Position: Long Germany (EWG); Short Italy (EWI) and Euro (FXE)

As two days of EU meetings conclude in Brussels today it appears that nothing definitive was decided on by the 27 ministers short of renewed discussions following last week’s rumors that the region’s bailout fund could be increased, possibly from €750 billion to €1 Trillion. While the Germans continue to flip-flop on the issue (depending on who you talk to) our bet is that if the funding were to increase (very likely) you'd see a pot far greater than €1 Trillion to meet the peripheral debts, especially the bigger exposures of Italy and Spain.

In any event, all eyes are turned to bond auctions again this week. On a bullish note, Spain sold €4.5 Billion of 12 month bills at 2.947% today, versus 3.449% on December 14th.

Tomorrow: Portugal issues short term bills

Thursday: Spain issues long term debt maturing in 2020 and 2024, a critical gauge for investor demand and yield premium offered

Rumors flew around today that Russia could buy European bonds, following commitments from China and Japan earlier this month. While Russia has impressive FX and gold reserves (3rd largest in the world at $480.7 Billion), given the economic and political instability in Russia we think this rumor could be off base. Yet over the near term the rumor (like the increased funding talks in Brussels) offers another support mechanism for European equities and the EUR.

In contrast, the credit markets of the PIIGS + Belgium have seen little arrest with yields continuing to rise since last Friday (see chart). Of note is that Portugal's 10YR yield is now above 7%, a level that proved an important upward momentum line for both Greece and Ireland.

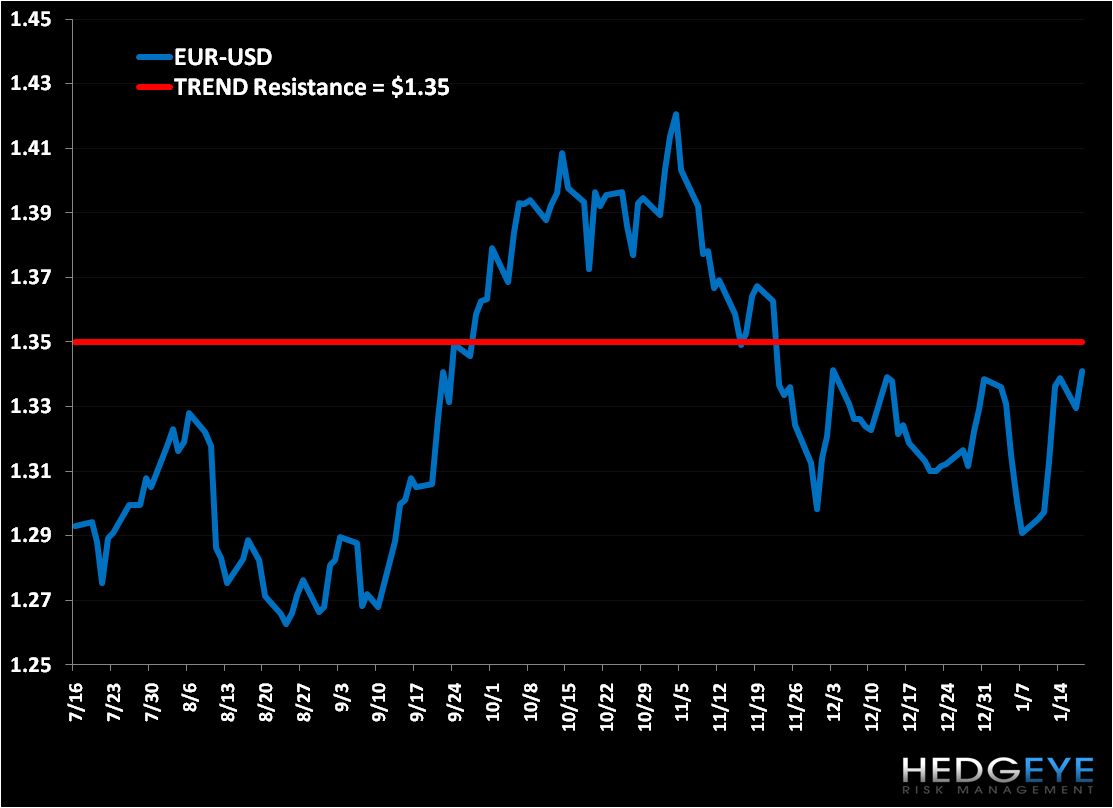

Below we give our levels for the EUR-USD. We’d be short the EUR-USD with impunity at $1.35, its intermediate term TREND level of resistance.

