our ways in Washington. I am proposing that we link to raising the debt ceiling — that we link a balanced budget rule, an ironclad rule that they can't evade.

We have to change the rules and we have to say to Washington, Balance the budget. You have to do it by law. And then I'll vote to raise the debt ceiling. But only if we have an ironclad balanced budget rule that we attach to the debt ceiling.”

Ironically, the best assessment of the debt and debt situation was probably Senator Obama back in 2006. The fact is that we are in this fiscal situation today because of failed leadership. This is failed leadership that has transcended administrations and political parties. It is because the United States has created long term obligations in the way of social security and healthcare that we can’t fulfill, and administrations have overspent on discretionary items when times were good. (In fact, our friend Karl Rove even acknowledged to us that the one regret he had was that the Bush administration didn’t do a better job on discretionary spending.)

In the coming weeks, the debate over the debt ceiling will increase in velocity and volume. The fiscal conservatives, particularly those who were swept in with the Tea Party in the most recent midterm, will be on the soap box and will be chirping like never before. Unfortunately, even Goolsbee’s language and delivery is somewhat inflammatory, and as a nation, we really have no choice, but to increase the limit on the debt ceiling.

In the coming months, there are three key catalysts that will take the debate over the debt and deficit to a heightened level, these are:

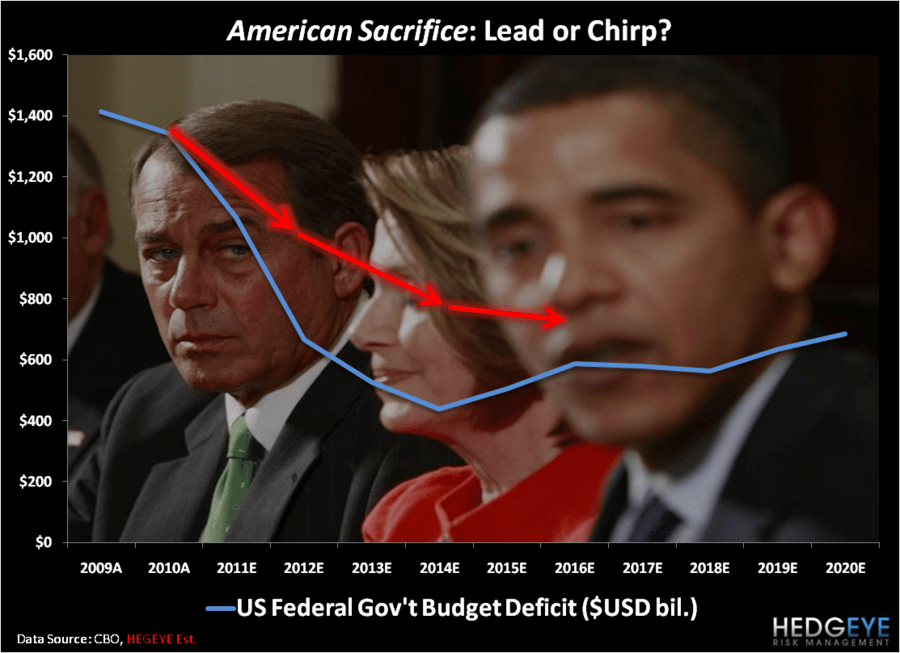

1) Late January - Congressional Budget Office deficit projections will have to be raised dramatically for the next few years. We’ve highlighted their projections in the Chart of the Day, and, simply put, the numbers are too low for what we’ve already seen in Q1 of fiscal 2011.

2) Mid February - President Obama’s draft budget proposal will be submitted in early February. This proposal will be more heavily scrutinized than any budget in recent memory and since so few of the line items can be played with in the short term, they’ll surely not satisfy the fiscal conservatives.

3) Early March - Finally, the vote on the debt ceiling will occur sometime before March 4th. This is when the debate will reach its highest pitch even though the outcome is already known, which is the ceiling must go higher.

We believe the outcome of all of this could be, American Sacrifice. This is the idea that this debate actually drives our politicians to implement meaningful initiatives that will begin to reverse the fiscal predicament we are facing. If we do start to see fiscal improvement, or at least positive discussions in that direction, it will be bullish for the U.S. dollar.

That said, as it relates to Washington, one never knows and productive legislation will actually require these politicians to set aside their “chirp, or be chirped” politicking, and help move the country forward.

Yours in risk management,

Daryl G. Jones