“The best way to destroy the capitalist system is to debauch the currency.”

-John Maynard Keynes

This year I am going to try my best to kick off each week with a Global Macro recap of the week prior. I’ll also try to address what decisions I made in the Hedgeye Asset Allocation Model to reflect ongoing and ever-changing Global Macro risks.

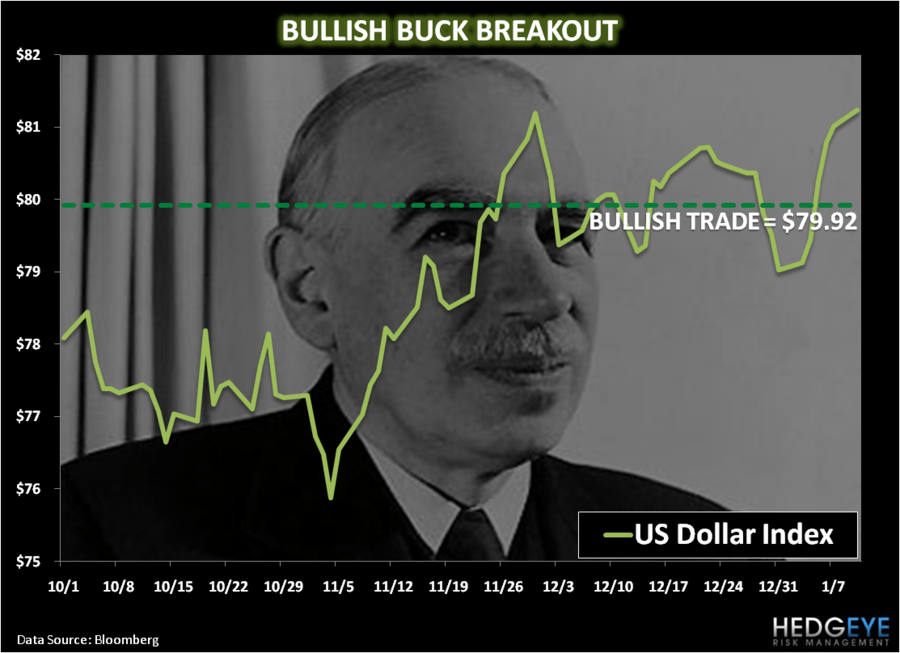

The biggest move that mattered last week was the Buck’s Breakout above my immediate-term TRADE line of $79.92 on the US Dollar Index. After taking a breather into December end, the US Dollar Index is now bullish again on both our immediate-term TRADE and intermediate-term TREND durations.

With the US Dollar Index closing up +2.6% on the week (up for the 8th week out of the last 10), here’s the big stuff that went down:

- Euro = down -3.1% to close the week at $1.29 (we covered our short position in FXE into week’s end)

- CRB Commodities Index = down -2.7%, after hitting a new cycle-high of 333 on the 1st trading day of 2011

- Oil = down -3.7%, breaking its immediate-term TRADE line of support of $89.46 midweek (we sold our OIL this wk)

- Gold = down -3.7%, breaking its December closing low (we remain short GLD)

- Copper = down -3.6%, after hitting an all-time closing-high of $4.48/lb on the 1st trading day of 2011

- Volatility = down -3.3% to $17.14 on the VIX, after seeing volatility rise in an up US equity market in the 2 weeks prior

I’m no Keynesian, but I (like Keynes did when he was 36 years old) trade currencies and believe them to be a very important barometer of a country’s overall health. In those days, as Liaquat Ahamed wrote in one of my favorite financial history books (Lords of Finance, page 11), “in 1914 the single most important, indeed overriding, objective of these institutions was to preserve the value of the currency.”

As a direct result of last week’s US currency strength, I think last week was a win, win, win for most Americans who care, not only about how much money they make, but how the rest of society does in the meantime.

Let’s look at these 3 wins associated with a strong American currency:

- Stocks went up (SP500 was up +1.1% on the week)

- Inflation went down (that’s what should happen if a country’s currency is pervasively strong)

- Rates of return on our hard earned savings accounts went up (10yr and 30yr US Treasury rates climbed again week-over-week)

No, I’m not saying we are out of the woods yet. I’m just saying that last week was a better week for America by my global macro scorecard than the week prior was – and by the looks of the aforementioned Keynesian quote, the Fiat Fools should agree.

Nor am I saying this was good for the rest of the world (some of their currencies went down, and so did their stock markets):

- India’s BSE Sensex Index = down -4.0%

- Spain’s IBEX Index = down -3.0%

- Luxembourg’s LUX Index = down -2.6%

- Portugal’s PSI Index = down -2.4%

- Taiwan’s TAIEX Index = down -2.1%

- Indonesia’s Jakarta Index = down -1.9%

After all, inflation, like politics, is priced in local currency. This, of course, isn’t a consensus way to look at the world; particularly from a money printing government official’s perspective – but I think that will change.

Whether it was the price of oil hitting an all-time high choking off US consumption in 2008 or the price of the United Nation’s Food Index hitting an all-time high (this week) staring Indian and Indonesian stock markets right in the face (the #2 and #4 largest country size populations in the world), it’s all the same to me. The Fiat Fools around this world are just taking turns.

Back to the Hedgeye Asset Allocation Model, I ended the week with the same allocation to US Cash that I started the week with (61%). Although I did drop down to a 49% position in cash intra-week and changed the complexion of my invested position into Friday’s close (I call this managing risk around my gross invested exposure). My updated positioning is now as follows:

- US Cash = 61%

- International Currencies = 21% (all in the Chinese Yuan, CYB)

- International Equities = 9% (all in German Equities, EWG)

- Commodities = 3% (all in Corn, CORN)

- US Equities = 3% (all in Volatility, VXX)

- Fixed Income = 3% (all in Treasury Inflation Protection, TIP)

Now I fully understand that this isn’t the way that most strategists do it - that’s why I do it this way.

As price, volatility, and volume studies change, I change both my asset allocation positions and invested exposures. For example, I started the week long oil (stocks and the commodity) and US Healthcare stocks (XLV), but Oil broke its immediate-term TRADE line of support and US Healthcare (XLV) became immediate-term TRADE overbought on Thursday. There are no rules stating that I can’t buy either of those positions back (lower) in the coming weeks.

Nor are there rules stating that I can’t get less bearish on US Equities if the US Dollar were to continue to strengthen. US stocks actually closed down for back-to-back sessions for the 1st time on Thursday/Friday since November 29th and 30th. I don’t have to buy them when they are on sale. I don’t have to get bullish on the way down either. I’m just saying that with a 61% cash position, I have plenty of options.

My immediate term support and resistance levels in the SP500 are now 1251 and 1276, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer