Restaurant sales results and presentations are ongoing; here is a look at yesterday’s price moves and news items.

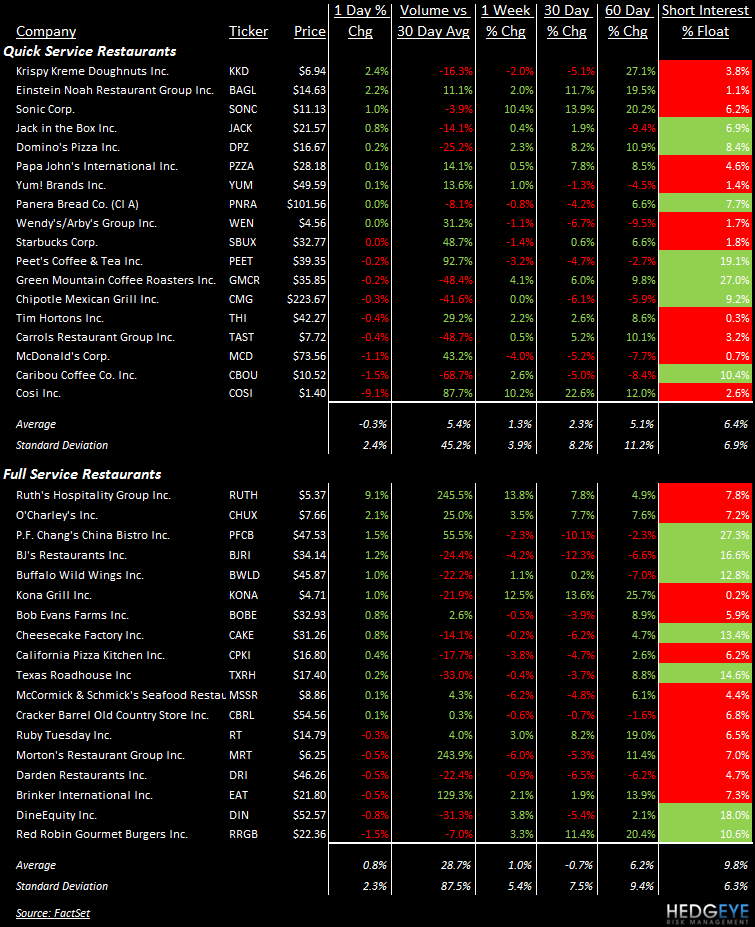

- CAKE released sales this morning ahead of their presentation at the Cowen Conference today. The Q4 comp result for The Cheesecake Factory and Grand Lux Café increased 0.9% in Q4. Given that the company grew traffic for the fourth consecutive quarter, and there is roughly 1.5% of price on the menu, it seems that CAKE’s average check problem has not gone away.

- CAKE reaffirmed 2011 guidance of annual comp sales up 1%-3% and 6-9 new restaurants.

- RUTH outperformed the space yesterday, gaining on strong Q4 sales results that were released yesterday including comps of +9.2%

- Overall, the strong relative outperformance continues into 2011

- Chains focused on the higher end customers and the business traveler continue to show the best trends (RUTH and MRT. Also in retail TIF posting good numbers today)

- COSI corrected after a strong first week to the year

- MCD declined on strong volume. I retain my bearish view for MCD in 2011 and am holding a conference call with clients to go over the fine details on Friday at 11am. Email for details.

Howard Penney

Managing Director