Conclusion: I remain positive on Brinker for the intermediate term given the significant progress the company is making on its back-of-house margin-enhancing initiatives. In November I reaffirmed my positive view on the stock and now the lunch day part initiatives management had spoken about are being rolled out. I expect these initiatives to positively impact comps for Chili’s, which I expect to be in positive territory in 2HFY11.

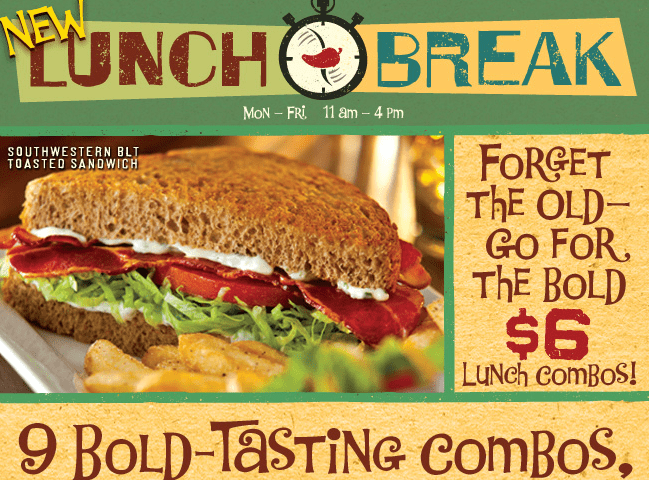

The lunch day part has traditionally been difficult for Chili’s and I am encouraged by management’s efforts to drive traffic during the 11am-4pm slot. In my most recent post focused on Brinker, I outlined the lapping of menu changes made last year, “2 for $20” becoming a permanent fixture on the menu, and the new lunch menu rollout as being three factors that would lead the concept to positive same-store sales in 2HFY11. Below I include a screenshot of the promotion email and also EAT’s quadrant chart, which shows EAT currently in the “life-line” quadrant with positive year-over-year margin growth and negative same-store sales. I anticipate a migration into the “nirvana” quadrant (positive year-over-year margins and same-store sales) in 2HFY11.

Howard Penney

Managing Director