This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

The good news is that the latest wave of COVID seems to be receding even as home prices continue to climb. The bad news is that this week the FOMC is “continuing discussions” about reducing the size of the Fed’s $8 trillion securities portfolio.

But recall, the Fed is still buying bonds and has yet to hike short-term rates. How will this uncertain environment impact banks and nonbank lenders?

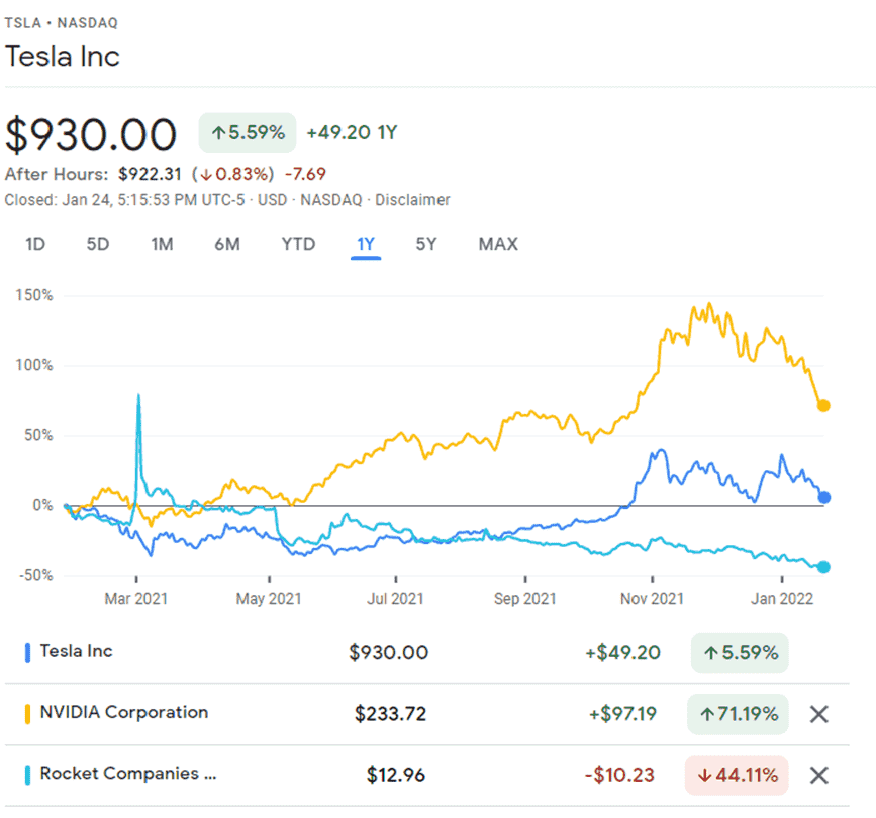

Investors are struggling with price inflation in many goods markets even as the financial sector deflates. Telltale indicators of asset price inflation, Bitcoin tokens and Tesla (TSLA) chief among them, are both sagging as the week begins, but let’s not lose perspective – yet.

Spreads have a long way to go before we return to the crisis levels of Q1 2020. And we are not nearly ready to go shopping.

Just as equity investors are having a tough time making decisions about risk, on or off, the bond market is relatively tranquil, in large part because the FOMC has done an above-average job of telegraphing change.

Think of it as a social learning process. As in 2018 and 2019, the FOMC is going to raise interest rates and deflate its portfolio at the same time. You'd think that Powell & Co have learned by now that tightening target rates while draining liquidity is a bad strategy, but apparently not.

In 2020-2021, the Treasury was the big market mover and the FOMC was forced to accommodate massive spending plans and the aftereffect of those fiscal actions. In 2022, however, the FOMC is the big mover, even as the predicted fiscal wave from Washington is subsiding into the more familiar pattern of inaction.

James Lucier of CapitalAlpha Partners wrote last week: “It’s now officially Build Back Smaller,” this after the Biden Administration abandoned most of its legislative agenda.

The FOMC continues to buy MBS. The buy on Friday was $3.7b, compared to $3.3b in the previous session. As the FOMC struggles with the monstrous pile of assets that has been accumulated over the past 18 months, investors will come to understand how the shrinkage of bank reserves and the coincident decline in Treasury and MBS issuance is going to impact US interest rates. That is, collateral is becoming scarce.

Assuming that the Fed does stop new purchases in March, net supply of MBS this year could reach $600 billion, but there is no shortage of buyers.

