The guest commentary below was written by written by Daniel Lacalle. This piece does not necessarily reflect the opinions of Hedgeye.

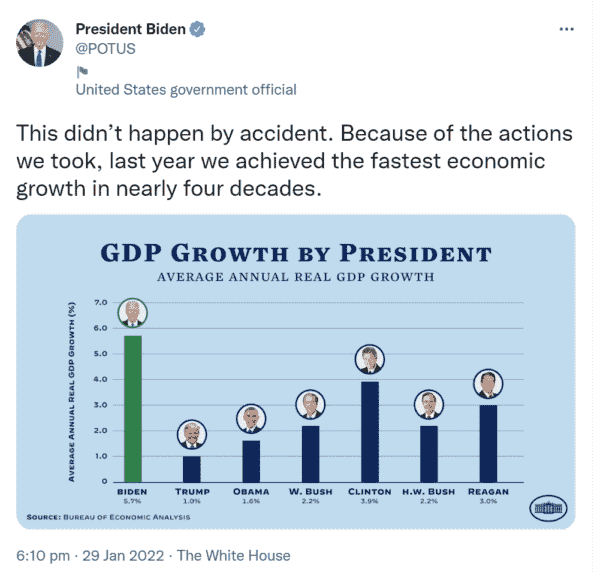

I was surprised to see a tweet from President Biden showing the GDP (Gross Domestic Product) of the United States for 2021 compared to the average GDP growth under other presidents.

The Tweet stated “This didn’t happen by accident. Because of the actions we took, last year we achieved the fastest economic growth in nearly four decades.”

The first thing we must remind the president is that a recovery from a massive crisis is not “growth.” Unfortunately, this marketing tactic is not new.

When Biden was vice-president under Obama, they always compared growth and jobs of the president’s tenure excluding the first year, 2009. Presidents tend to compare their figures favorably, but to talk about 2021 as the “fastest economic growth in nearly four decades” is misleading.

First, recovering the GDP after a massive crisis is not growth. After falling 3.5%, a 5.7% recovery is not “the fastest economic growth” in forty years. It is a bounce.

Furthermore, when inventory build contributed a massive 4.9 percentage points to the 6.9% increase in real GDP of the fourth quarter, we should be cautious. This factor is likely to fade in the first quarter and points to slower growth in 2022.

Seconds, because 2020 and 2021 saw the largest increase in federal debt in decades. After a $3.1 trillion deficit in 2020, the largest in history, and another historic record deficit in 2021 of $2.7 trillion, the United States’ economy has shown a much larger debt increase than GDP recovery.

Current-dollar GDP increased by $2.10 trillion in 2021 to a level of $22.99 trillion, in contrast to a decrease of 2.2 percent, or $478.9 billion, in 2020. This means that the United States economy has barely grown at all after adjusting for the massive increase in debt.

The United States government has consumed 3.5 times more debt than the GDP accumulated in two years.

Third, because the 2021 GDP growth comes with the highest inflation figure in 39 years, a 7% increase in CPI. This means that real wages have plummeted, and consumers are suffering while small and medium enterprises see declining margins.

The slowdown in economic growth that the United States is likely to see in 2022 is an important risk. Industrial production, retail sales and job creation have slowed down notably in the past three months. Let us not forget that the labor force participation rate has been stagnant for a year.

These figures show that the recovery is extremely complicated. More importantly, what these figures show is the extremely poor multiplier effect of government spending and the stimulus plans.

If we put this recovery in the context of the largest monetary and fiscal stimulus in recent history, with two record-high deficit prints, what the Biden tweet shows is the poorest recovery adjusted for debt and monetary support in many decades.

No administration since World War II has used such immense policy actions to deliver above-trend growth and a rapid recovery. However, despite the almost unlimited use of government spending and Federal Reserve resources, including negative real rates and the lowest borrowing cost of government debt in decades, the reality shows an extremely poor and diminishing return of the fiscal and monetary space.

This is also the problem of many economists’ and investment banks’ analysis.

No one seems to care about the massive debt surge and the appalling return on investment of the stimulus plans. If there is something that resembles “growth,” politicians are happy.

But there is a much deeper issue. The accumulated debt will be a burden on growth and jobs in the future, is likely to trigger massive tax increases and, additionally, the placebo effect of the spending plans fades away rapidly. The United States government consumes $1 trillion stimulus plans as of it did not matter.

There is a bounce after such massive adrenaline injection into the economy. But the bounce is clearly insufficient and low quality. The result is higher inflation and no discernible multiplier effect of the spending programs approved because most of the recovery comes from the re-opening of the economy, not from stimulus.

This, unfortunately, is typical in many economies. A lot more debt for weaker growth and higher inflation.

The Biden tweet states that “this is no accident.” He is right. It is more like a Keynesian trainwreck.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor note by economist Daniel Lacalle. He previously worked at PIMCO and was a portfolio manager at Ecofin Global Oil & Gas Fund and Citadel. Lacalle is CIO of Tressis Gestion and author of Life In The Financial Markets, The Energy World Is Flat and the most recent Escape from the Central Bank Trap. This piece does not necessarily reflect the opinions of Hedgeye.