Here’s a step back and post mortem on LIZ. Relative to the underlying fundamentals, this is overdone. But the company has not yet earned the benefit of the doubt from anyone. The irony is that the stock has changed more than the story has.

This LIZ blow-up today requires a big step back and post mortem for us. While not in the Hedgeye Virtual Portfolio, I (McGough) have definitely been a bull on LIZ with the stock as a single-digit midget despite the magnitude of challenges facing the industry in 2011.

The crux of our case has been that after 4-years of missing numbers (and releasing more earnings miss press releases than there were quarters) the company would finally start to harvest its investments of the past 2-years and would face positive earnings revisions on dramatically reduced working capital needs while the rest of retail went the other way.

The bottom line is that there was definitely a downturn in our expectations at Lucky, and to a lesser degree, Mexx. But the best way I can characterize this event is that it’s a ‘higher quality miss.’ “C’mon McGough, admit you’re wrong and throw in the towel on this dog.” I’ve had 3 such conversations over the past 12 hours where I heard these words.

But let’s tear it down and see what’s changed.

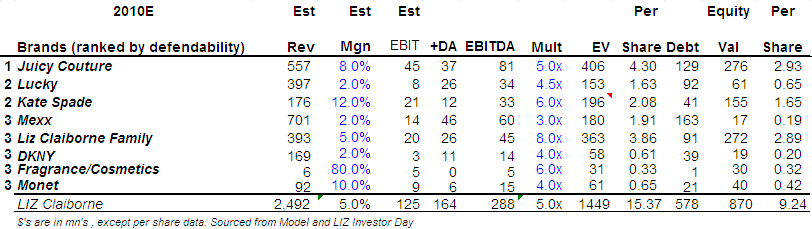

Liz Wholesale/JC Penney:

- It was a painful 2-year build up to the decision to go exclusive with JCP and pull out of other department stores. Leading up to the decision, the company not only lost out on top line, but got beat up on margin and working capital.

- In the 2-years it took to implement, LIZ worked down JCP exposure to Zero. But built up JCP/QVC from Zero.

- The bottom line is that we’re talking a $1bn unprofitable business with high working capital needs. That spells horrible RNOA. Now, they are 1-quarter into a sub $1bn business, but with steady 4-6% margins. That might not seem like much. But msd steady margins on a business with 2-3x operating asset turns is a trade I’ll take any day. The events leading to today’s stock action has Zero bearing on this thesis.

Liz Outlets: The company is nearly out of its 87 money losing Liz Claiborne branded outlet stores in the United States and Puerto Rico. These have been a major earnings and working capital drag. Think about it, with inventory poorly placed by multiple divorces between LIZ and Department Stores, the outlets have borne the brunt. That’s almost over. No change here in thesis.

Consumer Direct Brands:

This is where it gets dicey. I’ve got to check through 12 years of notes to confirm, but I think that this is the first time LIZ has ever called out bad weather as being the key contributing factor. In fact, it’s probably the first time in McComb’s life he’s used it.

Unfortunately, this is impossible for us to validate and/or quantify. What I’ll give ‘em is that all it takes is a simple Google search to find all the videos and news releases discussing the ‘paralyzed’ consumer in Western Europe. I’d argue that even a paralyzed consumer will make sure that they get the best product/value regardless of weather. But changes in consumer confidence rarely occur to a magnitude that would support a 16% negative diversion from one month to another.

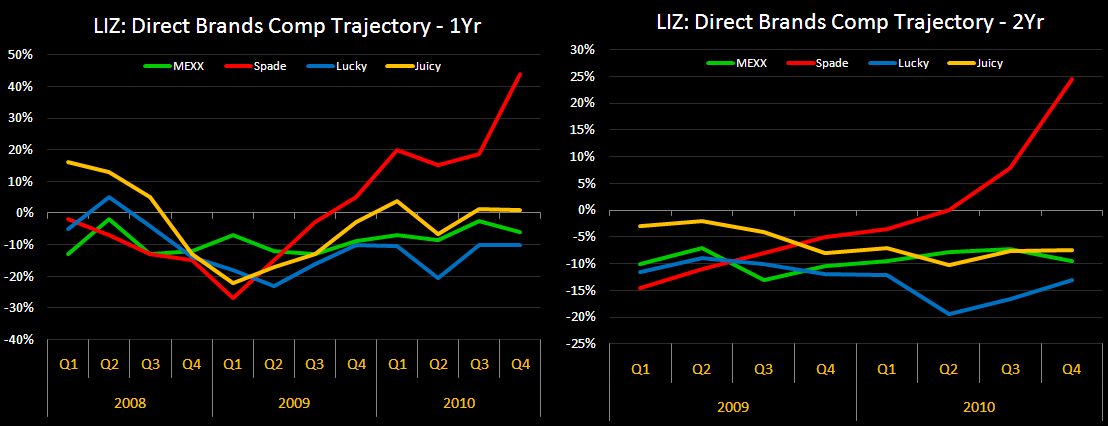

The irony here is that in looking at the underlying comp run rate for all Liz concepts, they all improved on the margin, except for Mexx, and Mexx only eroded by 200-300bps. If management is not flat-out lying about the snow factor, then this really is not that bad.

- That aside, Mexx Europe appears to be making progress early in year 2 under Thomas Grote’s direction with comp performance Oct-Nov flat after 3+ years of posting negative comps in addition to spring order book that’s up 14% both of which are positive on the margin.

- Leadership at both Juicy (Leann Nealz 9/10) and Lucky (Dave DeMattei 12/09) has been replaced within the last 12-months and product selling through now is likely to be legacy lines from the prior management. Spring 2011 is when we’ll likely see new product roll out.

- Despite the decline in December comps, Juicy’s comps on a 1yr and 2yr basis have been steadily improving and in addition to moderate store growth the top-line has reaccelerated in Q3 and Q4.

- Lucky continues to be a most significant drag with underperformance actually accelerating to the downside throughout the quarter with women’s product (over 50% of sales) highlighted at the key reason.

The question is whether the company deserves the benefit of the doubt between now and its 4Q call on February 17th at which time management will provide January trends to determine just how much of the shortfall in December was due to weather vs. product?

For a levered small cap stock over such a short duration, the answer is probably ‘No.” But is there enough for us to take this thing out behind the barn an pop a cap in it? Definitely not.

In fact, after the Feb 17 call, we’ll have better disclosure on the size, profitability and return characteristics of the partner brands and exit of the outlet stores – which we think will be a positive surprise.

Keep in mind that 4 out 5 investor conversations I have on Liz include questions around liquidity. People ask about LBOs on JCP, American Eagle, Carter’s and other peaky margin companies. But they don’t breach the topic on LIZ. Are they asking me about the math as to how you get the Liz Claiborne brand for free at the current price? No. This is completely backwards.