Robert W. Baird writes: "GSEs purchased $595.1 billion of newly originated loans in 3Q, a 16.1% decline from the previous period. That represented 71.8% of conventional-conforming origination during the period, the lowest securitization rate since 2019.”

Source: FDIC

This is not about the yield on the 10-year Treasury note understand, but instead about a tectonic shift in the distribution of risk-free assets and how this change impacts spreads for MBS and other debt instruments.

Changes in credit spreads, though uninteresting to equity markets, ultimately drive stocks, especially when the Fed has been manipulating the markets for years. Increased credit spreads mean lower economic growth.

“We saw a 20 bp rise of HY-Ts on Friday and 1 bp rise of BBB-AA,” notes Fred Feldkamp. “By my index, that's a 61 bp decrease in US marginal efficiency of capital. At roughly $5 billion per bp per year, Friday alone ate up capital growth at the rate of $305 B per annum ($3 T over 10 years). If it was not clear that over leveraged firms will soon be forced to report reductions of earnings due to expectations of higher rates, it certainly is clear now.”

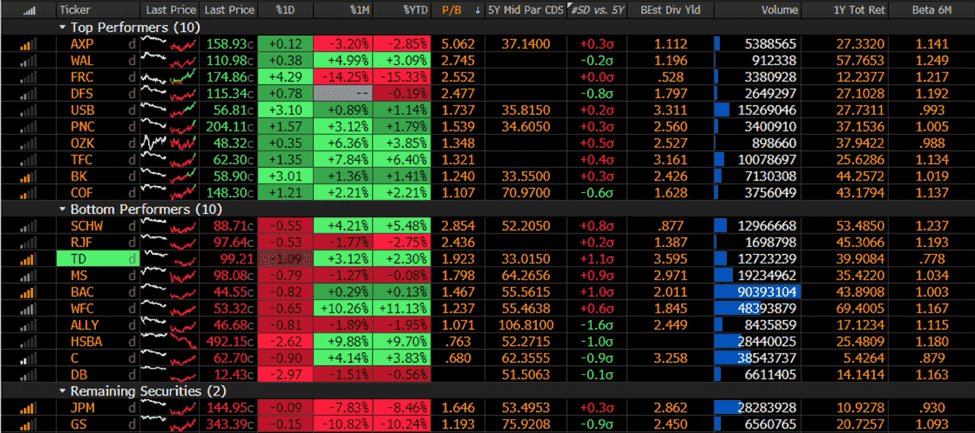

Despite all of the bloodshed in MEME stocks and crypto, the damage to more pedestrian sectors of the stock market is limited. As the screenshot below illustrates, the banking world is relatively unaffected albeit somewhat cheaper than at year-end.

To Feldkamp’s point, notice that JPMorgan (JPM) and Goldman Sachs (GS), two firms with outsized global market exposures, are underperforming the group.

Source: Bloomberg

Both JPM and GS, of note, have derivatives exposures that could wipe out the capital of both banks several times over, but most other US banks avoid such risks.

At the end of September 2021, total derivatives exposure at JPM and GS were 1,345% and 2,800% of total assets, respectively. Citigroup, by comparison, was only 1,818% of total assets at the same date. The average for all large US banks in Peer Group 1 is 28%.

With American Express (AXP) trading north of 5x book and U.S. Bancorp (USB) near 1.8x or now a premium above JPM, the world is not yet ready to end. But the fun in the world of MEME stocks and pretend assets is clearly at an end. JPM strategist Peng Cheng noted yesterday that small investors are heading for the door, selling $1.4 billion in stock before noon Monday.

The key question for risk managers is to differentiate between stocks that have been grossly inflated by the FOMC’s action and general market exuberance, and to what degree.

If you look at valuations for banks back in Q1 2020, for example, the whole industry has essentially gone sideways for two years. If we look at names such as TSLA, NVIDIA (NVDA) and Rocket Companies (RKT), on the other hand, the story is very different.

The moral of the story is that volatility is now a permanent fixture in many markets, especially those assets where FOMC policy has inflated prices excessively. Securities markets can reprice in minutes or hours.

Less efficient markets like residential real estate could overshoot for the next several years. But there are large sectors of the US equity markets that are relatively unaffected by the gyrations so far.

The world is not ending just yet. In the meantime, do watch those credit spreads in coming weeks.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. Currently, he serves as the editor of The Institutional Risk Analyst.