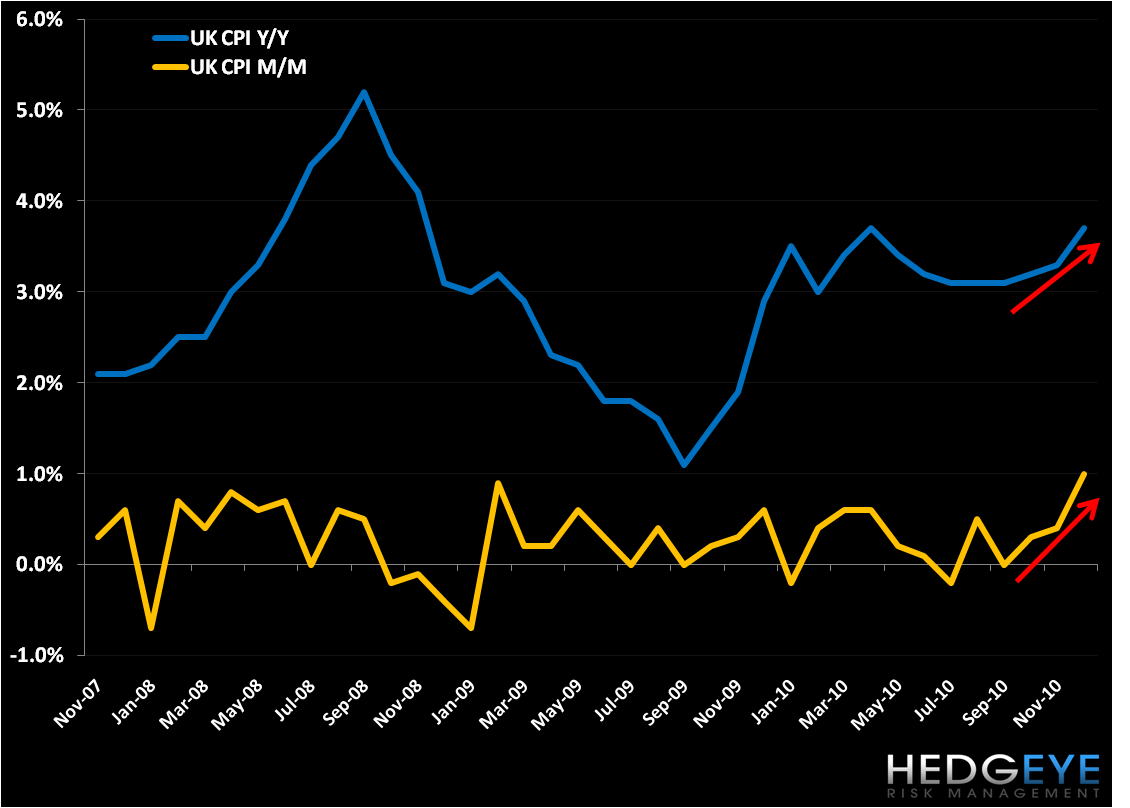

UK Inflation Punctuating

UK CPI registered 3.7% in December year-over-year, versus the previous month of +3.3%. We’ve been hitting on the risk of rising inflation in the UK for months, however with this huge jump in December there’s even more pressure on the BOE to act. Gains came from food and fuel prices and statements out of PM Cameron today suggest just how mainstream the inflation issue has become:

“I tend to be a ‘now man’ because we’ve had constant reassurances that inflation will fall and it hasn’t fallen… I’d rather see them start moving up gradually than go up in a huge jump, perhaps in the autumn.”

Considering that we’ll likely see more inflation pressure in January given that VAT was increased from 17.5% to 20% into the new year, we believe the BOE will have to bite the bullet over the next few months and raise rates (despite the threat of further choking off growth) to contain inflation.

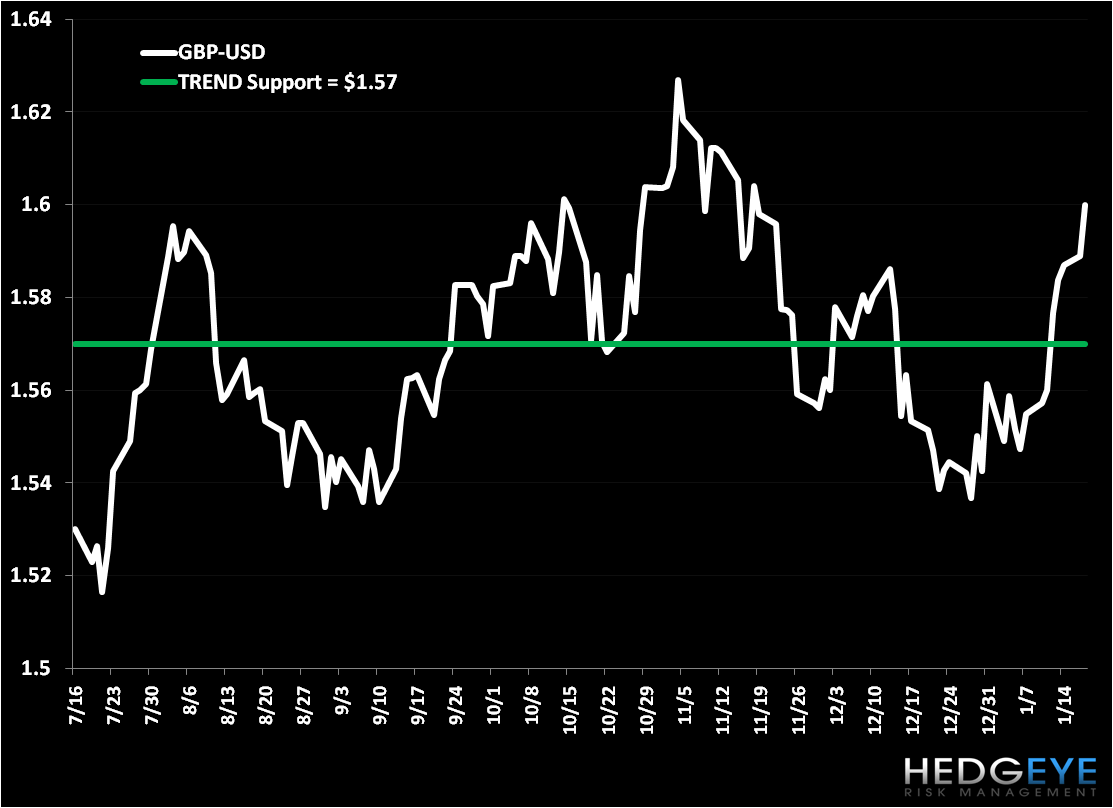

A rate hike should bolster the Pound versus major currencies. As the chart below shows, and given that we think the BOE will raise rates before the ECB, we like the GBP versus the USD above its intermediate term TREND line of $1.57, which it has currently broken through.

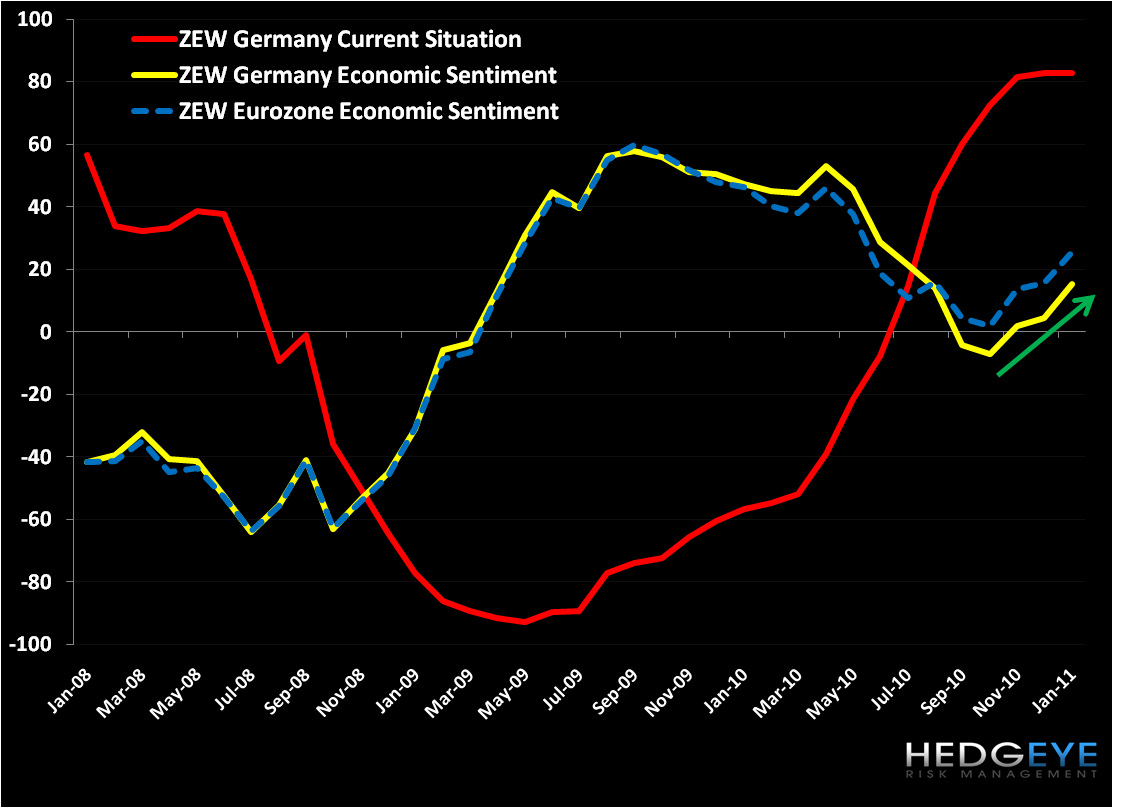

German ZEW Gains

Germany continues to impressive regarding the majority of the fundamentals we track. The chart below of the ZEW economic survey shows a significant gain in the Economic Sentiment survey, from 4.3 in December to 15.4 in January, with a more mild gain in the Current Situation, from 82.6 in December to 82.8 in January. (We’ve noticed that Economic Sentiment has been a much more predictive gauge than Current Situation).

We continue to like Germany as the sovereign debt dichotomy plays out in Europe. We're currently long Germany via the etf EWG in the Hedgeye Virtual Portfolio.

Matthew Hedrick

Analyst