There’s no question expectations were high headed into today’s December sales day and results ended up largely disappointing. Overall, we observed a near 50/50 split of beats to misses with far fewer earnings “guide-ups” than most expected. So where did all the whispers, MasterCard SpendingPulse studies, WikiLeaks go wrong? First, the cadence of the month was hardly linear, with most retailers reporting strength in the earlier half of December vs. the latter. Nothing new here as sales have been volatile on a weekly basis throughout much of 2010, even in the standout periods of March, May, and November. Second, the environment was promotional and perhaps a bit more so than we thought. Third, the weather did have some impact, but this was actually one of the more muted months for making excuses. Only a few retailers even mentioned weather as the culprit, let alone quantify its impact.

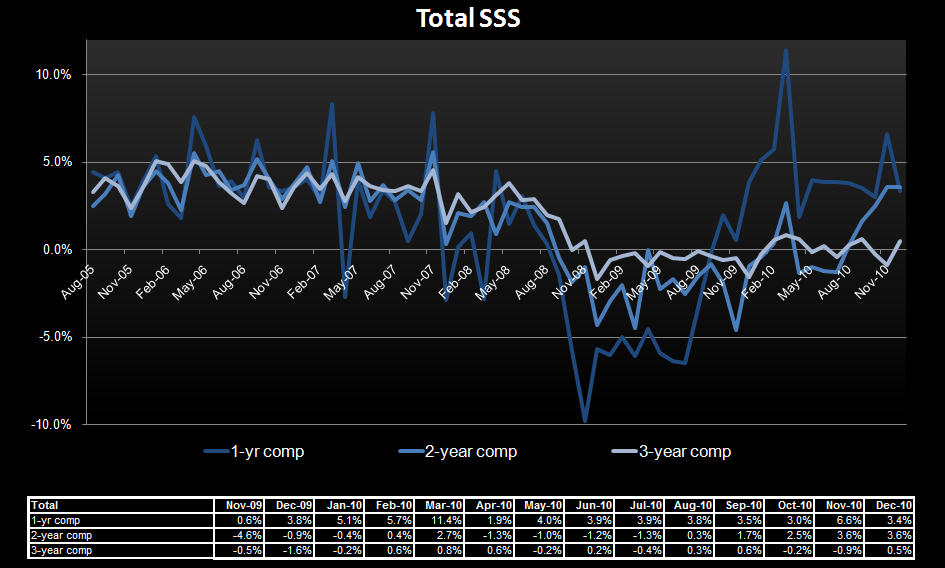

The bottom line here is absent expectations and sentiment that reached fever pitch levels, the actual overall comp growth for the entire 25 company reporting base was 3.4%, exactly in line with the run-rate we observed since June. The only caveat being November (+6.6%), which set the bar abnormally high heading into the more important month of December. Either way we look at it, without a reason (i.e holiday) to spend in the near to intermediate term it’s becoming increasingly difficult to paint a picture of accelerating demand.

As always there were several unique callouts from today’s monthly results:

- High-end clearly outperformed with SKS and JWN reporting strong results both on an absolute and relative-to-expectations basis. In the case of SKS, this number may have been even higher had the blizzard not had an impact on the company’s flagship NYC store (about 19% of the company’s annual sales).

- Off-price was another standout, with both ROST and TJX reporting better than expected and positive comps against very difficult comparisons. Both companies raised guidance. However, the more telling data point was ROST’s statement that their “merchants have been able to take advantage recently of a large amount of compelling close-out opportunities in the marketplace.” Recall that disruption in the marketplace is hugely beneficial to the off-price model and this one of the more bullish comments we’ve seen on the topic of inventory availability in over a year. On the flip side, to take advantage of such buys ROST saw pack-away rise to 47% from 39% for an increase in inventory of 19%!

- If there’s any hope for a recovery in consumer electronics, it will have to come from CES and not from COST. The club operator noted that December sales of consumer electronics were down high single digits, driven by a slightly negative comp in TV’s compounded by weakness in cameras, navigation, and hardware. Computers were positive.

- COST continues to confirm Hedgeye’s view on inflation, with the company noting that fresh food costs were up mid single digits while overall food and sundries saw inflation on the magnitude of 100 to 200 bps. This marks an acceleration in the monthly trends they’ve been consistently noting.

- TGT’s disappointing 0.9% comp store increase leads to many more questions than answers, even in the context of overall weakness for most retailers during the month. The slight increase calls into question the effectiveness of the company’s recent nationwide rollout of the 5% reward program as well as continued push via “P-Fresh” into more consumables. Yes, it’s still early to know if the program’s nationwide adoption rate has been below plan, but there’s no question that this incremental sale driver is not an immediate solution to accelerate sales growth.

- While PIR and CPWM are not the best proxies for overall demand in the home category, they do stand out as substantial sales outperformers during the key holiday season. This is also consistent with robust, pre-holiday results from BBBY. If anything, the category remains less promotional than the fashion apparel landscape.

- There were no shortage of positive e-commerce callouts with KSS reporting a 66% increase in sales, URBN +28%, M +28.4%, AEO +LDD, ANF +59%, and bn.com +78%.

- Sometimes comparisons are overrated. Nordstrom reported its 16th month in a row of increased traffic trends.

Eric Levine

Director